When we valuate inventory it is basically the identification and definition of monetary value of all the items in our inventory,

this process is usually initiated at the time of final accounting and preparing a statement which shoes the inventory ingredients.

Why is it important to value Inventory?

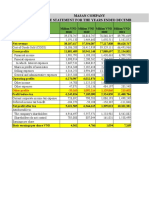

Inventory represents a large portion of companys assets and, as such, structures an essential part of the balance sheet of the company. And therefore it is of key importance for investors analyzing stocks to properly understand how inventory is valued. It is vital to value inventory since financial accounting intends at closely controlled recording and presenting of all transactions by the company. These transactions mentioned earlier are further classified into balance sheets. The idea behind inventory valuation while being an important principal asset is to depict the financial position of the company in terms of production and sales process. The amount of Sales per annum & production per annum solely depend upon the value of the inventory of the firm. In addition to the importance mentioned earlier, inventory valuation represented in form of a periodically prepared statement shown; leads to beneficial management decisions as a result of which the management reaches a well planned decision by keeping the economic factors that affect business into consideration. The decisions made include updating the inventory, method of valuation of inventory and changing a particular supply mode, etc. There are three principal ways used to properly evaluate the inventory of a firm.

1. 2. 3. First method is First- In- First- Out (FIFO) Method. Second method is Last- In- First- Out (LIFO) Method. Last method is Weighted Average Cost Method.

�Lets talk about FIFO Method first.

In this method it is assumed that when a company purchases goods it should be used in the same order as purchased, meaning that the first goods that are purchased by the company should be the first goods used which is solely a manufacturing concern or the first sold good in the merchandising concern and as a result of which the remaining inventory must represent the most recent purchase accordingly. In this method the revenues get matched against the initial cost of inventory by firm. Good business practice as of using FIFO method it is often parallel to the actual physical flow of merchandise as selling the oldest units first rather than the new ones first. We can easily explain FIFO by giving the example of a refrigerator used at our homes, when we buy grocery we put the fresh bought groceries at the back of the refrigerator and bring the old or unfinished groceries to front in order to use it as soon as possible before it spoils.

LIFO Method

In LIFO method which is totally the opposite of FIFO method as it matches the revenues against current cost of inventories and in which the newest inventory is sold first rather than the oldest inventory. By using LIFO method it is generally results in providing reports with lower net income as a result of which a lower net income will be paying less in taxes to authorities.

Weighted Average Method

Under weighted average method, this method matches revenues against the average cost of inventory by the firm. The costs of goods are divided equally or they are averaged in a way among the units of concerned inventory. In this method the costs of goods are matched against revenue according to the average of each unit of cost of sold goods. And the same weighted average unit costs derived are again used to determine the costs of the merchandise inventory when the concerned period is about to end. In weighted average method determined after dividing the total costs of units of each item that is available to sale during concerned period by related number of units of the same item.