You might also like

- CompilationDocument10 pagesCompilationZandrea LopezNo ratings yet

- Pre Qualifying ExamDocument14 pagesPre Qualifying ExamGelyn CruzNo ratings yet

- Basic AccountingDocument35 pagesBasic AccountingKaraCassandra LayuganNo ratings yet

- 3rdyr - 1stF - Accounting For Business Combinations - 2324Document34 pages3rdyr - 1stF - Accounting For Business Combinations - 2324zaounxosakubNo ratings yet

- SHAREHOLDERSDocument6 pagesSHAREHOLDERSJoana MarieNo ratings yet

- Corporate Accounting MCQDocument10 pagesCorporate Accounting MCQKumareshg GctkumareshNo ratings yet

- BAC 112 Final Departmental Exam (Answer Key) RevisedDocument12 pagesBAC 112 Final Departmental Exam (Answer Key) Revisedjanus lopezNo ratings yet

- Final ADM 3350Document13 pagesFinal ADM 3350Dan Grimsey100% (1)

- BAC 112 Final Examination With QuestionsDocument10 pagesBAC 112 Final Examination With Questionsjanus lopezNo ratings yet

- Compiled Question File FSPDocument22 pagesCompiled Question File FSPsyed aliNo ratings yet

- Wassim Zhani Income Taxation of Corporations (Chapter 9)Document38 pagesWassim Zhani Income Taxation of Corporations (Chapter 9)wassim zhaniNo ratings yet

- Acc 603 Test 2 Fall 2011Document7 pagesAcc 603 Test 2 Fall 2011Steph Stevens0% (1)

- Adv Fin AcctDocument7 pagesAdv Fin Accthikio30No ratings yet

- Afar Quick NotesDocument35 pagesAfar Quick NotesMichelle AlvarezNo ratings yet

- 2-1 Accounting ReviewerDocument15 pages2-1 Accounting ReviewerJulienne S. RabagoNo ratings yet

- Partnership ReviewerDocument11 pagesPartnership Reviewerbae joohyun0% (1)

- Saint Louis College Final Examinations: College of Commerce, Secretarial and Accountancy (CCSA)Document4 pagesSaint Louis College Final Examinations: College of Commerce, Secretarial and Accountancy (CCSA)Ivan RiveraNo ratings yet

- ACC 221 - Second ExaminationDocument4 pagesACC 221 - Second ExaminationCharlesNo ratings yet

- ACC501 Practice Exam IIDocument32 pagesACC501 Practice Exam IIgilli1trNo ratings yet

- Dwnload Full Pearsons Federal Taxation 2019 Comprehensive 32nd Edition Rupert Test Bank PDFDocument36 pagesDwnload Full Pearsons Federal Taxation 2019 Comprehensive 32nd Edition Rupert Test Bank PDFsportfulscenefulzb3nh100% (12)

- Practice Questions On Partnership BusinessDocument4 pagesPractice Questions On Partnership BusinessBamidele AdegboyeNo ratings yet

- Exam AnswersDocument5 pagesExam AnswersKelly Smith100% (2)

- FIN370 Final ExamDocument9 pagesFIN370 Final ExamWellThisIsDifferentNo ratings yet

- Dwnload Full Pearsons Federal Taxation 2019 Corporations Partnerships Estates Trusts 32nd Edition Anderson Test Bank PDFDocument36 pagesDwnload Full Pearsons Federal Taxation 2019 Corporations Partnerships Estates Trusts 32nd Edition Anderson Test Bank PDFsportfulscenefulzb3nh100% (13)

- Pre Quali 2019Document9 pagesPre Quali 2019Haidie DiazNo ratings yet

- Question Auditing ExamDocument11 pagesQuestion Auditing ExamAbbyRenn0% (1)

- Problem Set For Exam 1 - SolutionsDocument4 pagesProblem Set For Exam 1 - SolutionsInesNo ratings yet

- 2ndyr 2ndMT Accounting For Special Transaction 2223Document38 pages2ndyr 2ndMT Accounting For Special Transaction 2223Cristina VenturaNo ratings yet

- Quiz No. 1Document6 pagesQuiz No. 1Elboy Son DecanoNo ratings yet

- AFAR-1stPB 10.22Document12 pagesAFAR-1stPB 10.22Cyrene Joy RamaNo ratings yet

- Mba Ii Sem - FM - QBDocument29 pagesMba Ii Sem - FM - QBMona GhunageNo ratings yet

- Mca - 204 - FM & CFDocument28 pagesMca - 204 - FM & CFjaitripathi26No ratings yet

- Quiz 2 Lesson 3Document5 pagesQuiz 2 Lesson 3Andreau Granada0% (1)

- Advacc 1 Quiz 1 With AnswersDocument9 pagesAdvacc 1 Quiz 1 With AnswersGround ZeroNo ratings yet

- Consolidation-Method (Ta)Document7 pagesConsolidation-Method (Ta)Tram NgocNo ratings yet

- Quiz Pension SHEDocument8 pagesQuiz Pension SHEErine ContranoNo ratings yet

- Ross12e Chapter01 TBDocument12 pagesRoss12e Chapter01 TBHải YếnNo ratings yet

- Corporate Finance Canadian 7th Edition Jaffe Test BankDocument27 pagesCorporate Finance Canadian 7th Edition Jaffe Test Bankdeborahmatayxojqtgzwr100% (13)

- Ollege Usiness Ducation: International School of Asia and The PacificDocument10 pagesOllege Usiness Ducation: International School of Asia and The PacificNana GandaNo ratings yet

- Multiple Choice Questions: Business CombinationsDocument25 pagesMultiple Choice Questions: Business CombinationsHera AsuncionNo ratings yet

- Dividend QuestionsDocument6 pagesDividend QuestionsperiNo ratings yet

- Acct C.H.10Document6 pagesAcct C.H.10j8noelNo ratings yet

- Accounting On Business Combination Quiz 2: Multiple ChoiceDocument13 pagesAccounting On Business Combination Quiz 2: Multiple ChoiceTokkiNo ratings yet

- Chapter 1: Partnership: Part 1: Theory of AccountsDocument10 pagesChapter 1: Partnership: Part 1: Theory of AccountsKeay Parado0% (1)

- FAR 2 REVIEWER Other SourceDocument120 pagesFAR 2 REVIEWER Other SourceAirish GeronimoNo ratings yet

- JPIA Review S3 Installment 2 (Accounting For Business Combinations)Document30 pagesJPIA Review S3 Installment 2 (Accounting For Business Combinations)rylNo ratings yet

- BSA 1101 Fundamentals of Basic Accounting 1 and 2 FinalsDocument16 pagesBSA 1101 Fundamentals of Basic Accounting 1 and 2 FinalsJohn AcunaNo ratings yet

- Comprehensive Examinations 2 (Part I)Document13 pagesComprehensive Examinations 2 (Part I)Yander Marl BautistaNo ratings yet

- Fin622 McqsDocument25 pagesFin622 McqsIshtiaq JatoiNo ratings yet

- Full Download Advanced Accounting Jeter 5th Edition Test Bank PDF Full ChapterDocument36 pagesFull Download Advanced Accounting Jeter 5th Edition Test Bank PDF Full Chapterbeatencadiemha94100% (11)

- Advanced Accounting Jeter 5th Edition Test BankDocument36 pagesAdvanced Accounting Jeter 5th Edition Test Bankuraninrichweed.be1arg100% (39)

- Advanced Accounting Jeter 5th Edition Test BankDocument14 pagesAdvanced Accounting Jeter 5th Edition Test Bankjasonbarberkeiogymztd100% (48)

- Fundamentals of Financial Accounting 6th Edition Phillips Test BankDocument158 pagesFundamentals of Financial Accounting 6th Edition Phillips Test BankFeliciaPhillipstaqjo100% (13)

- Section 1 30 Marks Determine The Single Most Appropriate Response To The Following QuestionsDocument15 pagesSection 1 30 Marks Determine The Single Most Appropriate Response To The Following QuestionsHelloWorldNowNo ratings yet

- MCQ-on-FM WITH SOLDocument28 pagesMCQ-on-FM WITH SOLarmansafi761100% (1)

- B&a - MCQDocument11 pagesB&a - MCQAniket PuriNo ratings yet

- Final Spring 2021 (B)Document6 pagesFinal Spring 2021 (B)rtgxd25zygNo ratings yet

- Corporate Finance Canadian 7th Edition Ross Test BankDocument27 pagesCorporate Finance Canadian 7th Edition Ross Test BankChristinaCrawfordigdyp100% (16)

- Series 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2023 Edition)From EverandSeries 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2023 Edition)No ratings yet

- SIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2023 Edition)From EverandSIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2023 Edition)Rating: 5 out of 5 stars5/5 (1)

- Career Opportunities FairDocument105 pagesCareer Opportunities FairWilfrido MolinaresNo ratings yet

- Letter From Revenue Minister Diane LebouthillierDocument2 pagesLetter From Revenue Minister Diane LebouthillierCTV NewsNo ratings yet

- Income Tax and Benefit Return: IdentificationDocument8 pagesIncome Tax and Benefit Return: Identification1flailstarNo ratings yet

- Application For A T100 Identification Number (Tin) On The Exercise of Flow-Through Warrants (FTWS) and Details of The Ftws ExercisedDocument2 pagesApplication For A T100 Identification Number (Tin) On The Exercise of Flow-Through Warrants (FTWS) and Details of The Ftws ExercisedtstscribdNo ratings yet

- Instructions For Completing This Form 13.1 Financial StatementDocument33 pagesInstructions For Completing This Form 13.1 Financial StatementMy Support CalculatorNo ratings yet

- Shade NeDocument4 pagesShade Nezermaine.brooksNo ratings yet

- It419r2-E Arms LengthDocument8 pagesIt419r2-E Arms LengthAyesha NaazNo ratings yet

- RT Unification Shareholder CircularDocument357 pagesRT Unification Shareholder CircularLeon Vara brianNo ratings yet

- BC RAHA Homeowners ApplicationDocument8 pagesBC RAHA Homeowners ApplicationJennifer MacGaulNo ratings yet

- 14 - Chapter 5Document32 pages14 - Chapter 5Sukanya DuttaNo ratings yet

- rc65 Fill 22eDocument3 pagesrc65 Fill 22eprisweetstrawNo ratings yet

- Chapter 6 - DeductionsDocument86 pagesChapter 6 - DeductionsRyan YangNo ratings yet

- CPA 417828 Dialogue Volume 44 - Issue 1 ENGDocument44 pagesCPA 417828 Dialogue Volume 44 - Issue 1 ENGKrista RNo ratings yet

- Chapter 13 Lecture Notes (TA 2020) - Non-Financial and Current LiabilitiesDocument20 pagesChapter 13 Lecture Notes (TA 2020) - Non-Financial and Current LiabilitiesTSEvansNo ratings yet

- Tax Administration 2021 OecdDocument355 pagesTax Administration 2021 OecdscorpioboyNo ratings yet

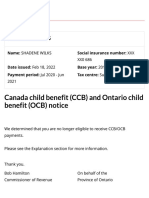

- OTB Notice 2020 08 20 19 15 50 176254Document4 pagesOTB Notice 2020 08 20 19 15 50 17625469j8mpp2scNo ratings yet

- Starting Small Business MBDocument40 pagesStarting Small Business MBnimaaaaaaaNo ratings yet

- Math 10-3 Unit 2.3 - 2.4 Worksheet - Additional Earnings - Pay 2018-19 STUDENTDocument5 pagesMath 10-3 Unit 2.3 - 2.4 Worksheet - Additional Earnings - Pay 2018-19 STUDENTBob SmynameNo ratings yet

- Taxable Benefits and Allowances: Employers' GuideDocument47 pagesTaxable Benefits and Allowances: Employers' GuideZhen WeiNo ratings yet

- 2022 Property Tax Exemption FormDocument5 pages2022 Property Tax Exemption FormsplouffevachonNo ratings yet

- Byrd and Chens Canadian Tax Principles 2011 2012 Edition Canadian 1st Edition Byrd Test BankDocument59 pagesByrd and Chens Canadian Tax Principles 2011 2012 Edition Canadian 1st Edition Byrd Test BankDavidRobertsdszbc100% (14)

- Esdc Emp5519Document16 pagesEsdc Emp5519Manan MughalNo ratings yet

- Form 13.1 - Financial StatementDocument10 pagesForm 13.1 - Financial StatementRobert GradNo ratings yet

- General Income Tax and Benefit Guide: Canada Revenue AgencyDocument63 pagesGeneral Income Tax and Benefit Guide: Canada Revenue AgencyvolvoproNo ratings yet

- Child Care Business Manual FinalDocument88 pagesChild Care Business Manual FinalGrace Yesaya100% (1)

- Hello Canada Account Activation FormDocument6 pagesHello Canada Account Activation FormRomeo Newtown EshalomNo ratings yet

- Stephen Harper VS Non ProfitsDocument28 pagesStephen Harper VS Non ProfitsAndre FaustNo ratings yet

- Identity Theft and Suspicious Activity Declaration Form For Individual, Business and TrustDocument2 pagesIdentity Theft and Suspicious Activity Declaration Form For Individual, Business and TrustJennifer LeetNo ratings yet

- Schedule 2-19e - FillDocument1 pageSchedule 2-19e - FillHiwa Khan SalamNo ratings yet

- County Analysis Utilizing Census Tract DataDocument38 pagesCounty Analysis Utilizing Census Tract DataCaroline BontempoNo ratings yet