You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5811)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- c356641bd6315c8f2cba5eaed3c3ef1aDocument76 pagesc356641bd6315c8f2cba5eaed3c3ef1aRicardo murphy bell MurphyNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Honda Case StudyDocument6 pagesHonda Case StudyPavan KumarNo ratings yet

- Bickslow Bank Statement Template - TemplateLabDocument1 pageBickslow Bank Statement Template - TemplateLabbaga ibakNo ratings yet

- Nick Leeson Barings BankDocument21 pagesNick Leeson Barings BankEric Mac-dorr100% (2)

- Haddock's Centennial History of Jefferson County NY Containing CRAMER History PDFDocument1,098 pagesHaddock's Centennial History of Jefferson County NY Containing CRAMER History PDFJanice R CramerNo ratings yet

- XNTDocument4 pagesXNTKha LidNo ratings yet

- Factors Behind The Rapid Growth in Financial EngineeringDocument3 pagesFactors Behind The Rapid Growth in Financial EngineeringCT SunilkumarNo ratings yet

- 10 Interview Questions and Answers - DAILY JOBS Dubai UAE - New Job OpeningsDocument27 pages10 Interview Questions and Answers - DAILY JOBS Dubai UAE - New Job OpeningsRaza ButtNo ratings yet

- 4Document14 pages4Alex liaoNo ratings yet

- Structural Engineering (M.tech, Applied Mechanics Dept) : Foster Wheeler India Private LimitedDocument11 pagesStructural Engineering (M.tech, Applied Mechanics Dept) : Foster Wheeler India Private LimitedannkkyyNo ratings yet

- Foreign AidDocument3 pagesForeign AidAmna KashifNo ratings yet

- SALN Form 2017 Downloadable Word and PDFDocument3 pagesSALN Form 2017 Downloadable Word and PDFJhun Poblete50% (2)

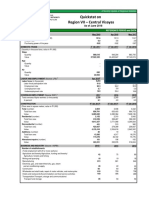

- Region VII - Central Visayas Quickstat On: As of June 2018Document3 pagesRegion VII - Central Visayas Quickstat On: As of June 2018Phil Edgar Contreras RNNo ratings yet

- Sole Proprietor DocumentsDocument3 pagesSole Proprietor DocumentsAmar Ali JunejoNo ratings yet

- Russel Hillberry - Trade and Trade Policy Outlook, 2022 Purdue Agricultural Economics Report PDFDocument5 pagesRussel Hillberry - Trade and Trade Policy Outlook, 2022 Purdue Agricultural Economics Report PDFWilliam WulffNo ratings yet

- Hong Kong Economic SuccessDocument19 pagesHong Kong Economic SuccessKevin LinNo ratings yet

- A Study On Customer Satisfaction of Insurance CompaniesDocument6 pagesA Study On Customer Satisfaction of Insurance CompaniesInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Account Statement From 1 Oct 2020 To 30 Sep 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument14 pagesAccount Statement From 1 Oct 2020 To 30 Sep 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceAartiNo ratings yet

- Flipkart InvoiceDocument1 pageFlipkart InvoiceRobin TirkeyNo ratings yet

- Globalization-Market Integration-NotesDocument13 pagesGlobalization-Market Integration-NotesCheskaNo ratings yet

- This Is A System-Generated Statement. Hence, It Does Not Require Any SignatureDocument9 pagesThis Is A System-Generated Statement. Hence, It Does Not Require Any SignatureLalayadav LalayadavNo ratings yet

- 2009 ACE Limited Annual ReportDocument259 pages2009 ACE Limited Annual ReportACELitigationWatchNo ratings yet

- DiwanDocument12 pagesDiwanfallingleaf_dsNo ratings yet

- Table 1: Seat Allocation Schedule For CSAB NEUT-2023Document1 pageTable 1: Seat Allocation Schedule For CSAB NEUT-2023Surya SweetsNo ratings yet

- Finding Manana EssayDocument5 pagesFinding Manana Essayapi-248362839No ratings yet

- Reflection PaperDocument1 pageReflection Paper2001103622No ratings yet

- CUA Interest RatesDocument1 pageCUA Interest Ratescrazy_babaNo ratings yet

- Capshaw WagesDocument2 pagesCapshaw WagesNevaeh SuttonNo ratings yet

- LAT-05 GL Pak Matiari Lahore Transmission Company 19-02-2018Document46 pagesLAT-05 GL Pak Matiari Lahore Transmission Company 19-02-2018Mubashir HussainNo ratings yet

- Evaluasi Dan StatistikaDocument11 pagesEvaluasi Dan StatistikaAmrita Oza NabillaNo ratings yet