You might also like

- Does Weak Governance Cause Weak Stock Returns An Examination of Firm Operating Performance and Investors' ExpectationsDocument33 pagesDoes Weak Governance Cause Weak Stock Returns An Examination of Firm Operating Performance and Investors' ExpectationsikangNo ratings yet

- Earnings ManagementDocument32 pagesEarnings ManagementMathilda ChanNo ratings yet

- Kim Heessoo 10621377 BSC ECBDocument20 pagesKim Heessoo 10621377 BSC ECBatktaouNo ratings yet

- Milena 2012Document47 pagesMilena 2012rehan44No ratings yet

- Long-run IPO performance analysis of UK and German firmsDocument5 pagesLong-run IPO performance analysis of UK and German firmsOm PatelNo ratings yet

- The Market Disciplinary Effect of Asset Write-Off: Theory and Empirical Evidence From Goodwill ImpairmentDocument68 pagesThe Market Disciplinary Effect of Asset Write-Off: Theory and Empirical Evidence From Goodwill ImpairmentYupeng LinNo ratings yet

- Determinants of Corporate Capital Structure Under Different Debt Maturities (2011)Document8 pagesDeterminants of Corporate Capital Structure Under Different Debt Maturities (2011)Lê DiệuNo ratings yet

- Subba ReddyDocument47 pagesSubba Reddyankitjaipur0% (1)

- Yu 2011Document15 pagesYu 2011atktaouNo ratings yet

- Dividend Declaration and Stock Price Behavior: Indian EvidencesDocument11 pagesDividend Declaration and Stock Price Behavior: Indian EvidencesAKASHNo ratings yet

- How Stock Issuance Predicts Factor ReturnsDocument38 pagesHow Stock Issuance Predicts Factor Returnsresat gürNo ratings yet

- Does Dividend Policy Foretell Earnings Growth?: Draft: December 2001 Comments WelcomeDocument34 pagesDoes Dividend Policy Foretell Earnings Growth?: Draft: December 2001 Comments WelcomeSnehanshu BanerjeeNo ratings yet

- Fama 1998Document25 pagesFama 1998Rizqi NadhirohNo ratings yet

- Print 4Document32 pagesPrint 4Himanshu JainNo ratings yet

- The IPO Derby: Are There Consistent Losers and Winners On This Track?Document36 pagesThe IPO Derby: Are There Consistent Losers and Winners On This Track?phuongthao241No ratings yet

- Corporate PuzzleDocument61 pagesCorporate PuzzlesimplyankurguptaNo ratings yet

- Dynamics and Determinants of Dividend Policy in Pakistan (Evidence From Karachi Stock Exchange Non-Financial Listed Firms)Document4 pagesDynamics and Determinants of Dividend Policy in Pakistan (Evidence From Karachi Stock Exchange Non-Financial Listed Firms)Junejo MichaelNo ratings yet

- Catering Theory by Baker & WurglerDocument42 pagesCatering Theory by Baker & Wurglerarchaudhry130No ratings yet

- Report On Dividend PolicyDocument21 pagesReport On Dividend PolicyMd. Golam Mortuza78% (9)

- An international analysis of earnings, stock prices andDocument38 pagesAn international analysis of earnings, stock prices andelielo0604No ratings yet

- CampelloSaffi15 PDFDocument39 pagesCampelloSaffi15 PDFdreamjongenNo ratings yet

- Fuwei JiangDocument58 pagesFuwei JiangDr. Naveed Hussain Shah Assistant Professor Department of Management SciencesNo ratings yet

- Do Tracking Stocks Reduce Informational Asymmetries by Elder Et Al. (JFR 2005)Document18 pagesDo Tracking Stocks Reduce Informational Asymmetries by Elder Et Al. (JFR 2005)Eleanor RigbyNo ratings yet

- Do Mergers Create or Destroy Value? Evidence From Unsuccessful MergersDocument26 pagesDo Mergers Create or Destroy Value? Evidence From Unsuccessful MergersemkaysubhaNo ratings yet

- Corporate Governance and Capital Structure DynamicsDocument63 pagesCorporate Governance and Capital Structure Dynamicskrenari68No ratings yet

- Main Chapter TwoDocument10 pagesMain Chapter TwoNicholas Mensah100% (1)

- Main Chapter TwoDocument10 pagesMain Chapter TwoNicholas MensahNo ratings yet

- Liu NguyenDocument33 pagesLiu NguyenYulianita AdrimaNo ratings yet

- Control and Bank Performance: Lawrence Fogelberg and John M. GriffithDocument7 pagesControl and Bank Performance: Lawrence Fogelberg and John M. GriffithArie ToddopuliNo ratings yet

- Dampak Manajemen Laba Terhadap Alokasi Investasi Perusahaan Siti RokhaniyahDocument11 pagesDampak Manajemen Laba Terhadap Alokasi Investasi Perusahaan Siti RokhaniyahRossita SariNo ratings yet

- Is The Market Surprised by Poor Earnings Realizations Following Seasoned Equity Offerings?Document41 pagesIs The Market Surprised by Poor Earnings Realizations Following Seasoned Equity Offerings?cipsfuyNo ratings yet

- Backdate 08182009 1Document37 pagesBackdate 08182009 1Yu Hua AnNo ratings yet

- SSRN Id770805Document47 pagesSSRN Id770805mishuk77No ratings yet

- Determinants of Dividend Policy in Saudi Listed CompaniesDocument10 pagesDeterminants of Dividend Policy in Saudi Listed CompaniesChickenrock TangerangNo ratings yet

- By Suleiman, Hamisu Kargi Phd/Admin/11934/2008-2009Document26 pagesBy Suleiman, Hamisu Kargi Phd/Admin/11934/2008-2009Lareb ShaikhNo ratings yet

- 7.5.2013 The Bumpy Road To OutperformanceDocument8 pages7.5.2013 The Bumpy Road To OutperformanceTBP_Think_TankNo ratings yet

- The Relationship Between Information Asymmetry and Dividend PolicyPapDocument56 pagesThe Relationship Between Information Asymmetry and Dividend PolicyPapRaj KumarNo ratings yet

- Stock SplitDocument36 pagesStock SplitSivakarthik SubramanianNo ratings yet

- Capital Structure, Cost of Debt and Dividend Payout of Firms in New York and Shanghai Stock ExchangesDocument9 pagesCapital Structure, Cost of Debt and Dividend Payout of Firms in New York and Shanghai Stock ExchangesDevikaNo ratings yet

- Detect Earnings Manipulation with Discretionary Accrual ModelsDocument34 pagesDetect Earnings Manipulation with Discretionary Accrual ModelsAlmizan AbadiNo ratings yet

- Can Mutual Fund Managers Pick Stocks? Evidence From Their Trades Prior To Earnings AnnouncementsDocument34 pagesCan Mutual Fund Managers Pick Stocks? Evidence From Their Trades Prior To Earnings AnnouncementsHendri AnjayantoNo ratings yet

- Sje 22 2 263Document26 pagesSje 22 2 263Enerel Otgonbayar (Eny)No ratings yet

- IraniOesch AnalystCoverageEarningsManagementDocument48 pagesIraniOesch AnalystCoverageEarningsManagementshadoNo ratings yet

- Do Dividends Forecast Future EarningsDocument57 pagesDo Dividends Forecast Future EarningsatktaouNo ratings yet

- Dividend Policy of Indian Corporate FirmsDocument19 pagesDividend Policy of Indian Corporate FirmsRoads Sub Division-I,PuriNo ratings yet

- Dividend PolicyDocument8 pagesDividend PolicyHarsh SethiaNo ratings yet

- Review of LiteratureDocument9 pagesReview of Literaturesonabeta07No ratings yet

- Testing The Pecking Order Theory: The Impact of Financing Surpluses and Large Financing DeficitsDocument40 pagesTesting The Pecking Order Theory: The Impact of Financing Surpluses and Large Financing DeficitsatktaouNo ratings yet

- Earnings Management and The Post-Earnings Announcement DriftDocument54 pagesEarnings Management and The Post-Earnings Announcement DriftIosiasNo ratings yet

- Corporate Focus Drives Stock ReturnsDocument21 pagesCorporate Focus Drives Stock ReturnsCẩm Anh ĐỗNo ratings yet

- Stock Performance or Entrenchment? The Effects of Mergers and Acquisitions On CEO CompensationDocument55 pagesStock Performance or Entrenchment? The Effects of Mergers and Acquisitions On CEO CompensationLoren SteffyNo ratings yet

- Yale Spring Load AccountingDocument44 pagesYale Spring Load AccountingMessina04No ratings yet

- Financial Performance Impact on Stock PricesDocument14 pagesFinancial Performance Impact on Stock PricesMuhammad Yasir YaqoobNo ratings yet

- Thesis On Determinants of Capital StructureDocument4 pagesThesis On Determinants of Capital Structuredwbeqxpb100% (2)

- Investor Behavior and The Timing of Secondary Equity OfferingsDocument43 pagesInvestor Behavior and The Timing of Secondary Equity Offeringsteeravac vacNo ratings yet

- Agency Costs and The Dividend DecisionDocument17 pagesAgency Costs and The Dividend DecisionhhhhhhhNo ratings yet

- Does Corporate Performance Determine Capital Structure and Dividend Policy?Document57 pagesDoes Corporate Performance Determine Capital Structure and Dividend Policy?DevikaNo ratings yet

- EIB Working Papers 2018/08 - Debt overhang and investment efficiencyFrom EverandEIB Working Papers 2018/08 - Debt overhang and investment efficiencyNo ratings yet

- Empirical Note on Debt Structure and Financial Performance in Ghana: Financial Institutions' PerspectiveFrom EverandEmpirical Note on Debt Structure and Financial Performance in Ghana: Financial Institutions' PerspectiveNo ratings yet

- The Declaration of Dependence: Dividends in the Twenty-First CenturyFrom EverandThe Declaration of Dependence: Dividends in the Twenty-First CenturyNo ratings yet

- IBFS Case - Rights Issue - Godrej Consumers (Group 1 - WMP13) - V3.0Document8 pagesIBFS Case - Rights Issue - Godrej Consumers (Group 1 - WMP13) - V3.0ProfessorAsim Kumar MishraNo ratings yet

- Bill FincgDocument16 pagesBill FincgProfessorAsim Kumar MishraNo ratings yet

- Divid PolicyDocument15 pagesDivid PolicyProfessorAsim Kumar Mishra100% (1)

- Post Merger ManagementDocument6 pagesPost Merger ManagementProfessorAsim Kumar MishraNo ratings yet

- KNR Construction - Book BuildingDocument11 pagesKNR Construction - Book BuildingProfessorAsim Kumar MishraNo ratings yet

- Group 2 Campbell Corpor DebtDocument9 pagesGroup 2 Campbell Corpor DebtProfessorAsim Kumar MishraNo ratings yet

- Analysis of Continuing ValueDocument8 pagesAnalysis of Continuing ValueProfessorAsim Kumar MishraNo ratings yet

- Announcement Effects of Bonus Issues On Equity Prices: The Indian ExperienceDocument15 pagesAnnouncement Effects of Bonus Issues On Equity Prices: The Indian ExperienceProfessorAsim Kumar MishraNo ratings yet

- Destin Brass Case SolDocument2 pagesDestin Brass Case SolProfessorAsim Kumar MishraNo ratings yet

- Stock MKT Pred CHRTDocument2 pagesStock MKT Pred CHRTProfessorAsim Kumar MishraNo ratings yet

- Short Term Sources of FinanceDocument18 pagesShort Term Sources of FinanceJithin Krishnan100% (1)

- DIP GuidelinesDocument11 pagesDIP GuidelinesProfessorAsim Kumar MishraNo ratings yet

- Horary and Sublord in RetroDocument1 pageHorary and Sublord in RetroProfessorAsim Kumar MishraNo ratings yet

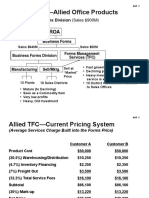

- ABC Costing Allied Office ProductsDocument13 pagesABC Costing Allied Office ProductsProfessorAsim Kumar Mishra100% (1)

- ARS AllRapidShare 3.0Document1 pageARS AllRapidShare 3.0ProfessorAsim Kumar MishraNo ratings yet

- TMP For AstroDocument4 pagesTMP For AstroProfessorAsim Kumar MishraNo ratings yet

- 8th House in MarriageDocument3 pages8th House in MarriageProfessorAsim Kumar MishraNo ratings yet

- Bill DiscountingDocument69 pagesBill DiscountingDhanesh BabarNo ratings yet

- 12 Signs of The ZodiacDocument9 pages12 Signs of The ZodiacProfessorAsim Kumar MishraNo ratings yet

- 12 Houses SignifyDocument7 pages12 Houses SignifyProfessorAsim Kumar MishraNo ratings yet

- "Simple Rules of 4 Step Theory": Rule 1Document5 pages"Simple Rules of 4 Step Theory": Rule 1SaptarishisAstrology100% (2)

- JASA Mar Apr 2012 IssueDocument104 pagesJASA Mar Apr 2012 IssueandrewduttaNo ratings yet

- KP Reader 3 Pg. 314Document5 pagesKP Reader 3 Pg. 314ProfessorAsim Kumar MishraNo ratings yet

- Nov-Dec 2011 Issue of JASADocument0 pagesNov-Dec 2011 Issue of JASAProfessorAsim Kumar MishraNo ratings yet

- Jasa Sep-Oct 2011 - 1Document0 pagesJasa Sep-Oct 2011 - 1ProfessorAsim Kumar MishraNo ratings yet

- KP Reader 3 Pg. 160Document5 pagesKP Reader 3 Pg. 160ProfessorAsim Kumar MishraNo ratings yet

- Nak ChintaDocument5 pagesNak ChintaProfessorAsim Kumar MishraNo ratings yet

- Journal For Advancement of Stellar AstrologyDocument95 pagesJournal For Advancement of Stellar Astrologyandrew_dutta67% (3)

- JASA May-Jun 2012 IssueDocument106 pagesJASA May-Jun 2012 IssueandrewduttaNo ratings yet

- JASA Oct-Dec 2013 IssueDocument116 pagesJASA Oct-Dec 2013 Issuekumarkumar123No ratings yet

- The Risk and Return Analysis of Equity Fund in Sundaram Mutual FundDocument102 pagesThe Risk and Return Analysis of Equity Fund in Sundaram Mutual Fundmallesha02No ratings yet

- Roles Functions Of: & SebiDocument14 pagesRoles Functions Of: & SebiJeffry MahiNo ratings yet

- Britannia Annual Report 2016-17Document232 pagesBritannia Annual Report 2016-17Naampreet Singh0% (1)

- Rospectus: SynopsisDocument13 pagesRospectus: SynopsisKeshav LaddhaNo ratings yet

- Fundamentals of Investment Management 10th Edition Hirt Solutions ManualDocument15 pagesFundamentals of Investment Management 10th Edition Hirt Solutions Manualtanyacookeajtzmonrd100% (28)

- Introduction To Financial ManagementDocument24 pagesIntroduction To Financial ManagementKabile MwitaNo ratings yet

- Cityam 2011-07-05Document28 pagesCityam 2011-07-05City A.M.No ratings yet

- Noarbitrage Eq To Risk Neutral ExistanceDocument46 pagesNoarbitrage Eq To Risk Neutral ExistanceJack SmithNo ratings yet

- United States Court of Appeals, Fourth CircuitDocument10 pagesUnited States Court of Appeals, Fourth CircuitScribd Government DocsNo ratings yet

- Class 12 - Payout Policy - 1Document1 pageClass 12 - Payout Policy - 1Stepan MaykovNo ratings yet

- CFA Career Guide India 2023Document80 pagesCFA Career Guide India 2023Anmol Arjun100% (1)

- CH 12Document9 pagesCH 12cddaniel910411No ratings yet

- Annual Report 2009 DNB Nor Bank AsaDocument114 pagesAnnual Report 2009 DNB Nor Bank AsaFrode HaukenesNo ratings yet

- Dimensional Service Corporation 2307Document3 pagesDimensional Service Corporation 2307Randy RosasNo ratings yet

- Financial Astrology vs. Business Astrology:: Comparing SystemsDocument25 pagesFinancial Astrology vs. Business Astrology:: Comparing Systemsrajasekharchilukuri100% (1)

- Panduan D'ONE Trade Pro IndonesiaDocument293 pagesPanduan D'ONE Trade Pro Indonesiaanto donlotNo ratings yet

- Sr. No Subject NoDocument5 pagesSr. No Subject NoKailash Chandra PradhanNo ratings yet

- 03 Banking CH 3 Ana 4Document57 pages03 Banking CH 3 Ana 4sabit hussenNo ratings yet

- Bloomberg Businessweek. 11 July 2004. Retrieved 29 December 2014)Document8 pagesBloomberg Businessweek. 11 July 2004. Retrieved 29 December 2014)GowreDaughterofVivekanandaNo ratings yet

- TAXATION REVIEW: KEY CONCEPTS AND SITUATIONSDocument113 pagesTAXATION REVIEW: KEY CONCEPTS AND SITUATIONSDaryl Mae Mansay100% (1)

- ACCT 302 Financial Reporting II Lecture 7Document63 pagesACCT 302 Financial Reporting II Lecture 7Jesse NelsonNo ratings yet

- PrivateEquityFinalReport PDFDocument140 pagesPrivateEquityFinalReport PDFSachin GuptaNo ratings yet

- 104 Overall CompilationDocument363 pages104 Overall Compilation할에쉿궨No ratings yet

- All E Technologies RHPDocument295 pagesAll E Technologies RHPShrey ShahNo ratings yet

- Jharkhand VAT Rules 2006Document53 pagesJharkhand VAT Rules 2006Krushna MishraNo ratings yet

- SMC Draft Licensing GuidelineDocument51 pagesSMC Draft Licensing Guidelinekrul786No ratings yet

- Corporate Governance and Bank Performance: Evidence From BangladeshDocument7 pagesCorporate Governance and Bank Performance: Evidence From BangladeshRubel SahaNo ratings yet

- Tutorial 10-2021-PIT2 ProblemsDocument8 pagesTutorial 10-2021-PIT2 ProblemsHien Bach Thi Tra QTKD-3KT-18No ratings yet

- Adani Gets Total Push in Hydrogen Race With Ambani We'Re Hiring: PM'S Missive For 1 Million Jobs by 2024Document18 pagesAdani Gets Total Push in Hydrogen Race With Ambani We'Re Hiring: PM'S Missive For 1 Million Jobs by 2024AshisNo ratings yet

- CASE - 4 Indian Stock Market: Does It Explain Perfect Competition?Document5 pagesCASE - 4 Indian Stock Market: Does It Explain Perfect Competition?Sasi RekhaNo ratings yet