You might also like

- The Art of Currency Trading: A Professional's Guide to the Foreign Exchange MarketFrom EverandThe Art of Currency Trading: A Professional's Guide to the Foreign Exchange MarketRating: 4.5 out of 5 stars4.5/5 (4)

- Manual Miniexcavadora Con Orugas 3000kg JCB Mod.8026cts 8030ztsDocument332 pagesManual Miniexcavadora Con Orugas 3000kg JCB Mod.8026cts 8030ztsGeorge Chiorean100% (4)

- BoaDocument6 pagesBoaRajiv PrasadNo ratings yet

- Is Relationship Exist Between Current Account Deficit and Fiscal Deficit The Case of IndiaDocument16 pagesIs Relationship Exist Between Current Account Deficit and Fiscal Deficit The Case of IndiaSeema PhougatNo ratings yet

- Oleh: Aditya Novianto / NIM: C2B606001 Dosen Pembimbing: Drs. Nugroho SBM, MSPDocument30 pagesOleh: Aditya Novianto / NIM: C2B606001 Dosen Pembimbing: Drs. Nugroho SBM, MSPEndi NugrohoNo ratings yet

- Indo Monetary PolicyDocument11 pagesIndo Monetary PolicyBoyke P SiraitNo ratings yet

- International Value Investing (Updated)Document11 pagesInternational Value Investing (Updated)eric_stNo ratings yet

- Analisis Efektivitas Penerapan Inflation Targeting Framework (Itf) Dalam Menjaga Stabilitas Ekonomi IndonesiaDocument9 pagesAnalisis Efektivitas Penerapan Inflation Targeting Framework (Itf) Dalam Menjaga Stabilitas Ekonomi IndonesiaCamelia HamidahNo ratings yet

- 18-Article Text-94-1-10-20200929Document14 pages18-Article Text-94-1-10-20200929Angela SolanaNo ratings yet

- 1237-Article Text-3389-2-10-20200212Document20 pages1237-Article Text-3389-2-10-20200212avicenna.deskartian.margani-2020No ratings yet

- ARDL Panel Strength in Detecting Economic Stability Leading Indicators Toward CIVI CountriesDocument9 pagesARDL Panel Strength in Detecting Economic Stability Leading Indicators Toward CIVI CountriesaijbmNo ratings yet

- Staf Pengajar Fakultas Ekonomi Dan Bisnis Universitas Pembangunan Panca Budi MedanDocument9 pagesStaf Pengajar Fakultas Ekonomi Dan Bisnis Universitas Pembangunan Panca Budi MedanCamelia HamidahNo ratings yet

- Leverage Financial DistressDocument16 pagesLeverage Financial DistressNurcahyonoNo ratings yet

- Jurnal Kajian Ekonomi, Januari 2013, Vol. I, No. 02: Dr. Hasdi Aimon, M.Si Adalah Dosen Fakultas Ekonomi UNPDocument15 pagesJurnal Kajian Ekonomi, Januari 2013, Vol. I, No. 02: Dr. Hasdi Aimon, M.Si Adalah Dosen Fakultas Ekonomi UNPstaticNo ratings yet

- Analisis Pengaruh Indikator Makroekonomi Dan Indeks Saham Regional Asean Terhadap Pasar Saham Indonesia (Ihsg) Periode Pada Tahun 2009-2014Document17 pagesAnalisis Pengaruh Indikator Makroekonomi Dan Indeks Saham Regional Asean Terhadap Pasar Saham Indonesia (Ihsg) Periode Pada Tahun 2009-2014Fadil YmNo ratings yet

- 325-Article Text-597-1-10-20150720 PDFDocument20 pages325-Article Text-597-1-10-20150720 PDFDiksNo ratings yet

- Analisis Pengaruh Inflasi, Suku Bunga Kredit, Pendapatan Per Kapita Terhadap Penanaman Modal Dalam Negeri Di IndonesiaDocument19 pagesAnalisis Pengaruh Inflasi, Suku Bunga Kredit, Pendapatan Per Kapita Terhadap Penanaman Modal Dalam Negeri Di IndonesiaEllisyaNo ratings yet

- 32 - Botis SDocument8 pages32 - Botis SEne Emanuel-StefanNo ratings yet

- Boxed: Income Inequality and Economic Segregation in Indonesia Metropolitan CitiesDocument2 pagesBoxed: Income Inequality and Economic Segregation in Indonesia Metropolitan CitiesUshaAdelinaNo ratings yet

- Rosellon Medalla 16 Elements of Competency Outlined in The Engineers Australia Stage 1 Standard For Professional EngineerDocument22 pagesRosellon Medalla 16 Elements of Competency Outlined in The Engineers Australia Stage 1 Standard For Professional EngineerDarrell BarisNo ratings yet

- Bici - Thomo-Methodology of TFR-engDocument12 pagesBici - Thomo-Methodology of TFR-engcourses.mesojNo ratings yet

- Jurnal 1 CDocument14 pagesJurnal 1 CCakra WicaksonoNo ratings yet

- Anti-Crisis Measures of Economic Policy in Lithuania and in Other Baltic CountriesDocument8 pagesAnti-Crisis Measures of Economic Policy in Lithuania and in Other Baltic CountriesDragan KaranovicNo ratings yet

- Macroeconomic Overview of The Philippines and The New Industrial Policy (2017)Document22 pagesMacroeconomic Overview of The Philippines and The New Industrial Policy (2017)DiegoNo ratings yet

- Maruti SuzukiDocument13 pagesMaruti SuzukildhboyNo ratings yet

- EN Memo Meat Processing Plant in Ukraine Confidential PDFDocument32 pagesEN Memo Meat Processing Plant in Ukraine Confidential PDFТарас ГолубNo ratings yet

- CIA1 - Ecotrix WordDocument6 pagesCIA1 - Ecotrix WordSrestha DasNo ratings yet

- Effects of Macroeconomic Conditionson Non-Performing Loan in Retail SegmentsDocument10 pagesEffects of Macroeconomic Conditionson Non-Performing Loan in Retail SegmentsVivi OktaviaNo ratings yet

- Inflation in IndonesiaDocument9 pagesInflation in IndonesiaNaurah Atika DinaNo ratings yet

- Finance ProjectDocument33 pagesFinance ProjectPratyush RaychaudhuriNo ratings yet

- Procuratio: e-ISSN 2580-3743 128Document18 pagesProcuratio: e-ISSN 2580-3743 128Shimaa AaNo ratings yet

- 2017 Y12 Chapter 5 - CDDocument22 pages2017 Y12 Chapter 5 - CDSourish IyengarNo ratings yet

- On Determinat of THB USDDocument9 pagesOn Determinat of THB USDayu cantikNo ratings yet

- Admin, Hantono Dan Luther Girsang (UNPRI MEDAN)Document12 pagesAdmin, Hantono Dan Luther Girsang (UNPRI MEDAN)arjuna pangalengan2No ratings yet

- Pengaruh Ekspor, Nilai Tukar Rupiah, Dan Penanaman Modal Asing Terhadap Cadangan Devisa Indonesia Tahun 2004-2018Document16 pagesPengaruh Ekspor, Nilai Tukar Rupiah, Dan Penanaman Modal Asing Terhadap Cadangan Devisa Indonesia Tahun 2004-2018arifNo ratings yet

- E2: Exchange Rates: Sterling Exchange Rate Index (SERI)Document1 pageE2: Exchange Rates: Sterling Exchange Rate Index (SERI)Ruchit DoshiNo ratings yet

- Factors Affecting The Fluctuations in Exchange Rate of The Indian Rupee Group 9 C2Document11 pagesFactors Affecting The Fluctuations in Exchange Rate of The Indian Rupee Group 9 C2Karishma Satheesh KumarNo ratings yet

- Fluktuasi Kurs Valuta Asing Di Beberapa Negara Asia TenggaraDocument22 pagesFluktuasi Kurs Valuta Asing Di Beberapa Negara Asia TenggaraRazji ReyhanNo ratings yet

- Report On Macroeconomics & Banking 061110Document18 pagesReport On Macroeconomics & Banking 061110Dheeraj GoelNo ratings yet

- 9708 - s11 - QP - 23 - Case Study ResponseDocument5 pages9708 - s11 - QP - 23 - Case Study ResponseZainab SiddiqueNo ratings yet

- The Evolution of The USDDocument9 pagesThe Evolution of The USDnkvkdkmskNo ratings yet

- Market Update July2011Document15 pagesMarket Update July2011Vinod KumarNo ratings yet

- An Impact of Currency Fluctuations On Indian Stock MarketDocument6 pagesAn Impact of Currency Fluctuations On Indian Stock MarketInternational Journal of Application or Innovation in Engineering & ManagementNo ratings yet

- Africa's Growing Debt Crisis: Who Is The Debt Owed To?Document24 pagesAfrica's Growing Debt Crisis: Who Is The Debt Owed To?Liu YanNo ratings yet

- Effects of Food Price Inflation On Infant and Child Mortality in Developing CountriesDocument17 pagesEffects of Food Price Inflation On Infant and Child Mortality in Developing CountriesbibrevNo ratings yet

- Pengaruh Penanaman Modal Asing Terhadap PertumbuhaDocument12 pagesPengaruh Penanaman Modal Asing Terhadap PertumbuhaAninditha IshiikaputNo ratings yet

- On Falling Neutral Real Rates Fiscal Policy and The Risk of Secular StagnationDocument68 pagesOn Falling Neutral Real Rates Fiscal Policy and The Risk of Secular StagnationjackefellerNo ratings yet

- 018 Icber2012 N10017Document5 pages018 Icber2012 N10017Anggi BoomNo ratings yet

- Seminar DrafDocument16 pagesSeminar DrafSanthe SekarNo ratings yet

- 02 Article Anirudh NarulaDocument17 pages02 Article Anirudh NarulaPrashant Gupta, RishikeshNo ratings yet

- Dampak Makroekonomi Terhadap Indeks Harga Saham Sektor Properti Di Indonesia Periode Tahun 1994-2012Document13 pagesDampak Makroekonomi Terhadap Indeks Harga Saham Sektor Properti Di Indonesia Periode Tahun 1994-2012Wahyu SubhanNo ratings yet

- Rupee Volatility, Causes, Effects, & RemediesDocument26 pagesRupee Volatility, Causes, Effects, & RemediesMonty ShethNo ratings yet

- Nertila FeruliDocument69 pagesNertila FerulisuelaNo ratings yet

- Pengaruh Indeks Saham Global Dan Kondisi Makro Indonesia Terhadap Indeks Harga Saham Gabungan Bursa Efek IndonesiaDocument18 pagesPengaruh Indeks Saham Global Dan Kondisi Makro Indonesia Terhadap Indeks Harga Saham Gabungan Bursa Efek IndonesiaIlham MaulanaNo ratings yet

- The Indian Rupee CrisisDocument10 pagesThe Indian Rupee CrisisArjun Khosla100% (1)

- Presentation: REALTOR® University Forum: Economic & Real Estate Outlook 05-21-2018Document9 pagesPresentation: REALTOR® University Forum: Economic & Real Estate Outlook 05-21-2018National Association of REALTORS®No ratings yet

- BX View On 2011 - Wein Oct 2010Document60 pagesBX View On 2011 - Wein Oct 2010anujbahalNo ratings yet

- Dynamics of Indonesia S International Trade A V - 2012 - Procedia Economics andDocument11 pagesDynamics of Indonesia S International Trade A V - 2012 - Procedia Economics andTest AccountNo ratings yet

- Keeping Banks SafeDocument19 pagesKeeping Banks SafeRajat MittalNo ratings yet

- Africa Emerging MarketDocument19 pagesAfrica Emerging MarketSuhrab Khan JamaliNo ratings yet

- Inflation: Table 7.1: Historical Trend in Headline Inflation (FY) CPI Food Non-FoodDocument13 pagesInflation: Table 7.1: Historical Trend in Headline Inflation (FY) CPI Food Non-FoodMudassirNo ratings yet

- EIB Working Papers 2019/09 - The impact of international financial institutions on SMEs: The case of EIB lending in Central and Eastern EuropeFrom EverandEIB Working Papers 2019/09 - The impact of international financial institutions on SMEs: The case of EIB lending in Central and Eastern EuropeNo ratings yet

- Novak 2012 NeurosciBiobehavRev Wheel ReviewDocument14 pagesNovak 2012 NeurosciBiobehavRev Wheel ReviewMoko NugrohoNo ratings yet

- Additional Chord For LargoDocument1 pageAdditional Chord For LargoMoko NugrohoNo ratings yet

- Elcoro 2008Document8 pagesElcoro 2008Moko NugrohoNo ratings yet

- Instrument Guides Electric Guitar D 8 2018 2Document7 pagesInstrument Guides Electric Guitar D 8 2018 2Moko NugrohoNo ratings yet

- The Effects of A Choice Test Between FooDocument8 pagesThe Effects of A Choice Test Between FooMoko NugrohoNo ratings yet

- The Lass of Patie's Mil in CDocument1 pageThe Lass of Patie's Mil in CMoko NugrohoNo ratings yet

- Here I Am DrumDocument2 pagesHere I Am DrumMoko NugrohoNo ratings yet

- Pratten Easy Progressive No2 WernerDocument1 pagePratten Easy Progressive No2 WernerMoko NugrohoNo ratings yet

- Cantata 147Document1 pageCantata 147Moko NugrohoNo ratings yet

- Cantata 147PianoGuitarDocument3 pagesCantata 147PianoGuitarMoko NugrohoNo ratings yet

- Bass SpiritDocument1 pageBass SpiritMoko NugrohoNo ratings yet

- BWV 114 From The Notebook of Anna Magdalena Bach 1720: Moderato Moderato Moderato Moderato QDocument2 pagesBWV 114 From The Notebook of Anna Magdalena Bach 1720: Moderato Moderato Moderato Moderato QMoko NugrohoNo ratings yet

- As The DeerDocument1 pageAs The DeerMoko NugrohoNo ratings yet

- Mertz Study On EDocument2 pagesMertz Study On EMoko NugrohoNo ratings yet

- First Ride by Don RossDocument11 pagesFirst Ride by Don RossMoko NugrohoNo ratings yet

- Ballade Pour Adeline by Richard Clayderman Guitare 1Document3 pagesBallade Pour Adeline by Richard Clayderman Guitare 1Moko NugrohoNo ratings yet

- Dejan Brosura 20161Document12 pagesDejan Brosura 20161Moko NugrohoNo ratings yet

- Primary Chords HandoutDocument1 pagePrimary Chords HandoutMoko NugrohoNo ratings yet

- Yamko Rambe Yamko Bass Only No DrumDocument2 pagesYamko Rambe Yamko Bass Only No DrumMoko NugrohoNo ratings yet

- Feliz Navidad Duet Guitar Score Sheet MusicDocument5 pagesFeliz Navidad Duet Guitar Score Sheet MusicMoko NugrohoNo ratings yet

- Teachers of YesteryearDocument12 pagesTeachers of YesteryearJesy Vergel PampilonNo ratings yet

- Toeic Writing EssayDocument37 pagesToeic Writing EssayThư NguyễnNo ratings yet

- HP Insight Management Agents User GuideDocument98 pagesHP Insight Management Agents User GuideChentaoNo ratings yet

- Deb58tis 4Document11 pagesDeb58tis 4CHEMA BASANNo ratings yet

- MIG-200L ManualDocument30 pagesMIG-200L ManualV-Man systemNo ratings yet

- Magelis XBTN enDocument186 pagesMagelis XBTN enPedro BarbosaNo ratings yet

- Hänchen Overview PDFDocument19 pagesHänchen Overview PDFBruno CecattoNo ratings yet

- 118: The Mill, Llanddewi Skirrid, Abergavenny. Watching BriefDocument20 pages118: The Mill, Llanddewi Skirrid, Abergavenny. Watching BriefAPAC LtdNo ratings yet

- Nokia Asha 206 Schematic DiagramDocument4 pagesNokia Asha 206 Schematic Diagramحسين أمينNo ratings yet

- Design and Implementation of Motion Detector With Alarm SystemDocument48 pagesDesign and Implementation of Motion Detector With Alarm SystemFarukNo ratings yet

- Ipc2022 - 87345 Enhancement of Mechanical Damage Crack EvaluationDocument12 pagesIpc2022 - 87345 Enhancement of Mechanical Damage Crack EvaluationOswaldo MontenegroNo ratings yet

- Account StatementDocument132 pagesAccount StatementBASHA SHAFIQNo ratings yet

- Policies To Promote Renewable Energy and Enhance Energy Security in Central AsiaDocument16 pagesPolicies To Promote Renewable Energy and Enhance Energy Security in Central AsiaADBI EventsNo ratings yet

- A Mixed Integer Linear Program For Airport Departure SchedulingDocument13 pagesA Mixed Integer Linear Program For Airport Departure SchedulingDang Khoa NgoNo ratings yet

- 6 - Percentage CompositionDocument2 pages6 - Percentage CompositionAugene BoncalesNo ratings yet

- Wireless Communications MCQDocument20 pagesWireless Communications MCQRenisha BennoNo ratings yet

- ACC702 Course Material Study GuideDocument78 pagesACC702 Course Material Study Guidethùy TrầnNo ratings yet

- Unchuan Vs TabamoDocument4 pagesUnchuan Vs TabamoMichael Kevin MangaoNo ratings yet

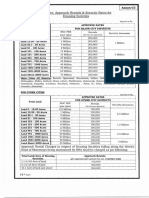

- Annex-C3 NOC Fee, Approach Rentals 86 Security Rates For Housing SocietiesDocument1 pageAnnex-C3 NOC Fee, Approach Rentals 86 Security Rates For Housing SocietiesSaqib RazaNo ratings yet

- Cryptography and Network Security Two Marks Unit-1 Network Security 1. Specify The Four Categories of Security Threads?Document11 pagesCryptography and Network Security Two Marks Unit-1 Network Security 1. Specify The Four Categories of Security Threads?PiriyangaNo ratings yet

- AnaValid-ProtocSécurité V3.1Document15 pagesAnaValid-ProtocSécurité V3.1nyamsi claude bernardNo ratings yet

- Raaj SipDocument76 pagesRaaj SipAdarsh VermaNo ratings yet

- Hitachi Tu-Hd1000Document47 pagesHitachi Tu-Hd1000Javier Sanchez SanchezNo ratings yet

- Mengetik Arab Menggunakan Microsoft Office 2007Document8 pagesMengetik Arab Menggunakan Microsoft Office 2007alfeddsNo ratings yet

- DATA - SHEET - Altratene 30% OS-SF - June 2018Document1 pageDATA - SHEET - Altratene 30% OS-SF - June 2018maha guettariNo ratings yet

- D 2119 - 96 - RdixmtktukveDocument4 pagesD 2119 - 96 - RdixmtktukveRaphael CordovaNo ratings yet

- Biodata of DR V K RainaDocument7 pagesBiodata of DR V K RainapaspaNo ratings yet