months and 3 ● Used to reduce the

STATEMENT OF weeks overall value of

FINANCIAL POSITION ● Convertible to the assets

amount of cash

● Also known as the

which is subject to Trade and other

“balance sheet”

an insignificant risk receivables

● Shows: the

to changes in value Accounts receivable

condition of the

Marketable securities ● The amount

company as of a

● These are stocks collectible from the

given period

and bonds customer to whom

● It is a clear

purchased by the sales have been

representation of

enterprise and are made or rendered

the accounting

to be held for only ● On account/ credit

equation

a short period or ● E.g. inutang ni

● Formula: A=L+OE

short duration customer anf

Trades and other goods (AR) cause

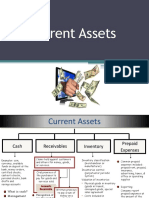

ASSETS

receivable walang natanggap

2 types of assets

● Collectible amounts si company

1. Current asset

Inventories Notes receivable

2. Non-current asset

● Unsold goods at ● The client issued a

Current asset

the end of the promissory note in

● Classified and

accounting period exchange for

presented

● Raw goods, in services or goods

according to

progress goods (in received as

liquidity

the process but not evidence

● Most liquid asset

yet finished) ● Obligation to pay

● Convertible to cash

Prepaid expenses ● A written pledge

within 1 year

● Supplies bought for that the customer

use in the business will pay a fixed

Classification of current

or service amount of money

assets

● Paid in advance on a certain date

Cash

● Expenses paid in Interest receivable

● Coins, currencies,

business in ● Amounts of interest

checks, bank

advance collectible on

deposits, bills, bank

● E.g. apartment promissory notes

balances, & money

rental you need to received from the

orders

pay in advance customer

● Available for use in

even if you have Advances to employees

the operations of

used it yet ● Amounts of money

the business

Contra-asset account loaned to

Cash equivalents

● Account deducted employees payable

● Investment

from the related in cash or through

securities for a

asset account salary deduction

short-term

maximum of 2

Accrued income property , plant and 4. Utilities payable

● Income already equipment 5. Unearned

earned but not yet ● Tangible assets revenues

received or that held by an Accounts payable

recorded enterprise for use ● Debts arising from

in the production the purchase of an

Other current asset: ● Long-term assets asset of service on

Supplies vital to business account

operations & not ● The money owned

● Cost of supplies on

easily converted by the business to

hand to operate

into cash its supplier

● E.g. pen, paper, ink, ● E.g. land, building, ● E.g. the supplier of

clip equipment, shoes so you have

furniture and a pair of shoes

Contra-asset accounts fixture, and fixtures then next time you

1. Allowance for bad service vehicle will pay the pair of

debts Intangible assets shoes in short,

● Losses due to ● Not physical in supplies before

uncollectible nature (can’t touch) pay

amounts ● E.g. brand name, Notes payable

Accumulated patents, copyright ● Evidence by a

depreciation license franchise, promissory note

● Expired cost of trademark, ● Liability in writing

Property, pants, & subscription lists, Utilities payable

equipment as a secret processes, ● Obligation to pay

result of usage and the utility company

non-competition for services

Classification of agreements received from them

non-current assets ● A company owned

Non-current asset Liabilities for utility

● Convertible to cash 1. Current liabilities ● E.g. electricity,

within a year 2. Non-current water, gas

Long-term investment liabilities ● Explanation: a

● Enterprise for Current liabilities company received

accretion of wealth ● Debt of a business utility bill but hasn’t

through capital that they have to paid it yet

distribution pay in a short Unearned revenues

● E.g. interest, period of time ● Company receives

royalties, dividends payment from the

and rentals for Classification of current customer before

other benefits to liabilities providing the goods

the inventing 1. Account payable or services

enterprise 2. Notes payable ● Advance payments

3. Loan payable received before

goods or services

Balance - Current the

are provided to the sheet assets business in

customer -Non its

● E.g. booking of current operation

ticket assets to produce

-liabilities revenues

Non-current liabilities (current

and non E.g. sell a

● Long term current) shirt of 600

liabilities/ and is the

obligations which cost of

are payable for the Owners Capital sales is

period longer than equity withdrawal 600

s

1 year

Salaries

Income Revenues expense:

Classification of statement expenses cost

non-current liabilities incurred to

pay

Mortgage payable employees

● Long term debt of

Utilities

the business with Owners Capital: expense:

security or equity original & cost

collateral in the additional incurred by

form of real investment using

of the utilities

property

owner of

● E.g. you lend a the Rent

money to a bank, business expense:s

the banks need a pace and

collateral (land) Withdrawa equipment

then the bank will ls: owners or other

give a money of the asset

business rentals

Bonds payable

removes

● Certificate of cash Insurance

indebtedness &other expense :

under the seal of a assets expired

corporation from the portion of

● Repayment and the business. insurance

rate of interest to For

personal Supplies

be charged expense:

use

expense of

expenses Cost of using

sales: supplies

Cost of

assets

used by

Week 3: why financial Transparency and 1. Entity concept

statement are important accountability 2. Periodicity

& the rules in financial ● Disclosing financial 3. Going concern

reporting information, Entity concept

ensuring ● Business separate

Financial statement accountability to from its owners and

● Crucial documents stakeholders, from other

that provide a regulators, and the business

snapshot of a public ● Business is

company's Basis for taxation and separated from

financial compliance personal money

performance ● Basis for tax Periodicity

● Important several calculations and ● Financial

reasons: decision regulatory accounting

making, compliance information about

performance ● Legal and standard the economic

evaluation, Financial reporting activities of an

transparency & ● Rules and principle enterprise

accountability, & to ensure 1. Fiscal year: feb to

basis for taxation accuracy, january * can start

and compliance consistency, and any months

Decision making comparability 2. Calendar year:

● Investors, Generally accepted january to

shareholders, use accounting principles( december

FS to make GAAP) ● Both have 12

informed decisions ● Rules and months

about investing, procedures Going concern

lending, or ● Serve as guides in ● Business

partnering with a the practice of enterprise will

company accounting continues to

Performance evaluation ● These are operate indefinitely

● Help to assess a standard, ● Infinity

company assumptions, and

profitability, concepts with Basic accounting

liquidity, solvency, general principle

and overall acceptability 1. Objectivity

performance over a ● It measure the principle

period techniques ans 2. Historical cost

● Allowing standards used in 3. Accrual principle

comparisons with the presentation 4. Adequate

industry standards and preparation of disclosure

and competitors financial 5. Materiality

statements 6. Consistency

Fundamental concepts Objectivity

● All business result between time single - step income

transactions that and periods statement

will be entered in ● It presents the

the accounting INCOME STATEMENT revenue, expenses

records must be ● It shows the and ultimately the

duly supported by company’s financial profit/ losses

verifiable performance during generated by a

evidence a particular period business

Historical cost ● It consist: revenue, ● Report information

● All properties and cost, & period by using 1 equation

services acquired ● FORMULA: to calculate profits

by the business REVENUE LESS: ● Straightforward

must be recorded EXPENSES= accounting of the

at their original PROFIT financial activity of

acquisition cost Revenue your business

Accrual principle ● Money a company ● Easy to understand

● Income should be actually receives & easy to prepare

recognized at the during a specific

time it is earned period

such as when Gains

goods are ● Increase in the

delivered or when value of an asset or

services have been property e.g.

rendered income from sale

Adequate disclosure of van Multi-step income

● All materials Expenses statement

facts that ● Economic costs a ● Same general

will affect business incurs in information

the financial order to revenue included in a

statements e.g. wages, rent, sing;e-step income

must be salaries, interest statement.

indicated paid ● Uses multiple

Materiality Losses equations to

● Financial reporting ● Portion of an determine the net

is only concerned insurance income, or profit of

with information company’s the company

that affects reserves for unpaid

decisions losses and costs of

Consistency investigation and

● Used in reporting adjustment losses

must be uniformly e.g. settlement

employed from cost of consumer

period to period to lawsuit

all comparison of

Net sales Salaries and wages

● The sum of a expense

company’s gross ● Compose of all the

sales minus its payments made to

return, employees or

allowances,& workers for rending

discounts services to the

company

Utilities expense

● Expenses related

Accounts in the single- to the use of

step income statement electricity, & water

1. Service income Supplies expense

2. Salaries or eagles ● Covers office

expenses supplies used by

3. Utilities expense the company in the

4. Supplies expense conduct of its daily

5. Insurance operation

expense Insurance expense

6. Depreciation ● Amount that the

expense company pays to

7. Uncollectible get an insurance

accounts cintract and any

expenses/ additional premium

doubtful account payments

expense/ bad ● Once they expire,

debts expense recorded as

8. Interest expense expense

Depreciation expense

Service income ● Annual portion of

● Revenue earned or the cost of tangible

generated by the assets such as

business in buildings,

performing service machineries, and

for a customer equipment charged

● E.g. laundry as expense for the

service by laundry year

shop (laundry ● E.g.

income), dental

services by dentist

(dental fees),

medical services by

doctores (medical

fees)

You might also like

- Example of Non-Current AssetDocument4 pagesExample of Non-Current AssetPatricia Isabelle Smith FloresNo ratings yet

- Sofp NotesDocument4 pagesSofp NotesLyka MillorNo ratings yet

- Accounting Midterm ReviewerDocument14 pagesAccounting Midterm Reviewerlorenadelejero14No ratings yet

- FM ReviewerDocument7 pagesFM ReviewerBianca MalinabNo ratings yet

- SSLIDES - VATEL - LSLIDES - Chap 4Document36 pagesSSLIDES - VATEL - LSLIDES - Chap 4uyenthanhtran2312No ratings yet

- Types of Accounts and The Account TitlesDocument25 pagesTypes of Accounts and The Account TitlesSeung BatumbakalNo ratings yet

- Accounting Finals 1 ReviewerDocument5 pagesAccounting Finals 1 ReviewerlaurenNo ratings yet

- Business MathDocument4 pagesBusiness MathPamela MarieNo ratings yet

- Accounting NotesDocument6 pagesAccounting NotesD AngelaNo ratings yet

- Module 2 - Slides - Introducing Financial StatementsDocument12 pagesModule 2 - Slides - Introducing Financial StatementsElizabethNo ratings yet

- Accounting Reviewer 2nd Long TestDocument45 pagesAccounting Reviewer 2nd Long TestZachary Job YuipcoNo ratings yet

- Fabm12 1ST QTRDocument4 pagesFabm12 1ST QTRAraNo ratings yet

- Topic - Explaining The Concept of Cash Flow Statement (Operating, Investing and Financing Activities)Document15 pagesTopic - Explaining The Concept of Cash Flow Statement (Operating, Investing and Financing Activities)Sakshi koulNo ratings yet

- Chapter 2 - The Accounting Equation and The Double Entry SystemDocument3 pagesChapter 2 - The Accounting Equation and The Double Entry SystemalonNo ratings yet

- Accounts ReceivablesDocument37 pagesAccounts ReceivablesYassi CurtisNo ratings yet

- Fabm 1 PS 11 Q3 0602Document49 pagesFabm 1 PS 11 Q3 0602ABM 11-5 Maneja, Ford Zedrick R.No ratings yet

- Fabm 1 - Week 4Document3 pagesFabm 1 - Week 4FERNANDO TAMZ2003No ratings yet

- Short Notes Financial AccountigDocument9 pagesShort Notes Financial AccountigNajihah AbNo ratings yet

- Pointers To Review: FABM 2: Recording Phase: Answer KeyDocument9 pagesPointers To Review: FABM 2: Recording Phase: Answer KeyMaria Janelle BlanzaNo ratings yet

- Fabm Week 4 Study GuideDocument3 pagesFabm Week 4 Study GuideFERNANDO TAMZ2003No ratings yet

- 4types of Major Accounts-For Observation2Document13 pages4types of Major Accounts-For Observation2Marilyn Nelmida TamayoNo ratings yet

- Basics of Accounting 3 Double Entry Book Keeping RulesDocument44 pagesBasics of Accounting 3 Double Entry Book Keeping Rulesjiten zopeNo ratings yet

- Financial StatementsDocument32 pagesFinancial Statementspeterpark0903No ratings yet

- 7 Elements of FS-specific AccountsDocument28 pages7 Elements of FS-specific Accountsivygem saanNo ratings yet

- Chapter 2 NLKTDocument58 pagesChapter 2 NLKTPhan Lê Anh Đào100% (1)

- Pertemuan 3 Current AssetDocument46 pagesPertemuan 3 Current AssetJason wibisonoNo ratings yet

- Accounting TerminologyDocument37 pagesAccounting Terminologyjhj01No ratings yet

- Chapter 3Document20 pagesChapter 3Nareen RajNo ratings yet

- 1five Major AccountsDocument30 pages1five Major AccountsEaster LumangNo ratings yet

- Financial Concepts 18 AprilDocument33 pagesFinancial Concepts 18 Aprilapi-295284877100% (1)

- Types of Major AccountsDocument6 pagesTypes of Major Accountsks505eNo ratings yet

- ACCOUNTING CYCLE STEP 1 TO 4 With IllustrationsDocument6 pagesACCOUNTING CYCLE STEP 1 TO 4 With IllustrationsmallarilecarNo ratings yet

- CONFRAS 1 (Practice Quiz)Document4 pagesCONFRAS 1 (Practice Quiz)Jessica MalabananNo ratings yet

- Fabm 4THDocument3 pagesFabm 4THDrahneel MarasiganNo ratings yet

- Essential Elements of The Definition of AccountingDocument9 pagesEssential Elements of The Definition of AccountingPamela Diane Varilla AndalNo ratings yet

- FABM2-Chapter 1Document31 pagesFABM2-Chapter 1Marjon GarabelNo ratings yet

- ACCOUNTINGDocument7 pagesACCOUNTINGGaga LalaNo ratings yet

- 3 - Current AssetsccDocument46 pages3 - Current AssetsccrintoatgpNo ratings yet

- Ey Terms: 3 3 4 Chapter 8 - ReceivablesDocument11 pagesEy Terms: 3 3 4 Chapter 8 - ReceivablesRaffay Maqbool100% (1)

- ConceptDocument2 pagesConceptYan YangNo ratings yet

- Cfas - ReceivablesDocument9 pagesCfas - ReceivablesYna SarrondoNo ratings yet

- Account TitlesDocument5 pagesAccount TitlesalyNo ratings yet

- Accounting: Nature of Accounting Business OrganizationDocument2 pagesAccounting: Nature of Accounting Business OrganizationRochelle Joy CruzNo ratings yet

- (ACCCOB2) Chapters 3-5 Receivables, Investments, InventoryDocument11 pages(ACCCOB2) Chapters 3-5 Receivables, Investments, InventoryMichaella PurgananNo ratings yet

- Acct 018 Chapter 4 5Document4 pagesAcct 018 Chapter 4 5rivera.roshelleNo ratings yet

- 5 6138856670966580425Document4 pages5 6138856670966580425sssNo ratings yet

- 1 LiabilitiesDocument39 pages1 LiabilitiesDiana Faith TaycoNo ratings yet

- Chapter 3 - Statement of Financial Position and Income StatementDocument28 pagesChapter 3 - Statement of Financial Position and Income Statementshemida75% (4)

- Chap 3 - Acctg Clasification Element of FSDocument21 pagesChap 3 - Acctg Clasification Element of FSEli Syahirah100% (1)

- Chapter 2Document22 pagesChapter 2John Edwinson JaraNo ratings yet

- Pas 7Document3 pagesPas 7Sacedon, Trishia Mae C.No ratings yet

- Balance Sheet - Ratio AnalysisDocument49 pagesBalance Sheet - Ratio AnalysisKarishmaAshuNo ratings yet

- Audit Group AssignmentDocument23 pagesAudit Group AssignmentShavi GurugeNo ratings yet

- Reviewer FinanceDocument4 pagesReviewer FinanceCalivo, Carl JohnNo ratings yet

- Financial Accounting For Managers: Shailesh PeriwalDocument7 pagesFinancial Accounting For Managers: Shailesh PeriwalNatasha DassNo ratings yet

- FabmDocument5 pagesFabmJihane TanogNo ratings yet

- Accounting PPT - Intangible AssetDocument58 pagesAccounting PPT - Intangible AssetGokul RamNo ratings yet

- FA1 NotesDocument270 pagesFA1 NotesNida KhanNo ratings yet

- Business Analysis & ValuationDocument50 pagesBusiness Analysis & ValuationAimee EemiaNo ratings yet

- Collateral Document Delivery Request Form v2Document1 pageCollateral Document Delivery Request Form v2Teena BarrettoNo ratings yet

- Presentation On IOCL - PPT On SUMMER INTERNSHIP PROJECTDocument15 pagesPresentation On IOCL - PPT On SUMMER INTERNSHIP PROJECTMAHENDRA SHIVAJI DHENAK33% (3)

- Cancellation Acord Form - CX149661-Ramon Aguilar-Aguila Trucking PDFDocument1 pageCancellation Acord Form - CX149661-Ramon Aguilar-Aguila Trucking PDFBryan ArenasNo ratings yet

- Hanlon Heitzman 2010Document53 pagesHanlon Heitzman 2010vita cahyanaNo ratings yet

- Igcse Accounting Multiple Choice FDocument43 pagesIgcse Accounting Multiple Choice FAung Zaw HtweNo ratings yet

- Slm-Strategic Financial Management - 0 PDFDocument137 pagesSlm-Strategic Financial Management - 0 PDFdadapeer h mNo ratings yet

- Important Points of Our Notes/Books:: TH THDocument42 pagesImportant Points of Our Notes/Books:: TH THpuru sharmaNo ratings yet

- 1557278181265Document12 pages1557278181265Hema VarmanNo ratings yet

- Philippine Red Cross (Non-Government Organization) : University of Perpetual Help System DALTADocument15 pagesPhilippine Red Cross (Non-Government Organization) : University of Perpetual Help System DALTAFroilan Arlando BandulaNo ratings yet

- PricingDocument2 pagesPricingKishore kandurlaNo ratings yet

- Doing Business in BrazilDocument164 pagesDoing Business in BrazilVarupNo ratings yet

- ADVANCED FA Chap IIIDocument7 pagesADVANCED FA Chap IIIFasiko Asmaro100% (1)

- ADMS 1010, ADMS 3530, ADMS 2511, All York BAS Course MaterialsDocument6 pagesADMS 1010, ADMS 3530, ADMS 2511, All York BAS Course MaterialsFahad33% (3)

- Lecture3 Sem2 2023Document35 pagesLecture3 Sem2 2023gregNo ratings yet

- PW Department CodesDocument19 pagesPW Department CodesanilNo ratings yet

- Pakistan Water and Power Development Authority: (In Quadruplicate)Document2 pagesPakistan Water and Power Development Authority: (In Quadruplicate)AsadAli100% (1)

- 14 Excise Invoice FormatDocument1 page14 Excise Invoice FormatZahirabbas BhimaniNo ratings yet

- Unit IvDocument26 pagesUnit Ivthella deva prasadNo ratings yet

- M Form 2019Document4 pagesM Form 2019Kamille Ann RiveraNo ratings yet

- 26nov2022 - 30jan2023Document12 pages26nov2022 - 30jan2023Srishti SharmaNo ratings yet

- Daily Report MonitoringDocument9 pagesDaily Report MonitoringMaasin BranchNo ratings yet

- 201FIN Tutorial 3 Financial Statements Analysis and RatiosDocument3 pages201FIN Tutorial 3 Financial Statements Analysis and RatiosAbdulaziz HNo ratings yet

- (Sarvesh Dhatrak) Derivatives in Stock Market and Their Importance in HedgingDocument79 pages(Sarvesh Dhatrak) Derivatives in Stock Market and Their Importance in Hedgingsarvesh dhatrakNo ratings yet

- Project Report LissstDocument6 pagesProject Report LissstShivareddyNo ratings yet

- Sat YamDocument39 pagesSat YamShashank GuptaNo ratings yet

- Direst Selling Agent Policy-Retail & Consumer LendingDocument13 pagesDirest Selling Agent Policy-Retail & Consumer LendingVijay DubeyNo ratings yet

- AdmissionDocument23 pagesAdmissionPawan TalrejaNo ratings yet

- InflationDocument40 pagesInflationmaanyaagrawal65No ratings yet