You might also like

- MATH4512 2022spring HW1SolutionDocument11 pagesMATH4512 2022spring HW1SolutionMNo ratings yet

- Bootstrapping Spot RateDocument37 pagesBootstrapping Spot Ratevirgoss8100% (1)

- Financial Risk Management: A Simple IntroductionFrom EverandFinancial Risk Management: A Simple IntroductionRating: 4.5 out of 5 stars4.5/5 (7)

- f01c 0808781Document72 pagesf01c 0808781Dylan SavageNo ratings yet

- Angel Abundance Oracle CardsDocument35 pagesAngel Abundance Oracle CardsThành Lê100% (3)

- Case Study On Financial Risk AnalysisDocument6 pagesCase Study On Financial Risk AnalysisolafedNo ratings yet

- FINA2322 Tutorial 7 NotesDocument6 pagesFINA2322 Tutorial 7 Notes华邦盛No ratings yet

- Test Your Knowledge: 2.2.4.2 Pricing of SwaptionsDocument11 pagesTest Your Knowledge: 2.2.4.2 Pricing of SwaptionsRITZ BROWNNo ratings yet

- FINA5520 WK3 IntRatesAndIntRateFuturesDocument46 pagesFINA5520 WK3 IntRatesAndIntRateFuturesthelittlebirdyNo ratings yet

- Basics of Bond Valuation: Government Securities (G-SEC, or GS) / Treasury BondsDocument39 pagesBasics of Bond Valuation: Government Securities (G-SEC, or GS) / Treasury BondsVrinda GargNo ratings yet

- Interest Rate FutureDocument25 pagesInterest Rate FutureRitika KhareNo ratings yet

- 2.3 Fra and Swap ExercisesDocument5 pages2.3 Fra and Swap ExercisesrandomcuriNo ratings yet

- Chapter 4 - Interest RatesDocument16 pagesChapter 4 - Interest Ratesuyenbp.a2.1720No ratings yet

- Commercial Bank Management Midsem NotesDocument12 pagesCommercial Bank Management Midsem NotesWinston WongNo ratings yet

- Problem Solving questions-IFTDocument18 pagesProblem Solving questions-IFTPiyush KothariNo ratings yet

- Session 6 - FDDocument26 pagesSession 6 - FDDaksh KhullarNo ratings yet

- EFB344 Lecture07, FRAs and SwapsDocument35 pagesEFB344 Lecture07, FRAs and SwapsTibet LoveNo ratings yet

- How To Value Bonds?: Application of Time Value of MoneyDocument36 pagesHow To Value Bonds?: Application of Time Value of Moneyabhishek dharNo ratings yet

- CH 7 Interest Rate Forwards and FuturesDocument15 pagesCH 7 Interest Rate Forwards and Futuressarthak1.khannaNo ratings yet

- Chapter 5: Interest Rate Risks: Lecturer: Amadeus GABRIEL La Rochelle Business SchoolDocument25 pagesChapter 5: Interest Rate Risks: Lecturer: Amadeus GABRIEL La Rochelle Business SchoolJuana BoresNo ratings yet

- Lecture04 Derivatives StudentDocument22 pagesLecture04 Derivatives StudentMit DaveNo ratings yet

- Econ 406 Final Exam Main 2017Document5 pagesEcon 406 Final Exam Main 2017Shihab HasanNo ratings yet

- FIN4110: Options and Futures: Zongbo Huang Cuhk (SZ)Document27 pagesFIN4110: Options and Futures: Zongbo Huang Cuhk (SZ)liuNo ratings yet

- MFIN6003 AssignmentsDocument4 pagesMFIN6003 AssignmentscccNo ratings yet

- CH 4Document43 pagesCH 4Mick MalickNo ratings yet

- Investment Basics I: ObjectivesDocument14 pagesInvestment Basics I: Objectivesno nameNo ratings yet

- Week 2 SlidesDocument22 pagesWeek 2 SlidesManish ChalanaNo ratings yet

- Fis 5 - 11012021Document5 pagesFis 5 - 11012021JapleenNo ratings yet

- Lecture 02Document31 pagesLecture 02jamshed20No ratings yet

- Chap010 StuDocument24 pagesChap010 StuBingbong Magluyan MonfielNo ratings yet

- Lecture 5312312Document55 pagesLecture 5312312Tam Chun LamNo ratings yet

- 14 Fixed Income Portfolio ManagementDocument60 pages14 Fixed Income Portfolio ManagementPawan ChoudharyNo ratings yet

- Midterm Exam - Answer Key: Professor Salyer, Economics 135, Spring 2009Document2 pagesMidterm Exam - Answer Key: Professor Salyer, Economics 135, Spring 2009kasimNo ratings yet

- Day 4Document39 pagesDay 4Bikash GajurelNo ratings yet

- Fixed Income Assignment 2Document4 pagesFixed Income Assignment 2Rattan Preet SinghNo ratings yet

- International Financial Management PgapteDocument30 pagesInternational Financial Management Pgapterameshmba100% (1)

- Ciia Final Exam 2 March 2009 - SolutionsDocument13 pagesCiia Final Exam 2 March 2009 - SolutionsDavid OparindeNo ratings yet

- Chap 18Document110 pagesChap 18Desai SarvidaNo ratings yet

- CH 18Document131 pagesCH 18Desai SarvidaNo ratings yet

- 70-398 International Finance SPRING 2023: Prof. Serkan AkgucDocument36 pages70-398 International Finance SPRING 2023: Prof. Serkan AkgucAmiko GogitidzeNo ratings yet

- 441 Final Quiz 2021Document6 pages441 Final Quiz 2021yifeihufionaNo ratings yet

- Fixed Income Chapter4Document51 pagesFixed Income Chapter4Sourabh pathakNo ratings yet

- WN 1: Computation of FRA RateDocument5 pagesWN 1: Computation of FRA RateBharat GudlaNo ratings yet

- Chap005a - The Value of BondDocument35 pagesChap005a - The Value of Bondnt.phuongnhu1912No ratings yet

- Level 2 2016 SS 16 (Derivatives)Document51 pagesLevel 2 2016 SS 16 (Derivatives)Anonymous K5ZLwxNo ratings yet

- IM6. Fixed IncomeDocument42 pagesIM6. Fixed IncomeZoon KiatNo ratings yet

- Chapter 5Document25 pagesChapter 5aman7300No ratings yet

- EX 1718 SolDocument10 pagesEX 1718 SolJoana SilvaNo ratings yet

- Immunization StrategiesDocument75 pagesImmunization StrategiesSarang GuptaNo ratings yet

- Bonds DurationDocument31 pagesBonds DurationAashima GroverNo ratings yet

- Security Valuation: DCF Approach To Stock and Bond ValuationDocument44 pagesSecurity Valuation: DCF Approach To Stock and Bond ValuationarchonVNo ratings yet

- Exam Fin 2011Document16 pagesExam Fin 2011alexajungNo ratings yet

- BBA VI Sem. - International Finance - Practical ProblemsDocument16 pagesBBA VI Sem. - International Finance - Practical ProblemsdeepeshmahajanNo ratings yet

- Global Edition: Interest-Rate Swaps, Caps, and FloorsDocument32 pagesGlobal Edition: Interest-Rate Swaps, Caps, and FloorskerenkangNo ratings yet

- MGMT 41150 Midterm Practice Questions - Partial KeyDocument5 pagesMGMT 41150 Midterm Practice Questions - Partial KeyLaxus DreyerNo ratings yet

- Fi8000 Bonds, Interest RatesDocument34 pagesFi8000 Bonds, Interest Ratesradhika1992No ratings yet

- FINA2322 Tutorial 2 SolutionDocument5 pagesFINA2322 Tutorial 2 Solution华邦盛No ratings yet

- HW 2 ADocument6 pagesHW 2 AhatemNo ratings yet

- Week 6 Solutions To ExercisesDocument6 pagesWeek 6 Solutions To ExercisesBerend van RoozendaalNo ratings yet

- FINS3630: UNSW Business SchoolDocument27 pagesFINS3630: UNSW Business SchoolcarolinetsangNo ratings yet

- SOLUTION1. Exercise 1 PDFDocument10 pagesSOLUTION1. Exercise 1 PDFVanessa ThuyNo ratings yet

- You Are Subject To Interest Rate Risk and Wish To HedgeDocument14 pagesYou Are Subject To Interest Rate Risk and Wish To Hedgeexfireex1No ratings yet

- Interest Rate FuturesDocument30 pagesInterest Rate Futuresnischal mathurNo ratings yet

- FINA2322 Tutorial 10 Notes 2023Document8 pagesFINA2322 Tutorial 10 Notes 2023华邦盛No ratings yet

- FINA2322 Tutorial 4 NotesDocument3 pagesFINA2322 Tutorial 4 Notes华邦盛No ratings yet

- Banking Careers Guide 2023Document117 pagesBanking Careers Guide 2023华邦盛No ratings yet

- CH - 4 Introduction To Risk ManagementDocument34 pagesCH - 4 Introduction To Risk Management华邦盛No ratings yet

- FINA2322 Tutorial 5 NotesDocument8 pagesFINA2322 Tutorial 5 Notes华邦盛No ratings yet

- Ch9 ACCT1101 DE S1 2223 MOODLEDocument67 pagesCh9 ACCT1101 DE S1 2223 MOODLE华邦盛No ratings yet

- CH 1Document32 pagesCH 1华邦盛No ratings yet

- FINA2322 Tutorial 2 SolutionDocument5 pagesFINA2322 Tutorial 2 Solution华邦盛No ratings yet

- CH 3 Insurance, Collars, and Other StrategiesDocument44 pagesCH 3 Insurance, Collars, and Other Strategies华邦盛No ratings yet

- Ch3 ACCT1101DE S1 2223 MOODLEDocument71 pagesCh3 ACCT1101DE S1 2223 MOODLE华邦盛No ratings yet

- 13 Single Entry and Incomplete Records - Additional ExercisesDocument5 pages13 Single Entry and Incomplete Records - Additional ExercisesMei Mei Chan100% (2)

- CFPB Consumer Sample Student Loan Payment LetterDocument3 pagesCFPB Consumer Sample Student Loan Payment LetterJiro B.100% (1)

- DR Complete Guide To Money PDFDocument366 pagesDR Complete Guide To Money PDFRobert LindseyNo ratings yet

- Outline in Credit TransactionsDocument11 pagesOutline in Credit TransactionsChristine Gel MadrilejoNo ratings yet

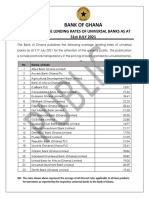

- Average Lending Rates As at July 2021Document1 pageAverage Lending Rates As at July 2021Fuaad DodooNo ratings yet

- A Framework For The Analysis of Financial FlexibilityDocument9 pagesA Framework For The Analysis of Financial FlexibilityEdwin GunawanNo ratings yet

- What Is FortfaitingDocument3 pagesWhat Is FortfaitingRAMESHBABUNo ratings yet

- Complaint For Foreclosure of Real Estate MortgageDocument2 pagesComplaint For Foreclosure of Real Estate MortgageTere Tongson100% (1)

- Tripartite Agreement - New Draft - 2020Document9 pagesTripartite Agreement - New Draft - 2020KAMESH MOOLANo ratings yet

- FIN 3331 Managerial Finance: Time Value of MoneyDocument23 pagesFIN 3331 Managerial Finance: Time Value of MoneyHa NguyenNo ratings yet

- Banking Operations by Pooja KadamDocument12 pagesBanking Operations by Pooja KadamSomnath KhandagaleNo ratings yet

- Analysis of Financial StatementsDocument53 pagesAnalysis of Financial StatementsProject MgtNo ratings yet

- 500 - Household Assets and Liabilities in IndiaDocument498 pages500 - Household Assets and Liabilities in IndiaRishiNo ratings yet

- Intermediate Acctg Lecture On Liabilities 22Document3 pagesIntermediate Acctg Lecture On Liabilities 22Tracy Lyn Macasieb NavidadNo ratings yet

- Serfino vs. Far East BankDocument8 pagesSerfino vs. Far East BankGracelyn Enriquez BellinganNo ratings yet

- PV Factor 1/1.1 0.909091 .909091/1.1 0.826446 .826446/1.1 0.751315 133,100.00 100,000.00Document5 pagesPV Factor 1/1.1 0.909091 .909091/1.1 0.826446 .826446/1.1 0.751315 133,100.00 100,000.00Allyna Jane EnriquezNo ratings yet

- Placencia's Code On The Ancient Customs of The Tagalogs (1589)Document18 pagesPlacencia's Code On The Ancient Customs of The Tagalogs (1589)CassandraNo ratings yet

- Blai - PrelimDocument7 pagesBlai - PrelimSydney Miles MahinayNo ratings yet

- WEEK SIX Bond Valuation Part-2Document12 pagesWEEK SIX Bond Valuation Part-2kazi A.R RafiNo ratings yet

- Debt Deception: How Debt Buyers Abuse The Legal System To Prey On Lower-Income New Yorkers (2010)Document36 pagesDebt Deception: How Debt Buyers Abuse The Legal System To Prey On Lower-Income New Yorkers (2010)Jillian Sheridan100% (1)

- Del Monte Pacific LimitedDocument7 pagesDel Monte Pacific LimitedPrincess Diane VicenteNo ratings yet

- Capital MarketDocument26 pagesCapital MarkethimanshusangaNo ratings yet

- Test Bank For Economics of Money Banking and Financial Markets Canadian 6th Edition by Mishkin Serletis ISBN 0133897389 9780133897388Document36 pagesTest Bank For Economics of Money Banking and Financial Markets Canadian 6th Edition by Mishkin Serletis ISBN 0133897389 9780133897388james.crouse530100% (14)

- دور-البنوك-في-تمويل-الاستثمارات-مسعود-دراوسيDocument8 pagesدور-البنوك-في-تمويل-الاستثمارات-مسعود-دراوسيseed1876No ratings yet

- Mortgage OfferDocument11 pagesMortgage OfferMark JacksonNo ratings yet

- Conceptual Framework and Accounting Standards Final ExamDocument59 pagesConceptual Framework and Accounting Standards Final ExamCleofe Mae Piñero AseñasNo ratings yet

- Financial Analysis of BioconDocument12 pagesFinancial Analysis of BioconNipun KothariNo ratings yet