You might also like

- Unincorporated Business TrustDocument9 pagesUnincorporated Business TrustSpencerRyanOneal98% (43)

- Independent Contractor Draft AgreementDocument10 pagesIndependent Contractor Draft AgreementEtienne BellemareNo ratings yet

- Risk Management in The Insurance Industry and Solvency IIDocument40 pagesRisk Management in The Insurance Industry and Solvency IIkhush360% (1)

- Cancellation Form Refund RequestDocument2 pagesCancellation Form Refund RequestVinh Duong0% (1)

- Notes Week 10 Ucsp Nonstate InstitutionsDocument2 pagesNotes Week 10 Ucsp Nonstate InstitutionsJosephine Coevas100% (4)

- Ap 3Document397 pagesAp 3Ayush SharmaNo ratings yet

- 120 Multiple Choice Questions: Answer: AIIBDocument29 pages120 Multiple Choice Questions: Answer: AIIBनरोत्तमवत्सNo ratings yet

- Advanced Financial Accounting and Reporting III Final Exam Answer KeyDocument16 pagesAdvanced Financial Accounting and Reporting III Final Exam Answer KeyCarlito B. Bancil100% (1)

- Frauds in Insurance SectorDocument55 pagesFrauds in Insurance Sectormansi berde100% (3)

- LIC Project ReportDocument67 pagesLIC Project ReportKusum Pali50% (2)

- Bpvoy3 Format PDFDocument17 pagesBpvoy3 Format PDFAnonymous UCveMQNo ratings yet

- LICDocument82 pagesLICTinu Burmi Anand67% (3)

- Insurance Awareness in India MainDocument39 pagesInsurance Awareness in India Maintejaskamble4575% (4)

- Pre Trial Brief UpgainsDocument4 pagesPre Trial Brief UpgainsSig G. MiNo ratings yet

- Role of LIC in Indian InsuranceDocument61 pagesRole of LIC in Indian Insurancenikita950100% (2)

- Finance - HDFCSLIC - Analysis of Insurance Industry With Respect To HDFCSLICDocument101 pagesFinance - HDFCSLIC - Analysis of Insurance Industry With Respect To HDFCSLICGaurav RathaurNo ratings yet

- Project Topic IRDA and Insurance Administration in IndiaDocument18 pagesProject Topic IRDA and Insurance Administration in IndiaSneha SharmaNo ratings yet

- FA SonalDocument15 pagesFA SonalPrakash BhanushaliNo ratings yet

- Comparative Analysis of Life Insurance Products Report FinalDocument55 pagesComparative Analysis of Life Insurance Products Report Finalprabux55314No ratings yet

- Insurance in India - WikipediaDocument4 pagesInsurance in India - WikipediaRakesh HaldarNo ratings yet

- Comparison Between Pension Plans of Lic and IciciDocument103 pagesComparison Between Pension Plans of Lic and IciciNaMan SeThiNo ratings yet

- The Insurance Industry in India and OverviewDocument15 pagesThe Insurance Industry in India and OverviewVijayKumar NishadNo ratings yet

- A Study On Assessing Insurance Awareness in India: G.SuganyaDocument4 pagesA Study On Assessing Insurance Awareness in India: G.SuganyaShehzadNo ratings yet

- Icici PrudentialDocument52 pagesIcici PrudentialDeepak DevaniNo ratings yet

- Growth of Ins Sec in IndiaDocument11 pagesGrowth of Ins Sec in IndiaVishal Dh MajhiNo ratings yet

- Chapter 1Document14 pagesChapter 1Devi Bala JNo ratings yet

- T Reliance Life InsuranceDocument54 pagesT Reliance Life Insurancenikhil kumarNo ratings yet

- Bbi Ka ProjectDocument60 pagesBbi Ka ProjectViral SanghaviNo ratings yet

- Project Report: Life Insurance Corporation of IndiaDocument57 pagesProject Report: Life Insurance Corporation of IndiaBidhu Bhushan AcharyaNo ratings yet

- Kar MV Eeeeeeeeeee RDocument18 pagesKar MV Eeeeeeeeeee RvirenderjpNo ratings yet

- Project FinalDocument65 pagesProject FinalSafil FaizNo ratings yet

- Current Insurance Market: Project ONDocument26 pagesCurrent Insurance Market: Project ONAnkita DharodNo ratings yet

- Overview of Indian Insurance SectorDocument16 pagesOverview of Indian Insurance SectorViral FanasiaNo ratings yet

- Comparative Analysis of HDFC SLIC With Other Insurance CompanyDocument76 pagesComparative Analysis of HDFC SLIC With Other Insurance Companysshane kumarNo ratings yet

- Insurance in IndiaDocument6 pagesInsurance in IndiaChandresh KumarNo ratings yet

- Insurance Awareness PDF by ExampunditDocument9 pagesInsurance Awareness PDF by ExampunditKathleen StephensonNo ratings yet

- Insurance System in IndiaDocument8 pagesInsurance System in IndiaTej DhillonNo ratings yet

- National InsuranceDocument29 pagesNational InsurancePratik HariyaniNo ratings yet

- Chapter-I: 1.1 Industry Profile & 1.2 Company ProfileDocument55 pagesChapter-I: 1.1 Industry Profile & 1.2 Company ProfileTeja KaikapalliNo ratings yet

- Group 2 Test ADocument16 pagesGroup 2 Test AHarish JanardhananNo ratings yet

- Report On Recruitment of Life Advisors Bharti AXADocument84 pagesReport On Recruitment of Life Advisors Bharti AXAmegha140190No ratings yet

- Research ProjectDocument37 pagesResearch Projectmansi berdeNo ratings yet

- WipDocument38 pagesWipsujata_patil11214405No ratings yet

- RelianceDocument35 pagesRelianceamisha wakadeNo ratings yet

- Yes ICICIDocument55 pagesYes ICICIRahul ChhabraNo ratings yet

- Insurance Sector in IndiaDocument5 pagesInsurance Sector in Indiamukesh_khana962No ratings yet

- Tata Aia Vs LICDocument21 pagesTata Aia Vs LICsahilgrvr100% (1)

- Insurance in IndiaDocument4 pagesInsurance in IndiaHussainAttarwalaNo ratings yet

- Student, Department of Management Studies, Christ UniversityDocument13 pagesStudent, Department of Management Studies, Christ UniversitydharmarajNo ratings yet

- Market Share of Insurannce CompanyDocument29 pagesMarket Share of Insurannce Companysaurabh dixitNo ratings yet

- A Study On Recruitment and Selection Process of Advisors in Insurance CompanyDocument56 pagesA Study On Recruitment and Selection Process of Advisors in Insurance Companykundanky@live.in83% (6)

- Distribution On Insurance SectorDocument23 pagesDistribution On Insurance SectorSIDHARTH TiwariNo ratings yet

- Index: Student Declaration I Certificate From Guide II Acknowledgement III Executive Summary IVDocument37 pagesIndex: Student Declaration I Certificate From Guide II Acknowledgement III Executive Summary IVJaime ButlerNo ratings yet

- Submitted in The Partial For The Award of Degree Of: Bachelor of Business AdministrationDocument45 pagesSubmitted in The Partial For The Award of Degree Of: Bachelor of Business AdministrationDimple SharmaNo ratings yet

- Summer Training Project Report On Recruitment and Training of Life Associate'S in DLF Pramerica Life Insurance CompanyDocument79 pagesSummer Training Project Report On Recruitment and Training of Life Associate'S in DLF Pramerica Life Insurance CompanynagpalanishNo ratings yet

- Financial Performance of Commercial Bank in IndiaDocument85 pagesFinancial Performance of Commercial Bank in IndiamamtaNo ratings yet

- Insurance in India: HistoryDocument6 pagesInsurance in India: HistoryRahul MandalNo ratings yet

- Somendra Kumar MeenaDocument98 pagesSomendra Kumar MeenaSomendra Kumar MeenaNo ratings yet

- My ProjectDocument91 pagesMy ProjectRanjith BandiNo ratings yet

- Business Environment Project Report: Group 4Document13 pagesBusiness Environment Project Report: Group 4SHIVAM CHUGHNo ratings yet

- Role of Intermediaries in Insurance Sector-1Document32 pagesRole of Intermediaries in Insurance Sector-1Prakash Kumar100% (6)

- Icici Life Insurance Recruitment of Advisers For Selling The Financial ProductsDocument103 pagesIcici Life Insurance Recruitment of Advisers For Selling The Financial Productschinu1988No ratings yet

- History of Insurance SectorDocument8 pagesHistory of Insurance SectorNeethu B.sNo ratings yet

- DeclarationDocument72 pagesDeclarationit rewaNo ratings yet

- Financial Analysis of Future Generali Life InsuranceDocument56 pagesFinancial Analysis of Future Generali Life InsurancesuryakantshrotriyaNo ratings yet

- A Study On The Growth of Indian Insurance SectorDocument16 pagesA Study On The Growth of Indian Insurance SectorIAEME Publication100% (1)

- MetlifeDocument73 pagesMetlifeMusharaf MominNo ratings yet

- LAW AND SOCIAL TRANSFORMATION RELATED TO FAMILY LAWS IN INDIADocument7 pagesLAW AND SOCIAL TRANSFORMATION RELATED TO FAMILY LAWS IN INDIAGeerthana ArasuNo ratings yet

- Pamela HerdDocument14 pagesPamela HerdGeerthana ArasuNo ratings yet

- TARA SINHA - Gujarat insuranceDocument11 pagesTARA SINHA - Gujarat insuranceGeerthana ArasuNo ratings yet

- SURROGACY IN INDIADocument16 pagesSURROGACY IN INDIAGeerthana ArasuNo ratings yet

- Branfoot 2008Document25 pagesBranfoot 2008Geerthana ArasuNo ratings yet

- REVISED TRIPs - SLIDESDocument35 pagesREVISED TRIPs - SLIDESGeerthana ArasuNo ratings yet

- Neuro PsychologyDocument9 pagesNeuro PsychologyGeerthana ArasuNo ratings yet

- Volume9 Issue7 (2) 2020Document214 pagesVolume9 Issue7 (2) 2020Geerthana ArasuNo ratings yet

- Research Methods and Applied StatisticsDocument8 pagesResearch Methods and Applied StatisticsGeerthana ArasuNo ratings yet

- Nayakar TempleDocument26 pagesNayakar TempleGeerthana ArasuNo ratings yet

- Biological Rhythms Lecture S1Document27 pagesBiological Rhythms Lecture S1Geerthana ArasuNo ratings yet

- DR K MangayarkarasiDocument5 pagesDR K MangayarkarasiGeerthana ArasuNo ratings yet

- The Chola Architecture: A Dravidan Style Gleand From Kailasanatha Temple at Sembianmahadevi R. Vennila & Dr. A. SrinivasanDocument4 pagesThe Chola Architecture: A Dravidan Style Gleand From Kailasanatha Temple at Sembianmahadevi R. Vennila & Dr. A. SrinivasanGeerthana ArasuNo ratings yet

- Moonlighting - An Impact Assessment Vis A Vis Labour Legislations in India - Taxguru - inDocument3 pagesMoonlighting - An Impact Assessment Vis A Vis Labour Legislations in India - Taxguru - inGeerthana ArasuNo ratings yet

- Child PsychologyDocument20 pagesChild PsychologyGeerthana ArasuNo ratings yet

- Uber Driver Gig EconomyDocument6 pagesUber Driver Gig EconomyGeerthana ArasuNo ratings yet

- Gig Economy ChallegesDocument8 pagesGig Economy ChallegesGeerthana ArasuNo ratings yet

- Gig and Platform Workers A Way Towards Formal Labour RecognitionDocument10 pagesGig and Platform Workers A Way Towards Formal Labour RecognitionGeerthana ArasuNo ratings yet

- FIRM PROFILE - (Gitonga, Kinyanjui & Co.) 2011Document9 pagesFIRM PROFILE - (Gitonga, Kinyanjui & Co.) 2011Mopa MpknNo ratings yet

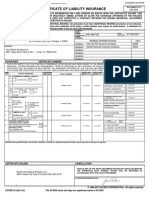

- CertificateOfInsurance - GeminiDocument1 pageCertificateOfInsurance - Geminiganesh gaddeNo ratings yet

- Impact of Financial and Non Financial Rewards On Employee MotivationDocument12 pagesImpact of Financial and Non Financial Rewards On Employee MotivationAswathy UdayabhanuNo ratings yet

- Manila Mahogany V CADocument3 pagesManila Mahogany V CAMICAELA NIALANo ratings yet

- La Excellence Goverment Schemes 2020Document126 pagesLa Excellence Goverment Schemes 2020SoumyAdeep HazarikaNo ratings yet

- October Month Current AffairsDocument87 pagesOctober Month Current AffairsSantosh Kumar ChallaNo ratings yet

- Rules: The Ancient Order of Foresters Friendly Society LimitedDocument45 pagesRules: The Ancient Order of Foresters Friendly Society LimitedFuzzy_Wood_PersonNo ratings yet

- Product Disclosure Sheet, 0Document2 pagesProduct Disclosure Sheet, 0Yusuf Md HusainNo ratings yet

- MIS770 Foundation Skills in Data Analysis T2 2019 Assignment 2Document8 pagesMIS770 Foundation Skills in Data Analysis T2 2019 Assignment 2Lezhou DUNo ratings yet

- Business Studies TermDocument9 pagesBusiness Studies TermPiyush JhamNo ratings yet

- Kilkenny Skate Park Final ReportDocument64 pagesKilkenny Skate Park Final ReportSeán Ó HArgáinNo ratings yet

- Insurance Regulatory and Development ActDocument13 pagesInsurance Regulatory and Development ActSai VasudevanNo ratings yet

- Functions of OmbudsmanDocument3 pagesFunctions of OmbudsmanSantosh KumarNo ratings yet

- Ican BrochureDocument16 pagesIcan BrochureAbhishek ShatagopachariNo ratings yet

- DBP Sheet Nexa FinalDocument26 pagesDBP Sheet Nexa FinalSameer AgrawalNo ratings yet

- CSE3S01 Session 1Document70 pagesCSE3S01 Session 1WaiLinLiNo ratings yet

- State Regulation of Rideshare CompaniesDocument3 pagesState Regulation of Rideshare CompaniesThe Council of State GovernmentsNo ratings yet

- MODULE 10 - Audit of Current Liabilities With DiscussionDocument130 pagesMODULE 10 - Audit of Current Liabilities With DiscussionDonise Ronadel SantosNo ratings yet

- Guidelines For Students (HX Joanne YIM) (Updated On 26 Oct 2020)Document22 pagesGuidelines For Students (HX Joanne YIM) (Updated On 26 Oct 2020)StephenieNo ratings yet

- Group Medicare ABCD E BrochureDocument4 pagesGroup Medicare ABCD E BrochurerawalarunNo ratings yet