You might also like

- Bookkeeping And Accountancy Made Simple: For Owner Managed Businesses, Students And Young EntrepreneursFrom EverandBookkeeping And Accountancy Made Simple: For Owner Managed Businesses, Students And Young EntrepreneursNo ratings yet

- The 8 Steps of The Accounting CycleDocument3 pagesThe 8 Steps of The Accounting Cyclemary grace sijuelaNo ratings yet

- Accounting Cycle 22-01069Document3 pagesAccounting Cycle 22-01069Huzaifa FaheemNo ratings yet

- 8 Steps in Accounting CycleDocument2 pages8 Steps in Accounting CycleMarko Zero FourNo ratings yet

- What Is Accounting?: Cash FlowsDocument4 pagesWhat Is Accounting?: Cash FlowsMamun RezaNo ratings yet

- UntitledDocument4 pagesUntitledJeco OlarveNo ratings yet

- Accounting CycleDocument21 pagesAccounting CycletamoorNo ratings yet

- Far - Nica TomitaDocument3 pagesFar - Nica TomitaMikayNo ratings yet

- Accounting CycleDocument4 pagesAccounting CycleAmitNo ratings yet

- Financial Accounting: Daksh Gautam 22/834 Topic: Accounting ProcessDocument13 pagesFinancial Accounting: Daksh Gautam 22/834 Topic: Accounting ProcessDaksh GautamNo ratings yet

- Accounting Cycle StepsDocument4 pagesAccounting Cycle StepsAntiiasmawatiiNo ratings yet

- Introduction: The Accounting Process Is A Series of Activities That BeginsDocument20 pagesIntroduction: The Accounting Process Is A Series of Activities That BeginsMiton AlamNo ratings yet

- Contingent Liability 3Document3 pagesContingent Liability 3David John MoralesNo ratings yet

- Contingent Liability 2Document2 pagesContingent Liability 2David John MoralesNo ratings yet

- ACC 003 - Fundamentals of Accounting Part 2 Lesson Title: Review The Accounting Cycle Lesson Objectives: ReferencesDocument2 pagesACC 003 - Fundamentals of Accounting Part 2 Lesson Title: Review The Accounting Cycle Lesson Objectives: ReferencesRochelle Joyce CosmeNo ratings yet

- Angelina - Kwofie - 301121003 Buac-171Document7 pagesAngelina - Kwofie - 301121003 Buac-171Yano NettleNo ratings yet

- New Microsoft Office Word DocumentDocument2 pagesNew Microsoft Office Word DocumentFarooq HaiderNo ratings yet

- The Accounting Cycle Is A Series of Steps. Starts With Making Accounting Entries For Each Transaction and Goes Through Closing The BooksDocument15 pagesThe Accounting Cycle Is A Series of Steps. Starts With Making Accounting Entries For Each Transaction and Goes Through Closing The Booksmay matabangNo ratings yet

- Accounting CycleDocument2 pagesAccounting CycleMa. Aizey TorresNo ratings yet

- The Accounting CycleDocument3 pagesThe Accounting Cycleliesly buticNo ratings yet

- Accounting CycleDocument2 pagesAccounting CycleDNLNo ratings yet

- Records in JournalDocument2 pagesRecords in JournalYhamNo ratings yet

- Accounting CycleDocument3 pagesAccounting CycleMardy DahuyagNo ratings yet

- Accountancy ProjectDocument14 pagesAccountancy ProjectKshitize NigamNo ratings yet

- What Is The Accounting Cycle?Document4 pagesWhat Is The Accounting Cycle?GOT MLNo ratings yet

- The Accounting Cycle: 9-Step Accounting Process InshareDocument3 pagesThe Accounting Cycle: 9-Step Accounting Process InshareBTS ARMYNo ratings yet

- Steps in The Accounting CycleDocument3 pagesSteps in The Accounting CycleAklilu TadesseNo ratings yet

- The Accounting Cycle: 9-Step Accounting ProcessDocument2 pagesThe Accounting Cycle: 9-Step Accounting Processfazal rahmanNo ratings yet

- New Microsoft Word DocumentDocument2 pagesNew Microsoft Word Documentracc wooyoNo ratings yet

- Accounting Cycle DefinedDocument3 pagesAccounting Cycle DefinedMichele RogersNo ratings yet

- What Is Accounting and What Is Its Purpose? What Is Its Role in Decision-Making?Document4 pagesWhat Is Accounting and What Is Its Purpose? What Is Its Role in Decision-Making?Jpoy RiveraNo ratings yet

- What Is The Accounting CycleDocument2 pagesWhat Is The Accounting CycleSHREE KRISHNA TUTORIALSNo ratings yet

- The Accounting Cycle: 9-Step Accounting ProcessDocument3 pagesThe Accounting Cycle: 9-Step Accounting ProcessLala ArdilaNo ratings yet

- Assignment On Accounting Cycle of A Business ConcernDocument6 pagesAssignment On Accounting Cycle of A Business Concernkhalid masumNo ratings yet

- The Accounting Cycle: 1. TransactionsDocument2 pagesThe Accounting Cycle: 1. TransactionsJonalyn MontecalvoNo ratings yet

- State The Three Fundamental Steps in The Accounting ProcessDocument5 pagesState The Three Fundamental Steps in The Accounting Processmashila arasanNo ratings yet

- Accounting CycleDocument3 pagesAccounting CycleShanta MathaiNo ratings yet

- 7 The Accounting CycleDocument3 pages7 The Accounting Cycleapi-299265916No ratings yet

- Accounting Cycle StepsDocument3 pagesAccounting Cycle Stepsjewelmir100% (1)

- 1.3 AccountingDocument4 pages1.3 Accountingnez.829.aNo ratings yet

- Rac 101 - Journals and LedgersDocument13 pagesRac 101 - Journals and LedgersKevin TamboNo ratings yet

- The Eight Steps of The Accounting CycleDocument9 pagesThe Eight Steps of The Accounting CycleDana GoanNo ratings yet

- What Is The Accounting Cycle?: Financial Statements BookkeeperDocument4 pagesWhat Is The Accounting Cycle?: Financial Statements Bookkeepermarissa casareno almueteNo ratings yet

- Accounting and Internal ControlsDocument2 pagesAccounting and Internal ControlsReylyn May CoderaNo ratings yet

- Accounting CycleDocument5 pagesAccounting CycleMikaela JuanNo ratings yet

- General AccountingDocument94 pagesGeneral Accountingswaroopbaskey2100% (1)

- Understanding The Accounting Cycle in Trading BusinessDocument4 pagesUnderstanding The Accounting Cycle in Trading BusinessHafidzi Derahman100% (1)

- Entrepreneurship: Quarter 2: Module 7 & 8Document15 pagesEntrepreneurship: Quarter 2: Module 7 & 8Winston MurphyNo ratings yet

- Acc201 Su2Document5 pagesAcc201 Su2Gwyneth LimNo ratings yet

- Accounting CycleDocument11 pagesAccounting Cyclemmaxy2566No ratings yet

- What Is The Accounting Cycle?Document2 pagesWhat Is The Accounting Cycle?Nadie LrdNo ratings yet

- Cheyanne Rhine Southern New Hampshire University ACC 201 7/13/2018Document1 pageCheyanne Rhine Southern New Hampshire University ACC 201 7/13/2018Ciprnn NortonNo ratings yet

- Chapter 6 LectureDocument21 pagesChapter 6 LectureDana cheNo ratings yet

- Bs in Hospitality Management: St. Nicolas College of Business and TechnologyDocument3 pagesBs in Hospitality Management: St. Nicolas College of Business and TechnologyMaria Charise TongolNo ratings yet

- The Accounting Cyc: 1. Identify TransactionsDocument8 pagesThe Accounting Cyc: 1. Identify TransactionsEnatnesh DegagaNo ratings yet

- Module 3 CFAS PDFDocument7 pagesModule 3 CFAS PDFErmelyn GayoNo ratings yet

- Flow Chart - Trial Balance - WikiAccountingDocument6 pagesFlow Chart - Trial Balance - WikiAccountingmatthew mafaraNo ratings yet

- ch03 Intermediate AccountingDocument34 pagesch03 Intermediate AccountingMostafa MohamedNo ratings yet

- Translate Into Vienamese What Is A Bookkeeping Journal? What Is A Daybook?Document4 pagesTranslate Into Vienamese What Is A Bookkeeping Journal? What Is A Daybook?Minh HoàngNo ratings yet

- Vivek Chauhan Chapter 1 04727488820 Bcom (H) 5th SemesterDocument19 pagesVivek Chauhan Chapter 1 04727488820 Bcom (H) 5th SemesterVivek ChauhanNo ratings yet

- SOA TemplateDocument20 pagesSOA TemplateNrkNo ratings yet

- LNT Grasim CaseDocument9 pagesLNT Grasim CaseRickMartinNo ratings yet

- Asian Currencies Sink in 1997Document3 pagesAsian Currencies Sink in 1997majidpathan208No ratings yet

- DESENTRALISASI Pengukuran Kinerja Di Organisasi Yang TerdesentralisasiDocument110 pagesDESENTRALISASI Pengukuran Kinerja Di Organisasi Yang Terdesentralisasimuhammad raflyNo ratings yet

- Charrie Mae MDocument2 pagesCharrie Mae MRaymond GanNo ratings yet

- Quicken Loans Decision 03-09-17Document52 pagesQuicken Loans Decision 03-09-17MLive.comNo ratings yet

- ICAEW Advanced Level Corporate Reporting Study Manual Chapter Wise Interactive Questions With Immediate AnswersDocument191 pagesICAEW Advanced Level Corporate Reporting Study Manual Chapter Wise Interactive Questions With Immediate AnswersOptimal Management Solution100% (1)

- Seller'S Full LetterheadDocument4 pagesSeller'S Full LetterheadRailesUsados83% (6)

- FINALS EXAM - FinAcctg SetADocument4 pagesFINALS EXAM - FinAcctg SetAJennifer RasonabeNo ratings yet

- CFA Institute Research ChallengeDocument3 pagesCFA Institute Research ChallengeAritra BhowmikNo ratings yet

- Ipsas 10-Financial Reporting in Hyperinflationary EconomiesDocument16 pagesIpsas 10-Financial Reporting in Hyperinflationary EconomiesEmmaNo ratings yet

- Billing Address: Tax InvoiceDocument1 pageBilling Address: Tax InvoiceManojkumar DNo ratings yet

- Spectrans M1 M2Document7 pagesSpectrans M1 M2Patricia CruzNo ratings yet

- 20221224-CITIC-Giant Biogene 2367.HK Initiation Exploring A Second Growth CurveDocument6 pages20221224-CITIC-Giant Biogene 2367.HK Initiation Exploring A Second Growth CurvejsbcpersonalNo ratings yet

- CS231 - A&H Application For ReinstatementDocument1 pageCS231 - A&H Application For ReinstatementLiyan OngNo ratings yet

- Ex - Scenario and Sensitifity AnalysisDocument3 pagesEx - Scenario and Sensitifity AnalysisSakura Rosella100% (1)

- Cibil Report KAILASH CHAND FULARA1564842956149 PDFDocument3 pagesCibil Report KAILASH CHAND FULARA1564842956149 PDFKaran FularaNo ratings yet

- Report Financial ManagementDocument30 pagesReport Financial ManagementRishelle Mae C. AcademíaNo ratings yet

- 0088470515-Premium Deposit Acknowledgement PDFDocument1 page0088470515-Premium Deposit Acknowledgement PDFjayanandaNo ratings yet

- Motilal Oswal Financial Services LTDDocument5 pagesMotilal Oswal Financial Services LTDseawoodsNo ratings yet

- Financial Econometrics IntroductionDocument13 pagesFinancial Econometrics IntroductionPrabath Suranaga MorawakageNo ratings yet

- Amplify University TrainingDocument11 pagesAmplify University Trainingshariz500100% (1)

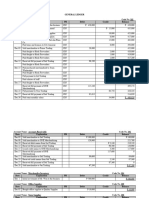

- General LedgerDocument4 pagesGeneral Ledger21-53070No ratings yet

- 13-Fair Value MeasurementDocument46 pages13-Fair Value MeasurementChelsea Anne VidalloNo ratings yet

- GE - Authorization FormDocument2 pagesGE - Authorization FormYiki TanNo ratings yet

- Internship Report On Deposit and Investment Management of Al Arafah Islami Bank LimitedDocument211 pagesInternship Report On Deposit and Investment Management of Al Arafah Islami Bank LimitedWahidHossainNo ratings yet

- 2017 ReportDocument67 pages2017 Reportআত্মজীবনীNo ratings yet

- Home Loans Project ReportDocument105 pagesHome Loans Project Reportkaushal2442No ratings yet

- Characteristics of The RestaurantDocument2 pagesCharacteristics of The RestaurantSudhansuSekharNo ratings yet

- Office of The State ComptrollerDocument4 pagesOffice of The State ComptrollerflippinamsterdamNo ratings yet

- Getting to Yes: How to Negotiate Agreement Without Giving InFrom EverandGetting to Yes: How to Negotiate Agreement Without Giving InRating: 4 out of 5 stars4/5 (652)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)From EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Rating: 4.5 out of 5 stars4.5/5 (15)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindFrom EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindRating: 5 out of 5 stars5/5 (231)

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)From EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Rating: 4.5 out of 5 stars4.5/5 (5)

- SAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsFrom EverandSAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsNo ratings yet

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!From EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Rating: 4.5 out of 5 stars4.5/5 (14)

- A Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineFrom EverandA Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineNo ratings yet

- Overcoming Underearning(TM): A Simple Guide to a Richer LifeFrom EverandOvercoming Underearning(TM): A Simple Guide to a Richer LifeRating: 4 out of 5 stars4/5 (21)

- Purchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsFrom EverandPurchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsRating: 5 out of 5 stars5/5 (1)

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)From EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Rating: 4 out of 5 stars4/5 (33)

- Start, Study and Pass The CPA Exam FAST - Proven 8 Step CPA Exam Study PlaybookFrom EverandStart, Study and Pass The CPA Exam FAST - Proven 8 Step CPA Exam Study PlaybookRating: 5 out of 5 stars5/5 (4)

- Ratio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to Analyse Any Business on the PlanetFrom EverandRatio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to Analyse Any Business on the PlanetRating: 4.5 out of 5 stars4.5/5 (14)

- Financial Accounting For Dummies: 2nd EditionFrom EverandFinancial Accounting For Dummies: 2nd EditionRating: 5 out of 5 stars5/5 (10)

- Warren Buffett and the Interpretation of Financial Statements: The Search for the Company with a Durable Competitive AdvantageFrom EverandWarren Buffett and the Interpretation of Financial Statements: The Search for the Company with a Durable Competitive AdvantageRating: 4.5 out of 5 stars4.5/5 (109)

- Accounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCFrom EverandAccounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCRating: 5 out of 5 stars5/5 (1)

- Accounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsFrom EverandAccounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsRating: 4 out of 5 stars4/5 (7)

- The Big Four: The Curious Past and Perilous Future of the Global Accounting MonopolyFrom EverandThe Big Four: The Curious Past and Perilous Future of the Global Accounting MonopolyNo ratings yet

- Your Amazing Itty Bitty(R) Personal Bookkeeping BookFrom EverandYour Amazing Itty Bitty(R) Personal Bookkeeping BookNo ratings yet

- Attention Pays: How to Drive Profitability, Productivity, and AccountabilityFrom EverandAttention Pays: How to Drive Profitability, Productivity, and AccountabilityNo ratings yet

- Contract Negotiation Handbook: Getting the Most Out of Commercial DealsFrom EverandContract Negotiation Handbook: Getting the Most Out of Commercial DealsRating: 4.5 out of 5 stars4.5/5 (2)

- The E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItFrom EverandThe E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItRating: 4.5 out of 5 stars4.5/5 (14)