You might also like

- Principle of TaxationDocument27 pagesPrinciple of TaxationkelvinplayzgamesNo ratings yet

- Abft1024 T2 - LtyDocument2 pagesAbft1024 T2 - Ltylfc778No ratings yet

- CH 2Document29 pagesCH 2syahirahNo ratings yet

- Dec20 QQ PDFDocument16 pagesDec20 QQ PDFSYAZWINA SUHAILINo ratings yet

- T2 Taxpayer Resident StatusDocument5 pagesT2 Taxpayer Resident StatusCHAN KER XINNo ratings yet

- Tax 1 RevisionDocument14 pagesTax 1 RevisionSoon Mei QiNo ratings yet

- t1q Rca2 Ya2020 Intro & RDocument2 pagest1q Rca2 Ya2020 Intro & RHaananth SubramaniamNo ratings yet

- T1Q Introduction & RSDocument9 pagesT1Q Introduction & RS吕仙姿No ratings yet

- Chapter 2 Residence Status of IndividualsDocument48 pagesChapter 2 Residence Status of IndividualsHazlina HusseinNo ratings yet

- Resident Status Q3Document3 pagesResident Status Q3Zale EzekielNo ratings yet

- Chapter 2 - Residence Status For Individual - JAN 2019 PDFDocument40 pagesChapter 2 - Residence Status For Individual - JAN 2019 PDF유장하100% (1)

- Tutorial 1 & 2 - Intro - RSDocument4 pagesTutorial 1 & 2 - Intro - RSnurinatihani24No ratings yet

- Tax467, Tax 267 Practice QuestionsDocument4 pagesTax467, Tax 267 Practice QuestionsRISNATUL UZMA HELMI RIZALNo ratings yet

- Personal Taxation Final QuestionsDocument5 pagesPersonal Taxation Final QuestionsKarthik RamanathanNo ratings yet

- Taxation Chapter TwoDocument21 pagesTaxation Chapter TwoHazlina HusseinNo ratings yet

- Week 2 - Resident StatusDocument9 pagesWeek 2 - Resident Statussam_suhaimiNo ratings yet

- Topic 2 Resident Status For IndividualDocument23 pagesTopic 2 Resident Status For IndividualTeh Chu LeongNo ratings yet

- Tutorial 1 - BP - Q A 21.3.2022Document3 pagesTutorial 1 - BP - Q A 21.3.2022KVTNo ratings yet

- Tutorial 2 QDocument4 pagesTutorial 2 QrajarajeswryNo ratings yet

- Chapter 2 Determination of Residence StatusDocument27 pagesChapter 2 Determination of Residence Statuswaniy amaniNo ratings yet

- Tutorial 1Document36 pagesTutorial 1yyyNo ratings yet

- Chapter 2 Residence StatusDocument9 pagesChapter 2 Residence StatusLOO YU HUANGNo ratings yet

- Tax Chap4Document12 pagesTax Chap4Dik Ah SholehahNo ratings yet

- Q & A Marathon DT Question Bank Part 1Document181 pagesQ & A Marathon DT Question Bank Part 1Gagan SahuNo ratings yet

- Chapter 2 Resident StatusDocument35 pagesChapter 2 Resident StatusNivaashene SaravananNo ratings yet

- 2 Topic2 Residence StatusDocument19 pages2 Topic2 Residence StatusIskandar Zulkarnain KamalluddinNo ratings yet

- Residential StatusDocument4 pagesResidential StatusShaji KuttyNo ratings yet

- Didier Permanent ResidencyDocument3 pagesDidier Permanent ResidencyDidier G PeñuelaNo ratings yet

- Tutorial Resident StatusDocument2 pagesTutorial Resident StatusSyamimi AqilahNo ratings yet

- Tutorial 1 RSDocument2 pagesTutorial 1 RSateen rizalmanNo ratings yet

- Chap 2 - Residence StatusDocument40 pagesChap 2 - Residence StatusIfa Chan100% (1)

- Chapter 2 Resident Status A 202Document33 pagesChapter 2 Resident Status A 202ateen rizalmanNo ratings yet

- Residential Status Problems 2021-2022-1Document5 pagesResidential Status Problems 2021-2022-120-UCO-517 AJAY KELVIN ANo ratings yet

- Resident Status For IndividualDocument24 pagesResident Status For IndividualMalabaris Malaya Umar SiddiqNo ratings yet

- Tax267 February 22 FaDocument13 pagesTax267 February 22 FarumaisyaNo ratings yet

- Sep 2014 N12M01 - Workshop 1Document3 pagesSep 2014 N12M01 - Workshop 1analsluttyNo ratings yet

- Tutorial 2 Topic 2: Residence Status of IndividualsDocument3 pagesTutorial 2 Topic 2: Residence Status of Individualsfujinlim98No ratings yet

- Practice QuestionsDocument133 pagesPractice QuestionsSarath KumarNo ratings yet

- Arrear JosephDocument1 pageArrear JosephChief Of AuditNo ratings yet

- Topic 2 - Resident StatusDocument31 pagesTopic 2 - Resident StatusEmelyn NurShahiraNo ratings yet

- Tax July 2021Document4 pagesTax July 2021MUHAMMAD FARIS NAIMNo ratings yet

- July21 QQ PDFDocument4 pagesJuly21 QQ PDFSYAZWINA SUHAILINo ratings yet

- Practice QuestionsDocument134 pagesPractice QuestionsKarthikNo ratings yet

- CH2 - Residence StatusDocument40 pagesCH2 - Residence Status謝中豪No ratings yet

- Feb2022 Tax267Document9 pagesFeb2022 Tax267Ayu MaisarahNo ratings yet

- Tax267 Jul2022 QQDocument9 pagesTax267 Jul2022 QQLENNY GRACE JOHNNIENo ratings yet

- Unit 3 Residential StatusDocument41 pagesUnit 3 Residential Status24.7upskill Lakshmi V100% (3)

- Fac22a2 SuppDocument11 pagesFac22a2 Suppsacey20.hbNo ratings yet

- Tutorial 3: Employment and Personal Taxation: Universiti Tunku Abdul Rahman Faculty of Business and FinanceDocument2 pagesTutorial 3: Employment and Personal Taxation: Universiti Tunku Abdul Rahman Faculty of Business and FinanceKAY PHINE NGNo ratings yet

- Jan22 QQ PDFDocument5 pagesJan22 QQ PDFSYAZWINA SUHAILINo ratings yet

- Jan 2023Document13 pagesJan 2023Aina OyenNo ratings yet

- 6411presenta 11 2022Document59 pages6411presenta 11 2022Anime FlicksNo ratings yet

- Faculty - Accountancy - 2022 - Session 1 - Degree - Tax467Document9 pagesFaculty - Accountancy - 2022 - Session 1 - Degree - Tax467HAZIQ HASNOLNo ratings yet

- T03 - Source of IncomeDocument10 pagesT03 - Source of Incometing ting shihNo ratings yet

- Chapter 2 Residential StatusDocument6 pagesChapter 2 Residential StatusGrave diggerNo ratings yet

- Topic 2 Residence Status For IndividualDocument23 pagesTopic 2 Residence Status For IndividualHANIS IZYAN MAT ISANo ratings yet

- Income Tax Divyastra CH 1 Residential Status RDocument9 pagesIncome Tax Divyastra CH 1 Residential Status RCRO0658286 DEEPANSHU GOYALNo ratings yet

- Alvin Chan QADocument4 pagesAlvin Chan QAkelly yuNo ratings yet

- ACC2054 MTS Tutorial 9 QDocument3 pagesACC2054 MTS Tutorial 9 QTharvind KumarNo ratings yet

- Transforming Bangladesh’s Participation in Trade and Global Value ChainFrom EverandTransforming Bangladesh’s Participation in Trade and Global Value ChainNo ratings yet

- E-Way MH Challan-14Document1 pageE-Way MH Challan-14Sunil GuptaNo ratings yet

- Tax Crimes (MCJ 405-Economic Crimes)Document11 pagesTax Crimes (MCJ 405-Economic Crimes)Han WinNo ratings yet

- CH 12Document44 pagesCH 12kevin echiverriNo ratings yet

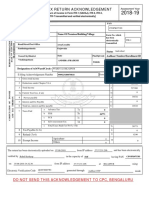

- Indian Income Tax Return Acknowledgement: Name of Premises/Building/VillageDocument1 pageIndian Income Tax Return Acknowledgement: Name of Premises/Building/VillageRahul KashyapNo ratings yet

- OnlinePayslipInquire Pages NewPayslipModuleDocument1 pageOnlinePayslipInquire Pages NewPayslipModuleArlene D. Panaligan44% (52)

- Salary SchemeDocument2 pagesSalary SchemeMichelle Acebuche SibayanNo ratings yet

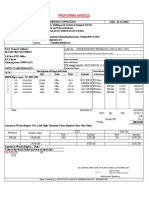

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Deepjyoti DasNo ratings yet

- E-Way Bill System - PDF 32 PDFDocument1 pageE-Way Bill System - PDF 32 PDFNirav MehtaNo ratings yet

- Final Computaion For Government OfficeDocument24 pagesFinal Computaion For Government OfficeGagan Deep PathakNo ratings yet

- Salary Slip (31837722 February, 2019) PDFDocument1 pageSalary Slip (31837722 February, 2019) PDFUsman AwanNo ratings yet

- Gross Income 2b Received by or Accrued NotesDocument27 pagesGross Income 2b Received by or Accrued Notestumonekongo02No ratings yet

- June2019260313FORM13 PDFDocument2 pagesJune2019260313FORM13 PDFdpo bathindaNo ratings yet

- Robinsons Daiso v. CIRDocument35 pagesRobinsons Daiso v. CIRaudreydql5No ratings yet

- FIN623 Midterm Subjective By:::: Usman Attari: Rules To Prevent Double Derivation and Double Deductions: Section 73Document10 pagesFIN623 Midterm Subjective By:::: Usman Attari: Rules To Prevent Double Derivation and Double Deductions: Section 73SunitaNo ratings yet

- Nirlaba JawabDocument7 pagesNirlaba JawabVerel HaikalNo ratings yet

- Audit Checklist For Goods and Services TaxDocument4 pagesAudit Checklist For Goods and Services Taxmani1970% (1)

- Research Paper On Tax Evasion in IndiaDocument7 pagesResearch Paper On Tax Evasion in Indiahjuzvzwgf100% (1)

- Practice Problems On Incidence of TaxDocument3 pagesPractice Problems On Incidence of TaxPratik DesaiNo ratings yet

- Nursery Care Corp. vs. AcevedoDocument1 pageNursery Care Corp. vs. AcevedoLouana AbadaNo ratings yet

- Cases On TaxationDocument13 pagesCases On TaxationPeanutButter 'n JellyNo ratings yet

- W-8BEN QRG enDocument8 pagesW-8BEN QRG enKen McLeanNo ratings yet

- Budget1 Taxation Upto GSTDocument37 pagesBudget1 Taxation Upto GSTbhavyaNo ratings yet

- Srisri Pilymer PI16122022-1Document1 pageSrisri Pilymer PI16122022-1GNANA CHARAN GNo ratings yet

- 3 Months Study Plan With A, B, C Analysis CS Executive Dec-23 Old SyllabusDocument42 pages3 Months Study Plan With A, B, C Analysis CS Executive Dec-23 Old SyllabusGungun ChetaniNo ratings yet

- Analysis of Rates For Pacca Brick WorkDocument1 pageAnalysis of Rates For Pacca Brick WorkMujahid ChishtiNo ratings yet

- Excise & Taxation Department, IslamabadDocument5 pagesExcise & Taxation Department, IslamabadAbeeha RajpootNo ratings yet

- IT Returns 2021-22Document3 pagesIT Returns 2021-22srinivas maguluriNo ratings yet

- Accrued Liabilities H Pengantar Praktik PengauditanDocument6 pagesAccrued Liabilities H Pengantar Praktik PengauditanArika KameliaNo ratings yet

- Invoice 2 PDFDocument1 pageInvoice 2 PDFPurva TiwariNo ratings yet

- NINJA Notes - Individual TaxationDocument26 pagesNINJA Notes - Individual TaxationMahesh Toppae100% (1)