You might also like

- Building An Investment ThesisDocument11 pagesBuilding An Investment ThesisJack Jacinto100% (2)

- Value Investing: The Buffett Techniques Of Accumulating Wealth With Practical Strategies To Always Choose The Intelligent InvestmentFrom EverandValue Investing: The Buffett Techniques Of Accumulating Wealth With Practical Strategies To Always Choose The Intelligent InvestmentRating: 4.5 out of 5 stars4.5/5 (39)

- Game TheoryDocument29 pagesGame TheoryPraveen YadavNo ratings yet

- A Framework For Defining Negotiation GoalsDocument5 pagesA Framework For Defining Negotiation Goalscalibr8torNo ratings yet

- Mauboussin - The Importance of ExpectationsDocument17 pagesMauboussin - The Importance of Expectationsjockxyz100% (1)

- Chaikin Money Flow Vs Chaikin OccilatorDocument12 pagesChaikin Money Flow Vs Chaikin Occilatorhaseeb100% (1)

- What Is Value Investing?Document10 pagesWhat Is Value Investing?Navaraj BaniyaNo ratings yet

- Halifax Statement 2023 08 18Document4 pagesHalifax Statement 2023 08 18VALENTIN SHABLIKANo ratings yet

- The Companies Act, 2013 - MCQ On Business Law With Answers - GST Guntur PDFDocument6 pagesThe Companies Act, 2013 - MCQ On Business Law With Answers - GST Guntur PDFJITENDER KUMARNo ratings yet

- 2012.08.21 - The Importance of Expectations - That Question That Bears Repeating - What's Priced in PDFDocument17 pages2012.08.21 - The Importance of Expectations - That Question That Bears Repeating - What's Priced in PDFbrineshrimpNo ratings yet

- Securities Regulations Code - Ra 8799Document28 pagesSecurities Regulations Code - Ra 8799Jave MagsaNo ratings yet

- Valuation Concepts and Methods Introduction To ValuationDocument18 pagesValuation Concepts and Methods Introduction To ValuationPatricia Nicole BarriosNo ratings yet

- Notes Lecture IIDocument2 pagesNotes Lecture IICigdemSahinNo ratings yet

- Understanding Bid-Ask SpreadDocument3 pagesUnderstanding Bid-Ask SpreadKidMonkey2299No ratings yet

- Tutorial 10 To PrintDocument1 pageTutorial 10 To PrintNora CaramellaNo ratings yet

- Hubris HypothesisDocument5 pagesHubris HypothesisGaurav RathaurNo ratings yet

- Google Ipo ProjectDocument21 pagesGoogle Ipo ProjectRobert Taylor0% (1)

- Methods Estimate Value by Luca CapitalDocument24 pagesMethods Estimate Value by Luca CapitalDũng NguyễnNo ratings yet

- 3.3 Underpricing and Entrepreneurial Wealth Losses in IPOs Theory and EvidenceDocument14 pages3.3 Underpricing and Entrepreneurial Wealth Losses in IPOs Theory and Evidenceمحمد ابوشريفNo ratings yet

- To Valuation Concepts: by Sarah M. Balisacan, CPADocument12 pagesTo Valuation Concepts: by Sarah M. Balisacan, CPAardee esjeNo ratings yet

- Chapter 8: Implications of Heuristics and Biases For Financial Decision-MakingDocument10 pagesChapter 8: Implications of Heuristics and Biases For Financial Decision-MakingRobinson MojicaNo ratings yet

- Value Investing ReportDocument4 pagesValue Investing ReportPrincess Joy Andayan BorangNo ratings yet

- First Law of DemandDocument23 pagesFirst Law of DemandMaiXuanPhamNo ratings yet

- The Winner's CurseDocument2 pagesThe Winner's Curseharshull27100% (1)

- Example of Real Rate of Return FormulaDocument19 pagesExample of Real Rate of Return FormulasahilkuNo ratings yet

- Bid-Ask, Limit Orders, and Margin CallsDocument15 pagesBid-Ask, Limit Orders, and Margin CallsAriful Haidar MunnaNo ratings yet

- Ten Rules For Bargaining Success. You Do Not Have To Use A: 6.1 Rule 1: Be PreparedDocument18 pagesTen Rules For Bargaining Success. You Do Not Have To Use A: 6.1 Rule 1: Be PreparedO KiNo ratings yet

- Activity 2 FinalsDocument8 pagesActivity 2 FinalsChaermalyn Bao-idangNo ratings yet

- 1-1 RMET Dacio, Anthony John Act # 17Document2 pages1-1 RMET Dacio, Anthony John Act # 17Anthony John DacioNo ratings yet

- Behavioral Finance (I)Document6 pagesBehavioral Finance (I)CigdemSahinNo ratings yet

- Syndicates in IPOsDocument3 pagesSyndicates in IPOsSamin SakibNo ratings yet

- SFM DescriptiveDocument3 pagesSFM DescriptiveZeeshan SikandarNo ratings yet

- Artical 1 New-CFDocument4 pagesArtical 1 New-CFiitebaNo ratings yet

- C30CY Week 4 Lecture - CanvasDocument54 pagesC30CY Week 4 Lecture - Canvasjohnshabin123No ratings yet

- An Introduction To Business ValuationDocument20 pagesAn Introduction To Business ValuationMurat SyzdykovNo ratings yet

- The Warren Buffett Way: High Quality Stocks in Emerging MarketsDocument10 pagesThe Warren Buffett Way: High Quality Stocks in Emerging MarketsCm ShegrafNo ratings yet

- Buyers, Companies Must Invest in Relationship Building and Customer IntimacyDocument4 pagesBuyers, Companies Must Invest in Relationship Building and Customer IntimacyJed DagotNo ratings yet

- Explain What A Preemptive Rights Offering Is With Example and Why A Standby Underwriting Arrangements May Be Needed. Also, Define Subscription PriceDocument4 pagesExplain What A Preemptive Rights Offering Is With Example and Why A Standby Underwriting Arrangements May Be Needed. Also, Define Subscription PriceuzairNo ratings yet

- Lesson 1 Notes: Foundation ProgrammeDocument11 pagesLesson 1 Notes: Foundation ProgrammeMarijan blaževićNo ratings yet

- Managerial Performance Tobins Q 2Document18 pagesManagerial Performance Tobins Q 2Pepper CorianderNo ratings yet

- Reacting To CompetitionDocument3 pagesReacting To CompetitionPat DomingoNo ratings yet

- Ranchi - Lecture On Value InvestingDocument45 pagesRanchi - Lecture On Value InvestingTran Ngan HoangNo ratings yet

- Options & Different Strategies of Options RBA: Contact: Jibransheikh@comsats - Edu.pkDocument19 pagesOptions & Different Strategies of Options RBA: Contact: Jibransheikh@comsats - Edu.pkjim125No ratings yet

- Merger & Acquisition: Defences Against Unwelcome TakeoversDocument22 pagesMerger & Acquisition: Defences Against Unwelcome TakeoversViraj GawandeNo ratings yet

- Underpricing of IPOsDocument4 pagesUnderpricing of IPOsSamin SakibNo ratings yet

- The Price of RiskDocument15 pagesThe Price of Riskomkar kothuleNo ratings yet

- Introduction To ValuationDocument5 pagesIntroduction To ValuationRG VergaraNo ratings yet

- Negotiation Notes at Bec DomsDocument49 pagesNegotiation Notes at Bec DomsBabasab Patil (Karrisatte)No ratings yet

- 5 Must-Have Metrics For Value InvestorsDocument6 pages5 Must-Have Metrics For Value InvestorstthorgalNo ratings yet

- Definition of 'Stop-Loss Order'Document25 pagesDefinition of 'Stop-Loss Order'Siddharth MehtaNo ratings yet

- Session 7 Pricing PolicyDocument30 pagesSession 7 Pricing PolicySakshi ShahNo ratings yet

- Case StudyDocument7 pagesCase StudyJoyNo ratings yet

- UNIT-III-Cost & Pricing Methods in Managerial EconomicsDocument19 pagesUNIT-III-Cost & Pricing Methods in Managerial EconomicsBrijlal MallikNo ratings yet

- Derivatives ManagementDocument13 pagesDerivatives ManagementMaharajascollege KottayamNo ratings yet

- Chapter 06Document20 pagesChapter 06যুবরাজ মহিউদ্দিনNo ratings yet

- Corporate Finance - Mergers and Acquisitions - Financing Issues - Dayana MasturaDocument11 pagesCorporate Finance - Mergers and Acquisitions - Financing Issues - Dayana MasturaDayana MasturaNo ratings yet

- Frederick 111018Document45 pagesFrederick 111018robertNo ratings yet

- Settlement RangeDocument2 pagesSettlement RangesvrmbabuNo ratings yet

- Twelve Ways To Detect Bid-Rigging CartelsDocument4 pagesTwelve Ways To Detect Bid-Rigging CartelsDilip SinghNo ratings yet

- Market Valuation and Merger Waves: Matthew Rhodes-Kropf and S. ViswanathanDocument34 pagesMarket Valuation and Merger Waves: Matthew Rhodes-Kropf and S. ViswanathanR. Shyaam PrasadhNo ratings yet

- The Right Game: Use Game Theory To Shape StrategyDocument18 pagesThe Right Game: Use Game Theory To Shape StrategywitheredwhiteNo ratings yet

- L2 - Distributive BargainingDocument9 pagesL2 - Distributive BargainingShazia Nawaz BajwaNo ratings yet

- Final NotesDocument2 pagesFinal Notesdaksh.aggarwal26No ratings yet

- PMS - CompetitionDocument9 pagesPMS - Competitionstd29925No ratings yet

- WK 1.1 - Intro To Corporate FinanceDocument17 pagesWK 1.1 - Intro To Corporate Financehfmansour.phdNo ratings yet

- WK 3.1 - Financial Statement & Ratio AnalysisDocument12 pagesWK 3.1 - Financial Statement & Ratio Analysishfmansour.phdNo ratings yet

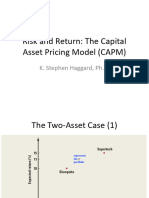

- WK 6.2 - Risk and Return CAPMDocument18 pagesWK 6.2 - Risk and Return CAPMhfmansour.phdNo ratings yet

- WK 8.1 - Stock ValuationDocument20 pagesWK 8.1 - Stock Valuationhfmansour.phdNo ratings yet

- WK 2.2 - The Income StatementDocument7 pagesWK 2.2 - The Income Statementhfmansour.phdNo ratings yet

- WK 6.1 - Risk and Return of PortfoliosDocument15 pagesWK 6.1 - Risk and Return of Portfolioshfmansour.phdNo ratings yet

- WK 5 - NotesDocument6 pagesWK 5 - Noteshfmansour.phdNo ratings yet

- Lesson 7.1Document3 pagesLesson 7.1crisjay ramosNo ratings yet

- Describing Trends in Business 2023Document2 pagesDescribing Trends in Business 2023Cristian CastilloNo ratings yet

- PROJECT: Joining The Market: Required ResourcesDocument5 pagesPROJECT: Joining The Market: Required ResourcesAngel Enamorado0% (1)

- Bitcoin Price HistoryDocument3 pagesBitcoin Price HistoryFiras ZahmoulNo ratings yet

- Intermediate Accounting Vol 2 Canadian 3Rd Edition Lo Solutions Manual Full Chapter PDFDocument36 pagesIntermediate Accounting Vol 2 Canadian 3Rd Edition Lo Solutions Manual Full Chapter PDFmarcus.hartley804100% (15)

- Class 12 BST ProjectDocument12 pagesClass 12 BST ProjectKathan PatelNo ratings yet

- Probate InventoryDocument4 pagesProbate Inventoryacer paulNo ratings yet

- Samudera Indonesia TBK - 30 September 2023 - FinalDocument114 pagesSamudera Indonesia TBK - 30 September 2023 - Finalade.yulyansyahNo ratings yet

- Chapter 2 - Shares and Share CapitalDocument10 pagesChapter 2 - Shares and Share CapitalDaksh GandhiNo ratings yet

- V41 C05 611ungeDocument10 pagesV41 C05 611ungeZen TraderNo ratings yet

- IepfDocument2 pagesIepf15986No ratings yet

- Selling Price: $14.: Oven Type ADocument2 pagesSelling Price: $14.: Oven Type ANguyễn Thị Thu HiềnNo ratings yet

- FINA3020 Assignment3Document5 pagesFINA3020 Assignment3younes.louafiiizNo ratings yet

- Canary - 2023-02-18 170231.l505964Document53 pagesCanary - 2023-02-18 170231.l505964SAID k sNo ratings yet

- Chapter 2 Hyperinflation LectureDocument4 pagesChapter 2 Hyperinflation LectureChristine SondonNo ratings yet

- FRM Test 11 AnsDocument47 pagesFRM Test 11 AnsKamal BhatiaNo ratings yet

- Statement of Comprehensive Income: Basic Financial Statements IiDocument5 pagesStatement of Comprehensive Income: Basic Financial Statements IiEurica LimNo ratings yet

- Literature Review On Foreign Exchange RateDocument8 pagesLiterature Review On Foreign Exchange Rateafmzqlbvdfeenz100% (1)

- MSC B2B 01 - Intro Course - Topic 2019Document35 pagesMSC B2B 01 - Intro Course - Topic 2019Raghav BansalNo ratings yet

- Acctstmt LDocument2 pagesAcctstmt LNew Age InvestmentsNo ratings yet

- Question Papers Sem-2 2022Document16 pagesQuestion Papers Sem-2 2022sauravpatil24No ratings yet

- Initiating Coverage - Metro Brands Ltd. - 250722Document22 pagesInitiating Coverage - Metro Brands Ltd. - 250722Praveen PuniaNo ratings yet

- Agricultural Loan - Main ApplicationDocument4 pagesAgricultural Loan - Main ApplicationAbisheikNo ratings yet

- Q4 FY22 InfographicDocument1 pageQ4 FY22 InfographicawarialocksNo ratings yet

- Fin402 - Case Study - Muhammad Hafizuddin Bin Abdul Hamid (Am1809004713)Document16 pagesFin402 - Case Study - Muhammad Hafizuddin Bin Abdul Hamid (Am1809004713)Muhammad HafizuddinNo ratings yet

- Digital Marketing in Indian Context: April 2016Document7 pagesDigital Marketing in Indian Context: April 2016Kandukuri Varun VenkyNo ratings yet