You might also like

- Quizzer - Cost Volume Profit AnalysisDocument8 pagesQuizzer - Cost Volume Profit AnalysisJethro Gutlay100% (3)

- The Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeFrom EverandThe Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeNo ratings yet

- NB New Imperialism or New CapitalismDocument86 pagesNB New Imperialism or New CapitalismvladcostinNo ratings yet

- Answer Key Long Quiz - CVP AnalysisDocument10 pagesAnswer Key Long Quiz - CVP AnalysistanginamotalagaNo ratings yet

- ADDITIONAL PROBLEMS-CVP AnalysisDocument4 pagesADDITIONAL PROBLEMS-CVP AnalysisFerb CruzadaNo ratings yet

- 3 Mas Answer KeyDocument25 pages3 Mas Answer KeyAngelie0% (1)

- 1 Cost Volume Profit AnalysisDocument4 pages1 Cost Volume Profit AnalysisGreta BassettiNo ratings yet

- Lesson 2: Absorption and Variable Costing: Management 9 Review Questions Multiple ChoiceDocument4 pagesLesson 2: Absorption and Variable Costing: Management 9 Review Questions Multiple Choiceandrea0% (1)

- Mas TestbanksDocument25 pagesMas TestbanksKristine Esplana ToraldeNo ratings yet

- The and First: Following CostsDocument20 pagesThe and First: Following CostsVince Christian Padernal100% (1)

- StudentDocument31 pagesStudentKevin CheNo ratings yet

- MAS B41 First Pre-Board Exams (Questions, Answers - Solutions)Document15 pagesMAS B41 First Pre-Board Exams (Questions, Answers - Solutions)Nanananana100% (3)

- MasDocument6 pagesMasZvioule Ma Fuentes100% (2)

- Pricing StrategiesDocument84 pagesPricing StrategiesKashika KohliNo ratings yet

- MS-1stPB 10.22Document12 pagesMS-1stPB 10.22Harold Dan Acebedo0% (1)

- Applied Economics Module 6Document6 pagesApplied Economics Module 6Shaine TamposNo ratings yet

- Mas Final PreboardDocument12 pagesMas Final Preboardpaulodantes099No ratings yet

- Mas MockboardDocument8 pagesMas MockboardMarizza WapinNo ratings yet

- Mas MockboardDocument7 pagesMas MockboardEunice BernalNo ratings yet

- Solution Relevant CostingDocument3 pagesSolution Relevant CostingAnn Salazar0% (1)

- Adms 1010 Class NotesDocument13 pagesAdms 1010 Class NotesOgochukwu A.D.No ratings yet

- Take Home Long QuizDocument5 pagesTake Home Long QuizMa Yumi Angelica TanNo ratings yet

- File 86Document4 pagesFile 86itik meowmeowNo ratings yet

- Strat Cost QuesDocument6 pagesStrat Cost QuesJasmineNo ratings yet

- Break Even Analysis PDFDocument5 pagesBreak Even Analysis PDFJohnpaul Maranan de GuzmanNo ratings yet

- Multiple Choice Questions - PROBLEMS Provide Your Solutions: Commented (1) : BDocument2 pagesMultiple Choice Questions - PROBLEMS Provide Your Solutions: Commented (1) : BSittie Sarah BangonNo ratings yet

- 02 CVP Analysis PDFDocument5 pages02 CVP Analysis PDFJunZon VelascoNo ratings yet

- This Study Resource WasDocument3 pagesThis Study Resource Waschiji chzzzmeowNo ratings yet

- Major Quiz #2Document10 pagesMajor Quiz #2jsus22No ratings yet

- Practice Set 1 (Modules 1 - 3) 371Document8 pagesPractice Set 1 (Modules 1 - 3) 371Marielle CastañedaNo ratings yet

- CostDocument18 pagesCostlordaiztrandNo ratings yet

- Midterm Exam - BSAIS 2ADocument6 pagesMidterm Exam - BSAIS 2AMarilou DomingoNo ratings yet

- Management Advisory Services QuestionnaireDocument12 pagesManagement Advisory Services QuestionnaireSteven Mark MananguNo ratings yet

- Finals Unit 5 Exercise Short Run Decision MakingDocument6 pagesFinals Unit 5 Exercise Short Run Decision MakingDia Mae Ablao GenerosoNo ratings yet

- Activity # 1: Management Advisory Services Part 1Document2 pagesActivity # 1: Management Advisory Services Part 1Vince BesarioNo ratings yet

- Relevant - AssignmentDocument2 pagesRelevant - AssignmentSendo AkiraNo ratings yet

- C. Financial Accounting and Absorption CostingDocument19 pagesC. Financial Accounting and Absorption CostingKelly CardejonNo ratings yet

- MCQ SCM FinalsDocument17 pagesMCQ SCM Finalsbaltazarjosh806No ratings yet

- College of Business Administration and Accountancy Management Advisory Services I Pre-Final ExamDocument3 pagesCollege of Business Administration and Accountancy Management Advisory Services I Pre-Final ExamVel JuneNo ratings yet

- Mas MockboardDocument7 pagesMas MockboardMaurene DinglasanNo ratings yet

- Cvpprac ExamDocument4 pagesCvpprac ExamGwy PagdilaoNo ratings yet

- Quiz #2 - BreakevenDocument1 pageQuiz #2 - BreakevenNelzen GarayNo ratings yet

- Instruction: You Have 3 Hours To Complete This Examination Including Accomplishing The Google Answer SheetDocument16 pagesInstruction: You Have 3 Hours To Complete This Examination Including Accomplishing The Google Answer SheetasdfghjNo ratings yet

- San Sebastian College Recoletos de Cavite Management Accounting Finals Christopher C. LimDocument5 pagesSan Sebastian College Recoletos de Cavite Management Accounting Finals Christopher C. LimAllyssa Kassandra LucesNo ratings yet

- MASDocument2 pagesMASClarisse AlimotNo ratings yet

- CVP Analysis Quiz and Exam QuestionsDocument4 pagesCVP Analysis Quiz and Exam QuestionsWafah HadjisalicNo ratings yet

- Equired Answer Each of The Following Questions IndependentlyDocument2 pagesEquired Answer Each of The Following Questions IndependentlyJan Christopher CabadingNo ratings yet

- Prelims Coverage MasDocument7 pagesPrelims Coverage MasTrisha CabralNo ratings yet

- TO DO - Illustrations (Product Costing and Segment Reporting)Document2 pagesTO DO - Illustrations (Product Costing and Segment Reporting)Lovely De CastroNo ratings yet

- MA REV 1 Finals Dec 2017Document33 pagesMA REV 1 Finals Dec 2017Dale PonceNo ratings yet

- Variable Costing ReviewerDocument3 pagesVariable Costing Reviewerdaniellejueco1228No ratings yet

- 5th Year MidtermDocument11 pages5th Year MidtermJoshua UmaliNo ratings yet

- MCQ Rel CostsRespAcctgTransferPricing PDFDocument6 pagesMCQ Rel CostsRespAcctgTransferPricing PDF수지No ratings yet

- CVP QUIZ TeachersDocument5 pagesCVP QUIZ TeachersAron Ace AycoNo ratings yet

- Examination Midterm MASDocument4 pagesExamination Midterm MASPrincess Claris ArauctoNo ratings yet

- SCM - Pre-Test Questionnaire (Computational)Document7 pagesSCM - Pre-Test Questionnaire (Computational)Angel BrutasNo ratings yet

- BUSE 3 - Practice ProblemDocument8 pagesBUSE 3 - Practice ProblemPang SiulienNo ratings yet

- Test 5Document2 pagesTest 5Kim LimosneroNo ratings yet

- CVP ExerciseDocument4 pagesCVP ExerciseJericho PagsuguironNo ratings yet

- Yes 3Document1 pageYes 3yes yesnoNo ratings yet

- Cost AccountingDocument4 pagesCost AccountingChamp Salcena PerezNo ratings yet

- MASDocument5 pagesMASHeinie Joy PauleNo ratings yet

- Module 2A - CVP AnalysisDocument5 pagesModule 2A - CVP AnalysisBhosx KimNo ratings yet

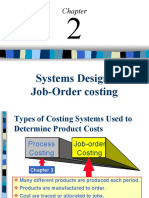

- Systems Design: Job-Order CostingDocument66 pagesSystems Design: Job-Order CostingOvaiss KhanNo ratings yet

- Cor dhvtsutNLYgSmDK5Document1 pageCor dhvtsutNLYgSmDK5Casper VillanuevaNo ratings yet

- Chapter 7Document8 pagesChapter 7Casper VillanuevaNo ratings yet

- Cor dhvtsutNLYgSmDK5Document1 pageCor dhvtsutNLYgSmDK5Casper VillanuevaNo ratings yet

- Cor dhvtsutNLYgSmDK5Document1 pageCor dhvtsutNLYgSmDK5Casper VillanuevaNo ratings yet

- Cor dhvtsutNLYgSmDK5Document1 pageCor dhvtsutNLYgSmDK5Casper VillanuevaNo ratings yet

- Chapter 3Document4 pagesChapter 3Casper VillanuevaNo ratings yet

- Cor dhvtsutNLYgSmDK5Document1 pageCor dhvtsutNLYgSmDK5Casper VillanuevaNo ratings yet

- Chapter 4Document4 pagesChapter 4Casper VillanuevaNo ratings yet

- Cor dhvtsutNLYgSmDK5Document1 pageCor dhvtsutNLYgSmDK5Casper VillanuevaNo ratings yet

- Q.E List Bsa 1HDocument2 pagesQ.E List Bsa 1HCasper VillanuevaNo ratings yet

- BSA 2K AttendanceDocument21 pagesBSA 2K AttendanceCasper VillanuevaNo ratings yet

- Reference Word DocumentDocument2 pagesReference Word Documentanisul1985No ratings yet

- Aggregate Demand and Aggregate Supply EconomicsDocument38 pagesAggregate Demand and Aggregate Supply EconomicsEsha ChaudharyNo ratings yet

- Theories of DevelopmentDocument35 pagesTheories of DevelopmentD Attitude Kid94% (18)

- Principles of Economics Arab World Edition 2nd Edition Mankiw Test BankDocument25 pagesPrinciples of Economics Arab World Edition 2nd Edition Mankiw Test BankEdwardBishopacsy100% (41)

- Corporate Finance HW 10Document4 pagesCorporate Finance HW 10RachelNo ratings yet

- What Are The Characteristics of Human WantsDocument4 pagesWhat Are The Characteristics of Human Wantsgeetkumar18No ratings yet

- One Economic Theory To Explain Everything - Bloomberg PDFDocument6 pagesOne Economic Theory To Explain Everything - Bloomberg PDFMiguel VenturaNo ratings yet

- ECN201 Assignment - 1720297Document15 pagesECN201 Assignment - 1720297Sultana Zannat MilaNo ratings yet

- The International Monetary System Chapter 11Document23 pagesThe International Monetary System Chapter 11Ashi GargNo ratings yet

- Dalit CapitalDocument2 pagesDalit CapitalVivek SinghNo ratings yet

- Supply and Demand: Analytical QuestionsDocument22 pagesSupply and Demand: Analytical QuestionsNghĩa Phạm HữuNo ratings yet

- Financial ManagementDocument9 pagesFinancial ManagementGogineni sai spandanaNo ratings yet

- Midterm ExamDocument14 pagesMidterm Exambeavivo1No ratings yet

- Unit 2 - Demand AnalysisDocument29 pagesUnit 2 - Demand AnalysisSri HimajaNo ratings yet

- Problem Set 5 (Solution)Document5 pagesProblem Set 5 (Solution)Akshit GaurNo ratings yet

- MAS Annual Report 2010 - 2011Document119 pagesMAS Annual Report 2010 - 2011Ayako S. WatanabeNo ratings yet

- The Laffer Curve Past Present and FutureDocument18 pagesThe Laffer Curve Past Present and FutureRullan RinaldiNo ratings yet

- Tietenberg 8e Ppt07 FinalDocument25 pagesTietenberg 8e Ppt07 Finalsamwalt86No ratings yet

- Economic Essays Grade 12Document56 pagesEconomic Essays Grade 12pleasuremaome06No ratings yet

- Entrepreneurship Module - Week 1Document4 pagesEntrepreneurship Module - Week 1Drama LlamaNo ratings yet

- JC KumarappaDocument10 pagesJC KumarappaRAGHUBALAN DURAIRAJUNo ratings yet

- Inflation, Interest Rate, and Exchange Rate: What Is The Relationship?Document11 pagesInflation, Interest Rate, and Exchange Rate: What Is The Relationship?Setyo Tyas JarwantoNo ratings yet

- Stanislav Botan Stanislav Botan Economic Concepts and Models Presentation 1203686 582364799Document15 pagesStanislav Botan Stanislav Botan Economic Concepts and Models Presentation 1203686 582364799cindefuckinbellaNo ratings yet

- Reith 2020 Lecture 1 TranscriptDocument16 pagesReith 2020 Lecture 1 TranscriptHuy BuiNo ratings yet

- The BSP Vision and MissionDocument11 pagesThe BSP Vision and Missioncamille janeNo ratings yet