0% found this document useful (0 votes)

41 views35 pagesLesson 3 Production

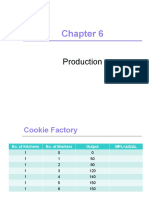

The document discusses the production decisions of firms, highlighting the importance of production technology, cost constraints, and input choices. It explains the production function, the distinction between short-run and long-run production, and the law of diminishing marginal returns. Additionally, it covers the concept of isoquants and returns to scale, illustrating how firms can optimize output by varying input combinations.

Uploaded by

rufeliofarinCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as PDF, TXT or read online on Scribd

Topics covered

- Output maximization,

- Production output,

- Fixed inputs,

- Average product,

- Labor input,

- Production output dynamics,

- Marginal rate of technical sub…,

- Production input optimization,

- Cost structure,

- Production input analysis

0% found this document useful (0 votes)

41 views35 pagesLesson 3 Production

The document discusses the production decisions of firms, highlighting the importance of production technology, cost constraints, and input choices. It explains the production function, the distinction between short-run and long-run production, and the law of diminishing marginal returns. Additionally, it covers the concept of isoquants and returns to scale, illustrating how firms can optimize output by varying input combinations.

Uploaded by

rufeliofarinCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as PDF, TXT or read online on Scribd

Topics covered

- Output maximization,

- Production output,

- Fixed inputs,

- Average product,

- Labor input,

- Production output dynamics,

- Marginal rate of technical sub…,

- Production input optimization,

- Cost structure,

- Production input analysis