You might also like

- BT Kiem ToanDocument5 pagesBT Kiem Toantrangnguyen.31221021691No ratings yet

- Business Processes - Part 1Document15 pagesBusiness Processes - Part 1Malinda NayanajithNo ratings yet

- Nature and Significance of Audit Evidence and Describe The Different Audit Procedures and TechniquesDocument3 pagesNature and Significance of Audit Evidence and Describe The Different Audit Procedures and TechniquesKristina De GuzmanNo ratings yet

- How Auditors Get Evidence: Substantive Testing - AssertionsDocument3 pagesHow Auditors Get Evidence: Substantive Testing - AssertionsSid TiglaoNo ratings yet

- CIS ReportDocument10 pagesCIS ReportMarieNo ratings yet

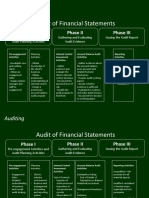

- Audit of Financial Statements: AuditingDocument3 pagesAudit of Financial Statements: AuditingAnjjjjNo ratings yet

- TOC - Cash On HandDocument1 pageTOC - Cash On HandMarie May Sese MagtibayNo ratings yet

- Chapter 3 - IcDocument3 pagesChapter 3 - IcHƯƠNG ĐỖ MINHNo ratings yet

- Please Differentiate Test of Controls and ControlDocument2 pagesPlease Differentiate Test of Controls and ControlHUONG DONG THI THUNo ratings yet

- Part 2 For StudentsDocument34 pagesPart 2 For StudentsLea JoaquinNo ratings yet

- Test of Control For Cash and Cash Equivalents - Cash On Hand and in BankDocument1 pageTest of Control For Cash and Cash Equivalents - Cash On Hand and in BankMarie May Sese MagtibayNo ratings yet

- Substantive Tests of Transactions and Balances: Learning ObjectivesDocument61 pagesSubstantive Tests of Transactions and Balances: Learning ObjectivesMatarintis A Zulqarnain IINo ratings yet

- Audit Procedures: Learning OutcomesDocument5 pagesAudit Procedures: Learning OutcomesKimberly parciaNo ratings yet

- Audit Objectives Techniques Assertions Procedures and TestsDocument14 pagesAudit Objectives Techniques Assertions Procedures and TestsNieza Marie MirandaNo ratings yet

- Lecture 7-Internal Control & AssertionsDocument6 pagesLecture 7-Internal Control & AssertionsFadil RushNo ratings yet

- Substantive Audit Procedures - Types - Examples - AccountinguideDocument3 pagesSubstantive Audit Procedures - Types - Examples - AccountinguideBennice 8No ratings yet

- Consideration of Internal ControlDocument4 pagesConsideration of Internal ControlFritzie Ann ZartigaNo ratings yet

- Jawaban Audit 16-25Document4 pagesJawaban Audit 16-25Lisca Nabilah50% (4)

- Sampc10le Ch10Document61 pagesSampc10le Ch10mynameisjcaa100% (1)

- Segregation of Duties Questionnaire - Controls For Significant Accounting ApplicationsDocument6 pagesSegregation of Duties Questionnaire - Controls For Significant Accounting ApplicationsKalyanNo ratings yet

- Module 3Document15 pagesModule 3Glaiza OrtigueroNo ratings yet

- Macaila Aud SummaryDocument24 pagesMacaila Aud Summarypopla poplaNo ratings yet

- 2RAC - Revision 2019 Lecture 11Document7 pages2RAC - Revision 2019 Lecture 11Jia YinNo ratings yet

- Audit ReviewDocument12 pagesAudit ReviewAmanda ClaroNo ratings yet

- Topic 5Document20 pagesTopic 5shinallata863No ratings yet

- Chapter 9 - Audit Rick HayesDocument21 pagesChapter 9 - Audit Rick HayessesiliaNo ratings yet

- LS 3.00 - PSA 330 Auditor's Response To Assessed RiskDocument5 pagesLS 3.00 - PSA 330 Auditor's Response To Assessed RiskSkye LeeNo ratings yet

- Weeks 5 Topic 5Document13 pagesWeeks 5 Topic 5Shalin LataNo ratings yet

- Auditing TechniquesDocument31 pagesAuditing TechniquesmigraneNo ratings yet

- Lesson G - 2 Ch09 2 Rev. Cycle Obj., Control, TestDocument34 pagesLesson G - 2 Ch09 2 Rev. Cycle Obj., Control, TestBlacky PinkyNo ratings yet

- 1) Lec 1 - The Auditing Assurance EnvironmentDocument15 pages1) Lec 1 - The Auditing Assurance Environmentcats singhNo ratings yet

- Auditing The Expenditure Cycle: Chapter 15 (Tutor Financial Audit)Document15 pagesAuditing The Expenditure Cycle: Chapter 15 (Tutor Financial Audit)Himawan TanNo ratings yet

- AuditofLiabilities PDFDocument6 pagesAuditofLiabilities PDFEricka Mher IsletaNo ratings yet

- LECTURE 2 Applied AuditingDocument9 pagesLECTURE 2 Applied AuditingJoanna GarciaNo ratings yet

- Arens Auditing16e SM 13Document21 pagesArens Auditing16e SM 13김현중No ratings yet

- Internal Control and EvidenceDocument12 pagesInternal Control and EvidenceSanaNo ratings yet

- Key Audit Topics - Final Comp ExamDocument3 pagesKey Audit Topics - Final Comp Examnevilalopariyahoo.comNo ratings yet

- Aud C11Document46 pagesAud C11FATIN 'AISYAH MASLAN ABDUL HAFIZNo ratings yet

- Fundamentals Level - Skills Module, F8 (INT) Audit and AssuranceDocument12 pagesFundamentals Level - Skills Module, F8 (INT) Audit and AssurancekhengmaiNo ratings yet

- The Purpose of Audit TestsDocument2 pagesThe Purpose of Audit TestsOsemwegie PaulNo ratings yet

- Auditing Technique: Kinds of Audit TechniquesDocument7 pagesAuditing Technique: Kinds of Audit TechniquesQasim DodhyNo ratings yet

- Ac6 Narrative Inherent Risk and Control EnvironmentDocument7 pagesAc6 Narrative Inherent Risk and Control EnvironmentAndrew PanganibanNo ratings yet

- ARIBA, Fretzyl Bless A. - Chapter 9 - Substantive Test of Receivables and Sales - ReflectionDocument3 pagesARIBA, Fretzyl Bless A. - Chapter 9 - Substantive Test of Receivables and Sales - ReflectionFretzyl JulyNo ratings yet

- AC414 - Audit and Investigations II - Introduction To Audit EvidenceDocument32 pagesAC414 - Audit and Investigations II - Introduction To Audit EvidenceTsitsi AbigailNo ratings yet

- 7 Major Phases On AuditDocument4 pages7 Major Phases On AuditvinceNo ratings yet

- Overall Audit Strategy and Audit Program: Concept Checks P. 385Document23 pagesOverall Audit Strategy and Audit Program: Concept Checks P. 385Eileen HUANGNo ratings yet

- Tutorial Solution 11042019Document6 pagesTutorial Solution 11042019Shilongo OliviaNo ratings yet

- Overview of Audit Process and Preliminary ActivitiesDocument40 pagesOverview of Audit Process and Preliminary Activitiesgelly studiesNo ratings yet

- .Overview of Audit Process and Preliminary ActivitiesDocument39 pages.Overview of Audit Process and Preliminary Activitiespamelajanmea2018No ratings yet

- Aulab Case 7Document7 pagesAulab Case 7sulthanhakimNo ratings yet

- Kunci Jawaban Arens Chapter 13Document27 pagesKunci Jawaban Arens Chapter 13Abdul Malik FajriNo ratings yet

- PSA NotesDocument15 pagesPSA NotesHanis MaisarahNo ratings yet

- NteDocument8 pagesNtevishnuvermaNo ratings yet

- Final Exam Revision 2 - B8af108 - SolutionDocument6 pagesFinal Exam Revision 2 - B8af108 - SolutionEizam Ben JetteyNo ratings yet

- 4.1 Audit Evidence NewDocument24 pages4.1 Audit Evidence NewSaiful IslamNo ratings yet

- SIM ACP 323 Week 4 5Document32 pagesSIM ACP 323 Week 4 5Helga MatiasNo ratings yet

- Topic 18 Tests of Control V Substantive TestsDocument6 pagesTopic 18 Tests of Control V Substantive TestsRoushie Nae Elarco BartolataNo ratings yet

- Annual Update and Practice Issues for Preparation, Compilation, and Review EngagementsFrom EverandAnnual Update and Practice Issues for Preparation, Compilation, and Review EngagementsNo ratings yet

- CPA Review Notes 2019 - Audit (AUD)From EverandCPA Review Notes 2019 - Audit (AUD)Rating: 3.5 out of 5 stars3.5/5 (10)

- Audi 01J Multitronic CVTDocument99 pagesAudi 01J Multitronic CVTenes_br95% (21)

- Technical Information: Spare Eebds Mentioned in Item 1 Are Not To Be Included in Total NumberDocument5 pagesTechnical Information: Spare Eebds Mentioned in Item 1 Are Not To Be Included in Total NumberSatbir SinghNo ratings yet

- Chapter 34 The Endocrine SystemDocument39 pagesChapter 34 The Endocrine Systemtheia28No ratings yet

- Dear John Book AnalysisDocument2 pagesDear John Book AnalysisQuincy Mae MontereyNo ratings yet

- List of Telugu Films of 2005 - WikipediaDocument1 pageList of Telugu Films of 2005 - WikipediaRa RsNo ratings yet

- ZONE A - Walled City ReportDocument49 pagesZONE A - Walled City ReportAr Vishnu Prakash0% (1)

- Reflection PaperDocument2 pagesReflection PapershanoiapowelllNo ratings yet

- Material 1 (Writing Good Upwork Proposals)Document3 pagesMaterial 1 (Writing Good Upwork Proposals)OvercomerNo ratings yet

- Animal Farm: Social and Historical ContextDocument4 pagesAnimal Farm: Social and Historical ContextfancyNo ratings yet

- Design and Construction of A GSM Based Gas Leak Alert SystemDocument6 pagesDesign and Construction of A GSM Based Gas Leak Alert SystemGibin GeorgeNo ratings yet

- Unit Test: Año de La Diversificación Productiva y Del Fortalecimiento de La EducaciónDocument5 pagesUnit Test: Año de La Diversificación Productiva y Del Fortalecimiento de La EducaciónClaudia Ortiz VicenteNo ratings yet

- Gremlins 3Document12 pagesGremlins 3Kenny TadrzynskiNo ratings yet

- Haramaya University: R.NO Fname Lname IDDocument13 pagesHaramaya University: R.NO Fname Lname IDRamin HamzaNo ratings yet

- LoL Champions & Summoners Stats & Rankings - LeagueOfGraphsDocument5 pagesLoL Champions & Summoners Stats & Rankings - LeagueOfGraphsnadim pachecoNo ratings yet

- Emñìr (Ûvr'Df© - 2018: A (ZDM'© (DF'MDocument54 pagesEmñìr (Ûvr'Df© - 2018: A (ZDM'© (DF'MKarmicSmokeNo ratings yet

- Test 4 A: Vocabulary Circle The Correct AnswerDocument2 pagesTest 4 A: Vocabulary Circle The Correct AnswerMarija JakovNo ratings yet

- AN APPRAISAL OF POPE LEO XIIIS AETERNI PatrisDocument59 pagesAN APPRAISAL OF POPE LEO XIIIS AETERNI PatrisCharles MorrisonNo ratings yet

- August 2012 NewsletterDocument27 pagesAugust 2012 NewsletterBiewBiewNo ratings yet

- Crim 2 ReviewerDocument193 pagesCrim 2 ReviewerMaria Diory Rabajante100% (3)

- A Detailed Lesson PlanDocument8 pagesA Detailed Lesson PlanCris LoretoNo ratings yet

- BPM Award Submission Adidas Bizagi 2013Document15 pagesBPM Award Submission Adidas Bizagi 2013AlirezaNNo ratings yet

- Flushing of An Indwelling Catheter and Bladder Washouts KnowbotsDocument5 pagesFlushing of An Indwelling Catheter and Bladder Washouts KnowbotsTanaman PeternakanNo ratings yet

- Ta35 Ta40 Operations SafetyDocument150 pagesTa35 Ta40 Operations Safetyjuan100% (2)

- Individual Defending SessionDocument6 pagesIndividual Defending SessionAnonymous FN27MzNo ratings yet

- Physical Hazards 101Document24 pagesPhysical Hazards 101Mohamed AhmedNo ratings yet

- Enzyme-Linked Immunosorbent Assay (ELISA)Document3 pagesEnzyme-Linked Immunosorbent Assay (ELISA)Wael OsmanNo ratings yet

- Inesco Amc 2106735164Document3 pagesInesco Amc 2106735164spahujNo ratings yet

- What Is IELTS?Document6 pagesWhat Is IELTS?ANGLISHTNo ratings yet

- Luxury Customer ProfilingDocument16 pagesLuxury Customer ProfilingIndrani Pan100% (1)

- Thi Giua Ki 2Document2 pagesThi Giua Ki 2Trang nguyenNo ratings yet