You might also like

- 6 Sources of Retirement Income: How To Create Your Retirement PaycheckDocument27 pages6 Sources of Retirement Income: How To Create Your Retirement PaycheckGerman Briceño0% (1)

- 0403 Glossary of Life Insurance TermsDocument6 pages0403 Glossary of Life Insurance TermsttongNo ratings yet

- Overview of Premium Financed Life InsuranceDocument17 pagesOverview of Premium Financed Life InsuranceProvada Insurance Services100% (1)

- Wage, Salary and Reward AdministrationDocument34 pagesWage, Salary and Reward AdministrationSuparna2No ratings yet

- Dec Salary SlipDocument1 pageDec Salary SlipShubhamNo ratings yet

- Understanding Actuarial Practice - KlugmanDocument54 pagesUnderstanding Actuarial Practice - Klugmanjoe malor0% (1)

- Foundations of Financial Markets and Institutions 4th Edition Fabozzi Solutions ManualDocument8 pagesFoundations of Financial Markets and Institutions 4th Edition Fabozzi Solutions Manualfinificcodille6d3h100% (23)

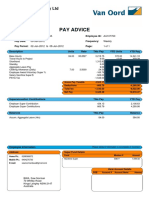

- 0451 Pay Advice AU107760 WK 201228 PDFDocument1 page0451 Pay Advice AU107760 WK 201228 PDFNorman BwaNo ratings yet

- Blackrock Essentials Guide To LdiDocument52 pagesBlackrock Essentials Guide To LdiL Prakash JenaNo ratings yet

- Payslip April 2021 State Bank of India: AIOPP6062HDocument1 pagePayslip April 2021 State Bank of India: AIOPP6062HsayanNo ratings yet

- Premium Paid Certificate For The Year 2022-2023Document1 pagePremium Paid Certificate For The Year 2022-2023yogesh bafnaNo ratings yet

- Project Report Sem IV - Tax Planning in IndiaDocument62 pagesProject Report Sem IV - Tax Planning in IndiaRahul SinghNo ratings yet

- (Use The Below Problem To Answers The Succeeding Four (4) Questions.)Document3 pages(Use The Below Problem To Answers The Succeeding Four (4) Questions.)admiral spongebobNo ratings yet

- Mercado R Mlprime 28072023152829Document19 pagesMercado R Mlprime 28072023152829Jem AmansecNo ratings yet

- Sun Smarter Life ClassicDocument7 pagesSun Smarter Life Classicpaul jan sarachoNo ratings yet

- B Pension Risk TransferDocument7 pagesB Pension Risk TransferMikhail FrancisNo ratings yet

- Aquino AP Ml100 With-Complete-RidersDocument16 pagesAquino AP Ml100 With-Complete-RidersAldrin Paul AquinoNo ratings yet

- EO-Short Qns & Ans onEPF ActDocument13 pagesEO-Short Qns & Ans onEPF ActRatnesh RajanyaNo ratings yet

- Insurance Commission Traditional Life ReviewerDocument42 pagesInsurance Commission Traditional Life Reviewerkristine de jesus100% (2)

- National Pension System (Blackbook)Document86 pagesNational Pension System (Blackbook)chirag karara100% (2)

- Asset Management-Pension FundsDocument9 pagesAsset Management-Pension FundsKen BiiNo ratings yet

- Chapter 15 - Pensions and Other Postretirement BenefitsDocument35 pagesChapter 15 - Pensions and Other Postretirement Benefitselizabeth karinaNo ratings yet

- Accounting For Pensions and Postretirement BenefitsDocument3 pagesAccounting For Pensions and Postretirement BenefitsDhivena JeonNo ratings yet

- Pension Topic One and TwoDocument7 pagesPension Topic One and Twonogarap767No ratings yet

- Chapter 14Document23 pagesChapter 14YolandaNo ratings yet

- Pension Terminology FinalDocument8 pagesPension Terminology FinalEugeneNo ratings yet

- LDI Explained - 2017 FinalDocument44 pagesLDI Explained - 2017 Finaladonettos4008No ratings yet

- Actuarial Glossary PDFDocument18 pagesActuarial Glossary PDFmiguelNo ratings yet

- Term Paper of BankingDocument22 pagesTerm Paper of BankingnidhijunejaNo ratings yet

- Project For Pension PlanDocument9 pagesProject For Pension PlanLakshmi DlaksNo ratings yet

- 03 Conventional With ProfitDocument8 pages03 Conventional With ProfitKimondo KingNo ratings yet

- Cash Balance PlansDocument11 pagesCash Balance Plansmphillips36111No ratings yet

- RISK Chapter 5Document19 pagesRISK Chapter 5Taresa AdugnaNo ratings yet

- Liability-Driven Investing For Defined Benefit Pensions PlansDocument25 pagesLiability-Driven Investing For Defined Benefit Pensions PlansasdasdNo ratings yet

- Organisation For Economic Co-Operation and Development: Hosted by The Government of BrazilDocument11 pagesOrganisation For Economic Co-Operation and Development: Hosted by The Government of Brazildata4csasNo ratings yet

- Effect of Pension Funds Characteristics On Financial Performance of Pension Administrators Chapter OneDocument39 pagesEffect of Pension Funds Characteristics On Financial Performance of Pension Administrators Chapter OneUmar FarouqNo ratings yet

- Chapter 20Document21 pagesChapter 20Diana SantosNo ratings yet

- Chapter 2 Lecture Notes.2021Document15 pagesChapter 2 Lecture Notes.2021Hoyin SinNo ratings yet

- Max New York Life, Axis Bank Sign Bancassurance RelationshipDocument22 pagesMax New York Life, Axis Bank Sign Bancassurance RelationshipAnurag PateriaNo ratings yet

- IAS Group1Document7 pagesIAS Group1Carol PhaswanaNo ratings yet

- Tier-I Account: Fund ManagersDocument5 pagesTier-I Account: Fund ManagersKarthikeyanNo ratings yet

- Life InsuranceDocument22 pagesLife Insuranceckchetankhatri967No ratings yet

- Pension Plans in India NEWWDocument22 pagesPension Plans in India NEWWKomal BhatiaNo ratings yet

- FP Group WorkDocument12 pagesFP Group WorkStellina JoeshibaNo ratings yet

- 1st Case CORTEZ - ML - MLPRIME - 21052022173703Document16 pages1st Case CORTEZ - ML - MLPRIME - 21052022173703Jeanina delos ReyesNo ratings yet

- A New Defined Benefit Pension Risk Measurement Methodology2015Insurance Mathematics and EconomicsDocument12 pagesA New Defined Benefit Pension Risk Measurement Methodology2015Insurance Mathematics and EconomicsMartínCamarenaNo ratings yet

- Defined Benefit Pension PlanDocument8 pagesDefined Benefit Pension Planhenok AbebeNo ratings yet

- Categories of InsuranceDocument6 pagesCategories of InsurancewilliamyesNo ratings yet

- Jagendra Kumar RenewedDocument7 pagesJagendra Kumar RenewedbcibaneNo ratings yet

- Performance Measurement For Pension Funds: Auke Plantinga March 2005Document15 pagesPerformance Measurement For Pension Funds: Auke Plantinga March 2005Dasulea V.No ratings yet

- Institute OF Commerce, Nirma University (Honors) Programme (2017-2020)Document15 pagesInstitute OF Commerce, Nirma University (Honors) Programme (2017-2020)Paras MasariaNo ratings yet

- All You Wanted To Know About Pension Plans!: Share ThisDocument10 pagesAll You Wanted To Know About Pension Plans!: Share ThisAbhi SharmaNo ratings yet

- Briones N Mlprime 18072023193014Document19 pagesBriones N Mlprime 18072023193014Jem AmansecNo ratings yet

- Wealthsurance Growth Insurance Plan SP - Brochure - 1 PDFDocument23 pagesWealthsurance Growth Insurance Plan SP - Brochure - 1 PDFKARAN SINGH-MBA0% (1)

- E.Types of Retirement Plans-1Document13 pagesE.Types of Retirement Plans-1Madhu dollyNo ratings yet

- Johnson & JohnsonDocument2 pagesJohnson & JohnsonpthavNo ratings yet

- Updated Pensions Training - Slides 05.03.18Document101 pagesUpdated Pensions Training - Slides 05.03.18archanaanuNo ratings yet

- BOLI Overview - Meyer ChatfieldDocument4 pagesBOLI Overview - Meyer ChatfieldjrboulwareNo ratings yet

- Bethlehem Case WriteupDocument3 pagesBethlehem Case WriteupAdityaMakhija100% (2)

- Group Insurance ProductsDocument8 pagesGroup Insurance Productshamza omarNo ratings yet

- File 4Document4 pagesFile 4Sk AslamNo ratings yet

- Chapter-25 - Pension Fund OperationsDocument17 pagesChapter-25 - Pension Fund OperationsZareen TasfiahNo ratings yet

- Semana JK Mlprime 30082023134907Document16 pagesSemana JK Mlprime 30082023134907Rogelio EscobarNo ratings yet

- EFU Retirement PlanDocument14 pagesEFU Retirement PlanGhafoor khanNo ratings yet

- POI MaterialDocument11 pagesPOI MaterialMukesh ChoudharyNo ratings yet

- Ac Standard - AS15Document9 pagesAc Standard - AS15api-3705877No ratings yet

- Heading DescriptionDocument4 pagesHeading DescriptionSri Ram SahooNo ratings yet

- Joint Trade Union Response From The Staff Side of The Pensions Working GroupDocument7 pagesJoint Trade Union Response From The Staff Side of The Pensions Working GroupRMT London CallingNo ratings yet

- The Economic Impact of Protracted Low Interest RatDocument21 pagesThe Economic Impact of Protracted Low Interest RatAna López RoucoNo ratings yet

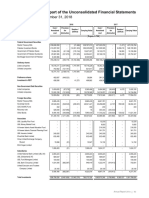

- UBL Annual Report 2018-182Document1 pageUBL Annual Report 2018-182IFRS LabNo ratings yet

- UBL Annual Report 2018-180Document1 pageUBL Annual Report 2018-180IFRS LabNo ratings yet

- UBL Annual Report 2018-179Document1 pageUBL Annual Report 2018-179IFRS LabNo ratings yet

- UBL Annual Report 2018-172Document1 pageUBL Annual Report 2018-172IFRS LabNo ratings yet

- UBL Annual Report 2018-159Document1 pageUBL Annual Report 2018-159IFRS LabNo ratings yet

- UBL Annual Report 2018-160Document1 pageUBL Annual Report 2018-160IFRS LabNo ratings yet

- UBL Annual Report 2018-126Document1 pageUBL Annual Report 2018-126IFRS LabNo ratings yet

- UBL Annual Report 2018-166Document1 pageUBL Annual Report 2018-166IFRS LabNo ratings yet

- UBL Annual Report 2018-157Document1 pageUBL Annual Report 2018-157IFRS LabNo ratings yet

- UBL Annual Report 2018-145Document1 pageUBL Annual Report 2018-145IFRS LabNo ratings yet

- UBL Annual Report 2018-165Document1 pageUBL Annual Report 2018-165IFRS LabNo ratings yet

- UBL Annual Report 2018-131Document1 pageUBL Annual Report 2018-131IFRS LabNo ratings yet

- UBL Annual Report 2018-125Document1 pageUBL Annual Report 2018-125IFRS LabNo ratings yet

- UBL Annual Report 2018-132Document1 pageUBL Annual Report 2018-132IFRS LabNo ratings yet

- UBL Annual Report 2018-109Document1 pageUBL Annual Report 2018-109IFRS LabNo ratings yet

- UBL Annual Report 2018-98Document1 pageUBL Annual Report 2018-98IFRS LabNo ratings yet

- UBL Annual Report 2018-118Document1 pageUBL Annual Report 2018-118IFRS LabNo ratings yet

- UBL Annual Report 2018-120Document1 pageUBL Annual Report 2018-120IFRS LabNo ratings yet

- UBL Annual Report 2018-137Document1 pageUBL Annual Report 2018-137IFRS LabNo ratings yet

- UBL Annual Report 2018-130Document1 pageUBL Annual Report 2018-130IFRS LabNo ratings yet

- UBL Annual Report 2018-97Document1 pageUBL Annual Report 2018-97IFRS LabNo ratings yet

- UBL Annual Report 2018-110Document1 pageUBL Annual Report 2018-110IFRS LabNo ratings yet

- UBL Annual Report 2018-103Document1 pageUBL Annual Report 2018-103IFRS LabNo ratings yet

- UBL Annual Report 2018-92Document1 pageUBL Annual Report 2018-92IFRS LabNo ratings yet

- UBL Annual Report 2018-95Document1 pageUBL Annual Report 2018-95IFRS LabNo ratings yet

- UBL Annual Report 2018-107Document1 pageUBL Annual Report 2018-107IFRS LabNo ratings yet

- UBL Annual Report 2018-106Document1 pageUBL Annual Report 2018-106IFRS LabNo ratings yet

- UBL Annual Report 2018-88Document1 pageUBL Annual Report 2018-88IFRS LabNo ratings yet

- UBL Annual Report 2018-90Document1 pageUBL Annual Report 2018-90IFRS LabNo ratings yet

- UBL Annual Report 2018-93Document1 pageUBL Annual Report 2018-93IFRS LabNo ratings yet

- QuestionnaireDocument3 pagesQuestionnaireMr. Khan100% (1)

- Unit 5Document2 pagesUnit 5HuysymNo ratings yet

- 1223.9 F Benefit Payment Application ISS6 - 1021 - HRDocument4 pages1223.9 F Benefit Payment Application ISS6 - 1021 - HRCam Kemshal-BellNo ratings yet

- Occupation GuidelinesDocument160 pagesOccupation Guidelinesjo lamosNo ratings yet

- ISR3702 Assignment 2 Second SemesterDocument2 pagesISR3702 Assignment 2 Second SemesteridreesNo ratings yet

- SAPayslipDocument1 pageSAPayslipmomen rababahNo ratings yet

- International Pay Systems (Chap 8)Document35 pagesInternational Pay Systems (Chap 8)Incia HaiderNo ratings yet

- Central Govt Scheme HandbookDocument51 pagesCentral Govt Scheme HandbookaatishsutardasNo ratings yet

- Pension Calculation Sheet Sindh 2019 20 21Document6 pagesPension Calculation Sheet Sindh 2019 20 21Inder KishanNo ratings yet

- 14 - PFM - Chapter 13 - Retirement and Estate PlanningDocument2 pages14 - PFM - Chapter 13 - Retirement and Estate PlanningLee K.No ratings yet

- IT-Checklist - Gratuity TrustDocument6 pagesIT-Checklist - Gratuity TrustD S VivekNo ratings yet

- Mint 18.10.2023?Document18 pagesMint 18.10.2023?manikantanjeNo ratings yet

- QC 16159Document18 pagesQC 16159Reza KühnNo ratings yet

- Armed Forces Pension Scheme 1975 Your Pension Scheme ExplainedDocument32 pagesArmed Forces Pension Scheme 1975 Your Pension Scheme ExplainedbobNo ratings yet

- Problems On Income From Salaries: Tax SupplementDocument20 pagesProblems On Income From Salaries: Tax SupplementJkNo ratings yet

- 2020 Annual ReportDocument128 pages2020 Annual ReportSaul PimientaNo ratings yet

- The Barefoot InvestorDocument8 pagesThe Barefoot Investortagoeedmund62No ratings yet

- PNHIS Enrollment Annx IVDocument2 pagesPNHIS Enrollment Annx IVRaghuNo ratings yet

- LIC Form - Intimation of Death Retirement Leaving ServiceDocument1 pageLIC Form - Intimation of Death Retirement Leaving ServicekaustubhNo ratings yet

- Project Investment in Tax Saving Product - An OverviewDocument12 pagesProject Investment in Tax Saving Product - An OverviewAkshay DakhaleNo ratings yet