You might also like

- Merged Documen of Strata Act - Rules&RegulationsDocument72 pagesMerged Documen of Strata Act - Rules&RegulationsCarla HaleyNo ratings yet

- The Tamil Nadu Stamp Prevention of Undervaluation TaNaStPrUnInRu1968COM17142Document10 pagesThe Tamil Nadu Stamp Prevention of Undervaluation TaNaStPrUnInRu1968COM17142Arpit AgarwalNo ratings yet

- Title Section: The Land (Rent and Service Charge) Act, 1974Document17 pagesTitle Section: The Land (Rent and Service Charge) Act, 1974SAID HAMADNo ratings yet

- Acts - Odisha Apartment Ownership Amendment Act 2015Document10 pagesActs - Odisha Apartment Ownership Amendment Act 2015dan barNo ratings yet

- Rajasthan Apartment Ownership ActDocument18 pagesRajasthan Apartment Ownership ActPrashant KaushikNo ratings yet

- The Punjab Urban Immovable Property Tax Rules 1958Document11 pagesThe Punjab Urban Immovable Property Tax Rules 1958Muhammad Aamir50% (2)

- Landlord and Tenant Act, No 6 of 1999Document18 pagesLandlord and Tenant Act, No 6 of 1999Corine EmilienNo ratings yet

- Rera Maharashtra DocumentDocument62 pagesRera Maharashtra DocumentArjun BhattNo ratings yet

- 3243420115150147483judgement09 Oct 2023 1 497485Document33 pages3243420115150147483judgement09 Oct 2023 1 497485SekharNo ratings yet

- Uganda Local Government (Rating) Act 2005Document21 pagesUganda Local Government (Rating) Act 2005African Centre for Media Excellence100% (4)

- Dar Es Salaam, A.J.Chenge, 30 June, 2000 Attorney GeneralDocument29 pagesDar Es Salaam, A.J.Chenge, 30 June, 2000 Attorney GeneralSteven Kisamo AmbroseNo ratings yet

- The Punjab Urban Immovable Property Tax Rules 1958 PDFDocument12 pagesThe Punjab Urban Immovable Property Tax Rules 1958 PDFHammad KhanNo ratings yet

- Show PDFDocument12 pagesShow PDFSujal KumarNo ratings yet

- The Himachal Pradesh Urban Rent Cotrol Act, 1987 Arrangement of SectionsDocument35 pagesThe Himachal Pradesh Urban Rent Cotrol Act, 1987 Arrangement of Sectionsabhishek kanwarNo ratings yet

- Intituled: 1. (1) This Act May Be Cited As The Land AcquisitionDocument35 pagesIntituled: 1. (1) This Act May Be Cited As The Land AcquisitionveercasanovaNo ratings yet

- Maharashtra Slum Areas Improvement ClearanceDocument47 pagesMaharashtra Slum Areas Improvement ClearancehkatniwalaNo ratings yet

- Appendix Notification: 1. Short Title. - These Rules May Be Called The TamilDocument41 pagesAppendix Notification: 1. Short Title. - These Rules May Be Called The TamilPROGETTO GKNo ratings yet

- The Urban Immovable Property Tax Rules, 1958Document31 pagesThe Urban Immovable Property Tax Rules, 1958abbasNo ratings yet

- R - The Uttar Pradesh PublicDocument12 pagesR - The Uttar Pradesh PublicPARAS MONGIANo ratings yet

- RA No 10752 The Right of Way ActDocument6 pagesRA No 10752 The Right of Way ActCarlemae SanquinaNo ratings yet

- Rera - Shubham TapkirDocument36 pagesRera - Shubham Tapkirshubham.gaurav.sensibullNo ratings yet

- Begun and Held in Metro Manila, On Monday, The Twenty-Seventh Day of July, Two Thousand FifteenDocument7 pagesBegun and Held in Metro Manila, On Monday, The Twenty-Seventh Day of July, Two Thousand FifteenDebra BraciaNo ratings yet

- TDR Rules 2017 PDFDocument20 pagesTDR Rules 2017 PDFVinay SengarapNo ratings yet

- High Coirt Order SraDocument48 pagesHigh Coirt Order SraMohd ShaikhNo ratings yet

- R 67expropration Other Laws PDFDocument2 pagesR 67expropration Other Laws PDFFutureLawyerNo ratings yet

- Republic Act No. 10752 An Act Facilitating The Acquisition of Right-Of-way Site or Location For National Government Infrastructure ProjectsDocument6 pagesRepublic Act No. 10752 An Act Facilitating The Acquisition of Right-Of-way Site or Location For National Government Infrastructure ProjectsMilio MilioNo ratings yet

- The Urban Immovable Property Tax RulesDocument5 pagesThe Urban Immovable Property Tax RulesTashweed HussainNo ratings yet

- Revenue Recovery Act, 1890Document6 pagesRevenue Recovery Act, 1890Mubashir IqbalNo ratings yet

- TN Regulation of Rights and Responsibilities of Landlords and Tenants Act, 2017Document25 pagesTN Regulation of Rights and Responsibilities of Landlords and Tenants Act, 2017KumaramtNo ratings yet

- TN Rent Tenancy Act 2017 PDFDocument19 pagesTN Rent Tenancy Act 2017 PDFthesrajesh7120No ratings yet

- TN Rent Tenancy Act 2017Document19 pagesTN Rent Tenancy Act 2017thesrajesh7120No ratings yet

- Council Tax LetterDocument7 pagesCouncil Tax LetterNadia MackayNo ratings yet

- LL 2.8 CompensationDocument22 pagesLL 2.8 CompensationsuhasiniNo ratings yet

- Uttar Pradesh Shashan Avasevamshahriniyojan Anubhag-3Document52 pagesUttar Pradesh Shashan Avasevamshahriniyojan Anubhag-3rkapoor584199No ratings yet

- The Landlord and Tenant Act 1999Document20 pagesThe Landlord and Tenant Act 1999Ungapen KartikayNo ratings yet

- RA10752 - Acquisition of Right of Way-Rule67 On ExproprationDocument13 pagesRA10752 - Acquisition of Right of Way-Rule67 On Exproprationkreistil weeNo ratings yet

- Rajasthan Rent ControlDocument21 pagesRajasthan Rent Controlsomeswar dutNo ratings yet

- Registration CertificateDocument3 pagesRegistration CertificateAnup SharmaNo ratings yet

- AP Residential and Non Residential Tenancy ActDocument18 pagesAP Residential and Non Residential Tenancy ActGeethesh JaddaNo ratings yet

- Chhattisgarh Rent Control ActDocument7 pagesChhattisgarh Rent Control ActAntriksh yadavNo ratings yet

- Rent Act (Cap 206)Document25 pagesRent Act (Cap 206)Tazilinda Mulenga100% (1)

- Tenancy Act 2017Document13 pagesTenancy Act 2017pavana krishnaNo ratings yet

- RA 7160 - Book 2 - Local TaxationDocument22 pagesRA 7160 - Book 2 - Local TaxationRobert Ramirez100% (1)

- Haryana Urban (Control of Rent and Eviction) Act 1973Document17 pagesHaryana Urban (Control of Rent and Eviction) Act 1973UTKARSHNo ratings yet

- HP Urban Rent Control Act, 1987Document35 pagesHP Urban Rent Control Act, 1987Karan Aggarwal0% (1)

- 300 Ex III 1a 0 Land Acquitation 2017Document52 pages300 Ex III 1a 0 Land Acquitation 2017Anand KumarNo ratings yet

- Right of WayDocument8 pagesRight of WayChelle Rico Fernandez BONo ratings yet

- Land LawsDocument14 pagesLand LawsSarthak PageNo ratings yet

- U.P. Urban Buildings (Regulation of Letting, Rent and Eviction) Act, 1972Document25 pagesU.P. Urban Buildings (Regulation of Letting, Rent and Eviction) Act, 1972lokesh4nigamNo ratings yet

- Land Acquisition Act 1894Document56 pagesLand Acquisition Act 1894Umar HayatNo ratings yet

- Rajasthan Rent Control Act 2001 With AmendmentsDocument26 pagesRajasthan Rent Control Act 2001 With AmendmentsQuid NuncNo ratings yet

- The Land Acquisition Act 1894Document27 pagesThe Land Acquisition Act 1894Badri NathNo ratings yet

- The Land Acquisition Act. 1894 (Act I of 1894) Part-I Preliminary SectionsDocument43 pagesThe Land Acquisition Act. 1894 (Act I of 1894) Part-I Preliminary SectionsRizwan MughalNo ratings yet

- 6 The Himachal Pradesh Urban Rent Control, Act, 1987Document24 pages6 The Himachal Pradesh Urban Rent Control, Act, 1987pardeep bainsNo ratings yet

- RFCTLARR Act (Amendment) Ordinance, 2015 PDFDocument4 pagesRFCTLARR Act (Amendment) Ordinance, 2015 PDFgvmaheshNo ratings yet

- The Land Acquisition (Amendment) Bill, 2007: O BE Introduced IN OK AbhaDocument29 pagesThe Land Acquisition (Amendment) Bill, 2007: O BE Introduced IN OK Abhaanshul14346No ratings yet

- Hrera - AiplDocument3 pagesHrera - Aiplcreative.aghiNo ratings yet

- Registration (Amendment) Bill 2013 - Bill No XLVII of 2013 As Introduced in Rajya SabhaDocument21 pagesRegistration (Amendment) Bill 2013 - Bill No XLVII of 2013 As Introduced in Rajya Sabharkjayakumar7639No ratings yet

- Detroit City Charter (With Commentary)Document145 pagesDetroit City Charter (With Commentary)Stephen BoyleNo ratings yet

- IFA AssignmentDocument5 pagesIFA AssignmentAdnan JawedNo ratings yet

- Taxpayer Registration FormDocument3 pagesTaxpayer Registration Formmuhammad ihtishamNo ratings yet

- CT Onboarding Research Results and Datasheet - Cathcart RailDocument52 pagesCT Onboarding Research Results and Datasheet - Cathcart RailAdrian Christopher JuntillaNo ratings yet

- Cir v. ST Luke's Medical Center Inc. GR No. 195909Document11 pagesCir v. ST Luke's Medical Center Inc. GR No. 195909Joshua RodriguezNo ratings yet

- The Informal Economy - Portes Haller 2004Document23 pagesThe Informal Economy - Portes Haller 2004Martin RiveroNo ratings yet

- Estate TaxDocument32 pagesEstate TaxANDREA SEVERINONo ratings yet

- Federal Reserve Notes Are Not MoneyDocument3 pagesFederal Reserve Notes Are Not Moneyin1or100% (4)

- URA V Siraje Hassan Kajura Supreme CourtDocument7 pagesURA V Siraje Hassan Kajura Supreme CourtMusiime Katumbire Hillary50% (2)

- Indian Income Tax Return Acknowledgement 2022-23: Assessment YearDocument1 pageIndian Income Tax Return Acknowledgement 2022-23: Assessment YearShivi ChaurasiaNo ratings yet

- Agenda 21, Club of Rome and Origins of AGWDocument5 pagesAgenda 21, Club of Rome and Origins of AGWevelynvdr100% (4)

- Module 06: Contemporary Economic Issues Facing The Filipino EntrepreneurDocument9 pagesModule 06: Contemporary Economic Issues Facing The Filipino EntrepreneurChristian ZebuaNo ratings yet

- Employment: Complete An Employment' Page For Each Employment or DirectorshipDocument2 pagesEmployment: Complete An Employment' Page For Each Employment or DirectorshipDick WilliamsNo ratings yet

- Need A Business IdeaDocument14 pagesNeed A Business IdeawqewqewrewNo ratings yet

- Transformation of Consumer Buying Behaviour From Unorganised To Organised RetailingDocument87 pagesTransformation of Consumer Buying Behaviour From Unorganised To Organised Retailingshipra kalaNo ratings yet

- An Introduction To EnterprishipDocument14 pagesAn Introduction To EnterprishipNigel A.L. BrooksNo ratings yet

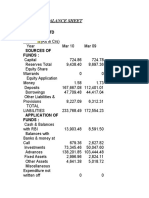

- Balance Sheet: JK Cement LTDDocument3 pagesBalance Sheet: JK Cement LTDHimanshu SharmaNo ratings yet

- United States Statutes at LargeDocument33 pagesUnited States Statutes at Largewealth2520100% (5)

- Unit 1 Notes TaxDocument14 pagesUnit 1 Notes TaxSuryansh MunjalNo ratings yet

- Project Proposal Amusement ParkDocument37 pagesProject Proposal Amusement ParkAjay B Nambiar100% (5)

- BPLS Survey Presentation LMP Agoo La Union Jan 26 2018Document57 pagesBPLS Survey Presentation LMP Agoo La Union Jan 26 2018Jane Tadina FloresNo ratings yet

- A Section Tues 11-07-17Document32 pagesA Section Tues 11-07-17Jacob LevaleNo ratings yet

- Insights Into Issues: BREXIT and Its ImpactDocument12 pagesInsights Into Issues: BREXIT and Its ImpactGSWALIANo ratings yet

- The Horrible Housing Blunder - The West's Biggest Economic Policy Mistake - Leaders - The EconomistDocument7 pagesThe Horrible Housing Blunder - The West's Biggest Economic Policy Mistake - Leaders - The Economist0wongNo ratings yet

- Street of Walls - Private Equity Training GuideDocument54 pagesStreet of Walls - Private Equity Training GuideJamesNo ratings yet

- The National Internal Revenue Code of The PhilippinesDocument154 pagesThe National Internal Revenue Code of The PhilippinesRuzzel Diane Irada OducadoNo ratings yet

- Labour Recruitment Methods in Zimbabwe During Colonial PeriodDocument15 pagesLabour Recruitment Methods in Zimbabwe During Colonial Periodlio chidausheNo ratings yet

- Bill of Rights, Section 20Document3 pagesBill of Rights, Section 20Iris Anthonniette SungaNo ratings yet

- HardestMath 2019 Challenge1 AnswersDocument1 pageHardestMath 2019 Challenge1 AnswersEffNowNo ratings yet

- P1 2ND Preboard PDFDocument9 pagesP1 2ND Preboard PDFmaria evangelistaNo ratings yet