0% found this document useful (0 votes)

367 views4 pagesAlgobaba ORB Trading Script

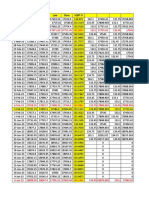

This strategy uses a moving average crossover technique to generate buy and sell signals for an intraday trading strategy. It defines inputs for trade direction, options vs futures, strike type, quantity, session times, profit/loss levels. On signals, it places orders to enter long/short positions and exits them at target or stop levels using the Algobaba platform.

Uploaded by

Abdul KalamCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as TXT, PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

367 views4 pagesAlgobaba ORB Trading Script

This strategy uses a moving average crossover technique to generate buy and sell signals for an intraday trading strategy. It defines inputs for trade direction, options vs futures, strike type, quantity, session times, profit/loss levels. On signals, it places orders to enter long/short positions and exits them at target or stop levels using the Algobaba platform.

Uploaded by

Abdul KalamCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as TXT, PDF, TXT or read online on Scribd