You might also like

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5795)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Common Transaction SlipDocument3 pagesCommon Transaction SlipGyan Swaroop TripathiNo ratings yet

- Praktikum Keuangan MenengahDocument5 pagesPraktikum Keuangan MenengahJoseph LimbongNo ratings yet

- Type 4-Transfer Agreement+Ats - Distressed Unit To Ic Unit - Anand YadavDocument29 pagesType 4-Transfer Agreement+Ats - Distressed Unit To Ic Unit - Anand YadavNitin AgnihotriNo ratings yet

- An Experiential Case Study On Social Media in IndiaDocument40 pagesAn Experiential Case Study On Social Media in IndiaShaddi Sophia LeraNo ratings yet

- Bid Document For RWH11.5b - CompressedDocument98 pagesBid Document For RWH11.5b - CompressedAdityaGelaniNo ratings yet

- Ffs Price ListDocument41 pagesFfs Price ListLibre MenteNo ratings yet

- Internship Report On General Banking Activities of Basic BankDocument55 pagesInternship Report On General Banking Activities of Basic BankAfroza KhanomNo ratings yet

- Manupatra 7303Document2 pagesManupatra 7303Karthik SaranganNo ratings yet

- Practice Set No. 1Document6 pagesPractice Set No. 1Rexie Tan100% (2)

- 02audit of CashDocument12 pages02audit of CashJeanette FormenteraNo ratings yet

- Thomas 05.31.23Document32 pagesThomas 05.31.23Deuntae ThomasNo ratings yet

- VPS Server Configuration Guide, Detailed For Linux BeginnersDocument39 pagesVPS Server Configuration Guide, Detailed For Linux BeginnersPatricio YumisacaNo ratings yet

- CXC Principles of Business Exam Guide: Section 4: Legal Aspects of BusinessDocument2 pagesCXC Principles of Business Exam Guide: Section 4: Legal Aspects of BusinessAvril CarbonNo ratings yet

- Chapter 10: Auditing Cash and Marketable SecuritiesDocument24 pagesChapter 10: Auditing Cash and Marketable SecuritiesMerliza JusayanNo ratings yet

- Online Challan For Admission BZU MultanDocument1 pageOnline Challan For Admission BZU MultanTayyab SaleemNo ratings yet

- CAS Corporate TransactionsDocument226 pagesCAS Corporate Transactionsapi-3763163No ratings yet

- Internal Audit ManualDocument92 pagesInternal Audit ManualSudhakar Jalagam50% (2)

- 02 PDFDocument2 pages02 PDFdm.chaminda0No ratings yet

- DigiDocument4 pagesDigiWellter JitapNo ratings yet

- Cash Balance Per Bank Versus Per BookDocument6 pagesCash Balance Per Bank Versus Per BookSyrill CayetanoNo ratings yet

- Payment: Commercial CorrespondenceDocument8 pagesPayment: Commercial CorrespondencestrawberryktNo ratings yet

- Make Money Fast With Cash Fiesta (New Version)Document10 pagesMake Money Fast With Cash Fiesta (New Version)Phi Van HoeNo ratings yet

- Nov2022Document14 pagesNov2022G SNo ratings yet

- Sport Centre Management SystemDocument19 pagesSport Centre Management System5lady100% (1)

- Indoor Air Quality Solutions (Iaq) For Sustainable BuildingsDocument2 pagesIndoor Air Quality Solutions (Iaq) For Sustainable BuildingsZaw Moe KhineNo ratings yet

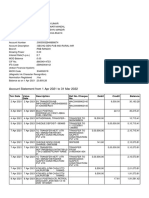

- Account Statement From 1 Apr 2021 To 31 Mar 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument14 pagesAccount Statement From 1 Apr 2021 To 31 Mar 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceRishav AnandNo ratings yet

- BA 9207 Legal AspectsDocument55 pagesBA 9207 Legal Aspectsvasanth777No ratings yet

- Negotiation of Negotiable InstrumentsDocument17 pagesNegotiation of Negotiable Instrumentsjuvilyn valeraNo ratings yet

- Bhartiya Post Jan 2007Document32 pagesBhartiya Post Jan 2007K V Sridharan General Secretary P3 NFPENo ratings yet

- Co-Operative Bank Exam Model Question Paper@PSC WINNERSDocument23 pagesCo-Operative Bank Exam Model Question Paper@PSC WINNERSSandeep Kumar75% (4)