UNIVERSITY CASEBOOK SERIES®

ANTITRUST LAW AND

TRADE REGULATION

CASES AND MATERIALS

SEVENTH EDITION

A. Dou@Las MELAMED

Professor of the Practice of Law,

Stanford Law School

Ranpat C. PICKER

‘James Parkor Hall Distinguished Service Professor of Law,

University of Chicago Lav School

PHILIP J. WEISER

Hattield Professor of Law and Telecommunications,

Dean Bmeritus, and Bxective Director of the

Silicon Flatiron Center for Law, Technology,

tnd Entrepreneurship

University of Colorado Law Schoo!

DIANE P. Woop

Chief Cireuit Judge, U.S. Court of Appeals,

Seventh Circuit

Senior Lecturer in Law,

University of Chicago Law Schoo!

FOUNDATION

PRESS

CHAPTER 2

MARKET POWER AND THE

MEANING OF COMPETITION

1. Market Power

2, The Limits of Permissible Competition

8, The Challongos of Applying the Antitrust Law (and the Concept of

Market Power)

1. MARKET POWER

A. MARKET POWER: DEFINITION AND SIGNIFICANCE

‘Market power is one of the most basic notions in antitrust, but that

does not mean that it is well understood or that itis easy to convey what

is at stake, The most natural path, we think, and the one that we will

follow, is to start with the absence of market power—a competitive

situation—and with that as the baseline, build up @ notion of mariet

power as a deviation from competitive conditions.

1. AN INPRODUCTION To THE ECONOMICS OF COMPETITION AND

‘MONOPOLY

‘The most basic tool in antitrust economics is the demand curve,

Demand curves can be either for a particular individual or for a group of

individuals or for even the economy as a whole. A demand curve

represents the willingness of the covered individuals to pay for the good

in question, And the most basic property of demand curves is that

consumers want more of the good as it becomes less expensive,

Consumers will buy more cases of Diet Coke at $3.99 than they will at

$4.25, That is true both because some individual consumers will buy

more Diet Coke at a lower price and because some consumers will not

buy any Diet Coke at the higher price. Put differently, demand curves

slope down, When economists say that—and they do say that with some

frequency—they have in mind the idea of a graph with price on the Y-

axis and quantity on the X-axis. High prices imply low quantities, and

low prices imply high quantities. Demand curves slope down. This is

illustrated by Figure 2.1.

1

o Manion Power AND THE MEANING OF ComPurrrioN Cuarren 2

$2___Manuer Powen aun Tu Mean or Cowrermon ____—Ciarren

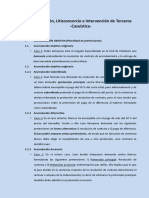

Demand Curve

10

In Figure 2.1, the vertical axis, labeled P, shows the unit price for

the product at issue, in this ease Diet Coke. ‘The horizontal axis, labeled

Q, shows the number of units of the product. The demand eurve, which

is typically labeled D, shows the number of units that consumers are

willing to buy at each price. Ifthe price is 10, eonsumers are not willing

to buy any units, They are willing to buy some number of units (1 unit in

Figure 2.1) ifthe price is 9, a larger number (2 in Figure 2.1) if the price

is 8, and 60 on, Another way of putting the point is that the demand curve

depicted in Figure 2.1 shows that consumers are willing to pay up to 9,

but no more, for the first unit of Diet Coke, up to 8 for the second unit,

tand so on. As we will see, however, the actual price that consumers will,

have to pay might be less than those shown on the demand curve.

a. Competitive Markets

Demand curves are important because they help frame how to think

about competitive markets. In a competitive market, goods are produced

80 long as consumers are willing to pay for those goods amounts that

‘excoed the cost af creating those goods. There is quite a bit embedded in

‘that statement. This is not an abstract statement about how much a

given consumer might enjoy consuming a particular good. Instead, it

focuses on the willingness of a consumer to pay for a good and, in doing

0, it focuses on the ability of that consumer to pay for the good. When

wwe think ahout competitive markets, we take demand curves as a given

and then assess how goods are produced relative to that demand eurve.

‘The stylized version of a competitive market assumes that producers

are each relatively small and each believes that it is a price-taker. That

means that each believes that the final price for the good is set by the

“market” and that its production is too small to influence that price. That

‘makes decision-making for the firm quite simple, If the current market

price excoeds its marginal cost—that is, the cost of making the next unit

of the good—the firm should make move units of the good. Put numbers

sscri0Nt Manes Powsn

on that. If the current market price ig $6 and the firm can make

additional units for $4, it will make a profit of $2 on the next uni: that it

eroates. And it should do that as fast as it can and make as many as

possible.

Of course, each firm is in the same position, and the only way for all,

of them in the aggregate to sell more of the good in question than the

amount they could sell at a price of $6 is for priee to go down. Why?

Demand eurves slope down. Consumers will take more of the good only if

the price goes down. That should start to make clear the dynamics of

‘competition at work here and the natural result of that outcome. In a

competitive market, if all of the firms that can make units for $4 keep

making units as long as the price excaeds $4, the price will decline until

it equals $4. Now, let's flip the facts and consider the opposing situation,

If the current market price of the good is $2 and it costs $4 to produce

each unit of the good, the firm should cut production because at the

current price it would lose $2 per unit. As each firm cuts production,

overall output will drop; and again, because demand curves slope down,

the market price of the good will rise as production drops until the price

equals marginal cost. Thus, in a competitive market, price equals

marginal cost. This is illustrated by Figure 2.2.

Stop to consider the beauty of what just took place. Producers

produce goods as long as consumers are willing to pay for them, No

consumer who is willing to pay more than it costs to create the next unit,

of the good is left unsatisfied. And no producer makes a good that isn't

‘covered by what a consumer is willing to pay for it. It costs one producer

more to make the good than it costs another producer, only the low cost.

Producer will keep producing the good and selling it at the low price. A

‘competitive economy is said to be economically efficient in that () enough

‘output is produced to satisfy all the demand of eonsumera who value the

product in excess of its cost of production (“allocative efficiency”) and Gi)

output is produced at minimum cost (“productive efficiency’)

Let's take a closer look at Figure 2.2. The point of an example like

the one set out in Figure 2.1 is to remove much of the complexity of the

real world to allow the core points to stand out. The idea that damand

‘curves slope down is captured in a simple equation P = 10-Q. Just put

4 few numbers in that to see what happens. At a price of 2—

You might also like

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5813)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- Becker Gary - La Naturaleza de La CompetenciaDocument10 pagesBecker Gary - La Naturaleza de La CompetenciaAlexa CNo ratings yet

- Gunnar Niels y Otros - Some Health Warnings On CompetitionDocument4 pagesGunnar Niels y Otros - Some Health Warnings On CompetitionAlexa CNo ratings yet

- Gunnar Niels y Otros - Some Health Warnings On CompetitionDocument4 pagesGunnar Niels y Otros - Some Health Warnings On CompetitionAlexa CNo ratings yet

- El Derecho Registral Inmobiliario y El Registro de La PropiedadDocument50 pagesEl Derecho Registral Inmobiliario y El Registro de La PropiedadAlexa CNo ratings yet

- TARUFFO, Michele. La Prueba. Tipos de PruebasDocument27 pagesTARUFFO, Michele. La Prueba. Tipos de PruebasAlexa CNo ratings yet

- Documento 7Document1 pageDocumento 7Alexa CNo ratings yet

- Niels Gunnar - 8. Explaining Some Basic Principles The Economic Naturalists WayDocument6 pagesNiels Gunnar - 8. Explaining Some Basic Principles The Economic Naturalists WayAlexa CNo ratings yet

- Conta UltimoDocument20 pagesConta UltimoAlexa CNo ratings yet

- Casación Laboral #10491-2015-Junín-Perjuicio A La Integridad FísicaDocument9 pagesCasación Laboral #10491-2015-Junín-Perjuicio A La Integridad FísicaAlexa CNo ratings yet

- Medios de ExtincionDocument19 pagesMedios de ExtincionAlexa CNo ratings yet

- S 4,9 y 14 ProcesosDocument13 pagesS 4,9 y 14 ProcesosAlexa CNo ratings yet

- Impuesto A La Renta - TimanáDocument27 pagesImpuesto A La Renta - TimanáAlexa CNo ratings yet

- Imputación de Pagos Parciales - EjerciciosDocument1 pageImputación de Pagos Parciales - EjerciciosAlexa CNo ratings yet

- Mir Puig. Estructura Del DelitoDocument7 pagesMir Puig. Estructura Del DelitoAlexa CNo ratings yet

- Esquemas ProcedimentalesDocument10 pagesEsquemas ProcedimentalesAlexa CNo ratings yet

- Brochure - Evento Derecho Inmobiliario y RegistralDocument10 pagesBrochure - Evento Derecho Inmobiliario y RegistralAlexa CNo ratings yet

- ALFARO, Luis. Casos Sobre Acumulación, Litisconsorcio e Intervención de Terceros.Document7 pagesALFARO, Luis. Casos Sobre Acumulación, Litisconsorcio e Intervención de Terceros.Alexa CNo ratings yet

- BERDUGO, Ignacio (69-87)Document10 pagesBERDUGO, Ignacio (69-87)Alexa CNo ratings yet

- Caso Edwin SierraDocument9 pagesCaso Edwin SierraAlexa CNo ratings yet