0% found this document useful (0 votes)

42 views3 pagesManagement Accounting II Finals Quiz

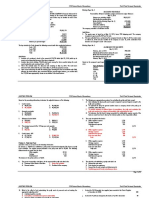

The document is a finals quiz for Management Accounting II at St. Vincent College, consisting of multiple-choice questions based on various financial scenarios. It includes problems related to equipment acquisition, cash inflows, and capital budgeting techniques. Students are instructed to select answers in capital letters on a provided answer sheet.

Uploaded by

Roselle Angela SernaCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as DOCX, PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

42 views3 pagesManagement Accounting II Finals Quiz

The document is a finals quiz for Management Accounting II at St. Vincent College, consisting of multiple-choice questions based on various financial scenarios. It includes problems related to equipment acquisition, cash inflows, and capital budgeting techniques. Students are instructed to select answers in capital letters on a provided answer sheet.

Uploaded by

Roselle Angela SernaCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as DOCX, PDF, TXT or read online on Scribd