You might also like

- CSR NotesDocument14 pagesCSR NotesMallik SVNo ratings yet

- CSR-PPT-29 01 2020Document44 pagesCSR-PPT-29 01 2020Acs Kailash TyagiNo ratings yet

- CSR Amendments in Companies (Amendment) Act, 2019 & Companies (Amendment) Act, 2020 AND Companies (CSR Policy) Amendment Rules, 2021Document36 pagesCSR Amendments in Companies (Amendment) Act, 2019 & Companies (Amendment) Act, 2020 AND Companies (CSR Policy) Amendment Rules, 2021Rutvik HNo ratings yet

- CSR-PPT-29 01 2020Document44 pagesCSR-PPT-29 01 2020Acs Kailash TyagiNo ratings yet

- CSR PolicyDocument8 pagesCSR PolicyKaranNo ratings yet

- 0016 Avantika Tijare Assignment 2Document4 pages0016 Avantika Tijare Assignment 2AKSHAT SINGHNo ratings yet

- CSR Laws and GuidelinesDocument4 pagesCSR Laws and Guidelinesanishvijay23No ratings yet

- Not Relating To Ongoing Project-In Case of Failure To Spend The Same, WillDocument4 pagesNot Relating To Ongoing Project-In Case of Failure To Spend The Same, WillJYOTINo ratings yet

- Corporate Social Responsibility PolicyDocument5 pagesCorporate Social Responsibility PolicyRaaj SinghNo ratings yet

- MSL / Note On CSR (Inclusion Provisions of All Amendments Till Date) From: Secretarial & Legal Department / 11 March 2021Document11 pagesMSL / Note On CSR (Inclusion Provisions of All Amendments Till Date) From: Secretarial & Legal Department / 11 March 2021mgsalunke108No ratings yet

- Company CSR Policy As Per Section 135 (4) - 17012020Document5 pagesCompany CSR Policy As Per Section 135 (4) - 17012020rajesh uluwatuNo ratings yet

- 0205 - Pragati - Verma - Assignment - 2 - Pragati VermaDocument6 pages0205 - Pragati - Verma - Assignment - 2 - Pragati VermaAKSHAT SINGHNo ratings yet

- Corporate Social Responsibility Policy: Page 1 of 9Document9 pagesCorporate Social Responsibility Policy: Page 1 of 9Darshan KannurNo ratings yet

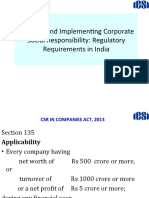

- Planning and Implementing Corporate Social Responsibility: Regulatory Requirements in IndiaDocument23 pagesPlanning and Implementing Corporate Social Responsibility: Regulatory Requirements in IndiaMuskan ManchandaNo ratings yet

- Franklin India CSR PolicyDocument7 pagesFranklin India CSR PolicyBhomik J ShahNo ratings yet

- CSR PolicyDocument10 pagesCSR Policysarvan125384No ratings yet

- CSR - A Panoramic View - DR Bhasker ChatterjiDocument39 pagesCSR - A Panoramic View - DR Bhasker ChatterjicodemakitNo ratings yet

- CSR LawDocument16 pagesCSR LawKarthikNo ratings yet

- Changes in CSR Changes in CSR Laws: IndiaDocument7 pagesChanges in CSR Changes in CSR Laws: IndiaAparajita MarwahNo ratings yet

- CSR Policy 2023-2024Document10 pagesCSR Policy 2023-2024keshnathjnpNo ratings yet

- CSR PolicyDocument14 pagesCSR PolicyJilla Vishwas100% (1)

- Markem Imaje India CSR PolicyDocument6 pagesMarkem Imaje India CSR PolicyAzim KhanNo ratings yet

- CSR PolicyDocument7 pagesCSR PolicyShhanya Madan BhatiaNo ratings yet

- Corporate Social ResponsibilityDocument24 pagesCorporate Social ResponsibilityNaveen MettaNo ratings yet

- CSR Annual Actionp LanDocument4 pagesCSR Annual Actionp LansushantNo ratings yet

- 45 Shivi HalDocument4 pages45 Shivi HalKunal KaushalNo ratings yet

- Company CSR Policy As Per Section 135 (4) - 24072018Document6 pagesCompany CSR Policy As Per Section 135 (4) - 24072018rajesh uluwatuNo ratings yet

- Report On CSRDocument9 pagesReport On CSRVinay VimalNo ratings yet

- CSR Policy New JBMLDocument7 pagesCSR Policy New JBMLKimmi KatariaNo ratings yet

- CSR PolicyDocument5 pagesCSR PolicyRitik SinghalNo ratings yet

- Corporate GovarnanceDocument12 pagesCorporate Govarnancerishabh044No ratings yet

- CSR PolicyDocument12 pagesCSR Policyshivam singhNo ratings yet

- Unitile, India - CSRDocument9 pagesUnitile, India - CSRHakimuddin GheewalaNo ratings yet

- Intex Tech India LTD-CSR PolicyDocument2 pagesIntex Tech India LTD-CSR PolicyBhomik J ShahNo ratings yet

- Rar Unit 4Document12 pagesRar Unit 4raval123690No ratings yet

- Timken - Corporate-Social-Responsibility-PolicyDocument5 pagesTimken - Corporate-Social-Responsibility-Policyadi.arrow7No ratings yet

- CSR and Sustainability Policy - New PDFDocument10 pagesCSR and Sustainability Policy - New PDFNaniNo ratings yet

- CSR Policy FinalDocument4 pagesCSR Policy FinalNaresh khandelwalNo ratings yet

- Company Law AssignmentDocument5 pagesCompany Law AssignmentABISHEK SRIRAM S 17BLA1008No ratings yet

- Corporate Social Responsibility Policy of Nalco (2019)Document8 pagesCorporate Social Responsibility Policy of Nalco (2019)indian Boy1887No ratings yet

- AA CSR Rules, 2021Document5 pagesAA CSR Rules, 2021AkshitaNo ratings yet

- DBS Bank CSR Policy PDFDocument10 pagesDBS Bank CSR Policy PDFArun KumarNo ratings yet

- Corporate Social Responsibility Policy: Version 3-April 2021Document9 pagesCorporate Social Responsibility Policy: Version 3-April 2021Vipul NarwalNo ratings yet

- CSR Policy - BilingualDocument15 pagesCSR Policy - BilingualRanjeet DongreNo ratings yet

- Corporate Social ResponsibilityDocument33 pagesCorporate Social ResponsibilitySharma VishnuNo ratings yet

- CSR-Policy-01-April-2019 - MahindraDocument8 pagesCSR-Policy-01-April-2019 - MahindraPrasad NaikNo ratings yet

- Chapter 3Document16 pagesChapter 3Mayank SenNo ratings yet

- Aarav CSRDocument64 pagesAarav CSRAbhay Singh ParmarNo ratings yet

- FR RTP May 23 - Board NotesDocument43 pagesFR RTP May 23 - Board Notesrocks007123No ratings yet

- CSR Policy of DredgingDocument3 pagesCSR Policy of DredgingSunny SinghNo ratings yet

- PDF 20221103 230325 0000Document44 pagesPDF 20221103 230325 0000Maaza Followers100% (1)

- Corporate Social Responsibility (Section-135) : by Akhil Kodam 20464Document24 pagesCorporate Social Responsibility (Section-135) : by Akhil Kodam 20464Kodam AkhilNo ratings yet

- Preamble: Corporate Social Responsibility (CSR) Policy of Anik Industries LimitedDocument4 pagesPreamble: Corporate Social Responsibility (CSR) Policy of Anik Industries LimitedSeshangNo ratings yet

- DsdsdsdsdsDocument2 pagesDsdsdsdsdssuvendu beheraNo ratings yet

- CSR Policy PDFDocument7 pagesCSR Policy PDFRAJAT SINGHNo ratings yet

- AMBUJA CEMENTS LIMITED Final DraftDocument14 pagesAMBUJA CEMENTS LIMITED Final DraftankitaprakashsinghNo ratings yet

- Public Financial Management Systems—Fiji: Key Elements from a Financial Management PerspectiveFrom EverandPublic Financial Management Systems—Fiji: Key Elements from a Financial Management PerspectiveNo ratings yet

- Fiscal Decentralization Reform in Cambodia: Progress over the Past Decade and OpportunitiesFrom EverandFiscal Decentralization Reform in Cambodia: Progress over the Past Decade and OpportunitiesNo ratings yet

- Week 1 DISCUSSION - Architects Code of Ethics2-CombinedDocument151 pagesWeek 1 DISCUSSION - Architects Code of Ethics2-Combinedjomarie apolinarioNo ratings yet

- Gender Stereotyping (A Human Resource Management Quandary)Document7 pagesGender Stereotyping (A Human Resource Management Quandary)MarriumNo ratings yet

- Rewards Management Report Final of The Finalest of The FinaleDocument56 pagesRewards Management Report Final of The Finalest of The FinaleDave Kurtney EvangelistaNo ratings yet

- Gadia Vs Sykes Asia, Inc. (2015)Document4 pagesGadia Vs Sykes Asia, Inc. (2015)KC ToraynoNo ratings yet

- Job Safety Analysis and Risk Assessment A Case Study of Frontier Ceramics LTDDocument13 pagesJob Safety Analysis and Risk Assessment A Case Study of Frontier Ceramics LTDaraaela 25No ratings yet

- Turnover: Ross Tripp Workforce Planning ManagerDocument12 pagesTurnover: Ross Tripp Workforce Planning ManagerVipin Gairola100% (2)

- Position Paper Labor CaseDocument11 pagesPosition Paper Labor CaseMaharshi Cru90% (30)

- USCIS Draft SolicitationDocument65 pagesUSCIS Draft SolicitationZenger News100% (1)

- Group 10 VivendiDocument18 pagesGroup 10 Vivendipkm84uch100% (1)

- Communication in HospitalityDocument34 pagesCommunication in Hospitalitysanyam nayakNo ratings yet

- EOI 14 2021 22-MinDocument37 pagesEOI 14 2021 22-MinAditya Raj GehlotNo ratings yet

- Agencies 080224104640665Document316 pagesAgencies 080224104640665thu6yaNo ratings yet

- Job Description Security GuardDocument2 pagesJob Description Security GuardFely Grace Anciano Cezar-AguipoNo ratings yet

- Ebook PDF Canadian Human Resource Management 12th Canadian Edition PDFDocument41 pagesEbook PDF Canadian Human Resource Management 12th Canadian Edition PDFdaniel.blakenship846100% (38)

- The Payment of Wages ActDocument8 pagesThe Payment of Wages ActMARITONI MEDALLANo ratings yet

- Draft Business Plan TemplateDocument6 pagesDraft Business Plan TemplateSanket MoteNo ratings yet

- Change Form - M.phill Qualification AllowanceDocument1 pageChange Form - M.phill Qualification AllowanceMuhammad AzamNo ratings yet

- 2 Duty Free Philippines Services Inc Vs Manolito Q TriaDocument10 pages2 Duty Free Philippines Services Inc Vs Manolito Q Triacertiorari19No ratings yet

- Fundamentals of Management: Eleventh EditionDocument35 pagesFundamentals of Management: Eleventh EditionNasser AbdullahNo ratings yet

- Essex County Council2Document8 pagesEssex County Council2James MontgomeryNo ratings yet

- Effect of Work Motivation On Job Performance Among Healthcare Providers in University College Hospital, Ibadan, Oyo StateDocument15 pagesEffect of Work Motivation On Job Performance Among Healthcare Providers in University College Hospital, Ibadan, Oyo StateCentral Asian StudiesNo ratings yet

- Management 01 PDFDocument7 pagesManagement 01 PDFMarlboro RedNo ratings yet

- Resume For E-PorfolioDocument2 pagesResume For E-Porfolioapi-160142920No ratings yet

- Jubilant FoodWorksDocument16 pagesJubilant FoodWorksAarushi ManchandaNo ratings yet

- Nevada Reports 1985 (101 Nev.) PDFDocument864 pagesNevada Reports 1985 (101 Nev.) PDFthadzigsNo ratings yet

- The Role of HR AgentsDocument19 pagesThe Role of HR AgentsAvalon FrederickNo ratings yet

- 238 - Caltex Filipino Managers and Supervisors Assn. v. CIRDocument4 pages238 - Caltex Filipino Managers and Supervisors Assn. v. CIRjovelanvescanoNo ratings yet

- As 567512Document4 pagesAs 567512Vaibhav Patil's VP CreationNo ratings yet

- Manaswini ManuDocument20 pagesManaswini ManuGattumanasviNo ratings yet

- BSCI Long Term GoalDocument3 pagesBSCI Long Term GoalMd. Abdul Hye Siddique0% (1)