You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (843)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5810)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (346)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Jesus Is My Help - GB Major - MN0084560Document11 pagesJesus Is My Help - GB Major - MN0084560Josue ANo ratings yet

- TLE.. ReviewerDocument3 pagesTLE.. ReviewerJohnCzyril Deladia Domens100% (1)

- Implementing IPSAS at UNHCR PDFDocument43 pagesImplementing IPSAS at UNHCR PDFrafimaneNo ratings yet

- Grant Thornton U S GAAP V IFRS ComparisonDocument90 pagesGrant Thornton U S GAAP V IFRS ComparisonjroesleNo ratings yet

- Management Advisory Services - PreboardDocument13 pagesManagement Advisory Services - PreboardAngelica Estrada100% (4)

- Report On Company ValuationDocument23 pagesReport On Company ValuationFarzana Fariha Lima100% (1)

- Uploading Asset GL Opening Balances Using OASV - F-02 Transaction - SAP BlogsDocument3 pagesUploading Asset GL Opening Balances Using OASV - F-02 Transaction - SAP BlogsManas Kumar SahooNo ratings yet

- 23 q3 Supplemental Information American TowerDocument37 pages23 q3 Supplemental Information American TowerDaniel KwanNo ratings yet

- Public Finance Management Act PFMA Course Outline BookingDocument10 pagesPublic Finance Management Act PFMA Course Outline BookingJuan G. HicksNo ratings yet

- 2.firm Performance Analysis - Seminar QuestionDocument3 pages2.firm Performance Analysis - Seminar QuestionYashrajsing LuckkanaNo ratings yet

- Exercises - Topic 3 (Impairment) (Eng)Document7 pagesExercises - Topic 3 (Impairment) (Eng)Thảo PhạmNo ratings yet

- Chapter 4 MDocument39 pagesChapter 4 MAhmed El KhateebNo ratings yet

- Precedent 4 Joint Venture Agreement (Unincorporated) To Implement Construction Contract Following ADocument10 pagesPrecedent 4 Joint Venture Agreement (Unincorporated) To Implement Construction Contract Following ASbusiNo ratings yet

- 1 CombinedDocument405 pages1 CombinedMansi aggarwal 171050No ratings yet

- Silicon Valley Bank Unit EconomicsDocument5 pagesSilicon Valley Bank Unit EconomicsPierpaolo VergatiNo ratings yet

- HW On Conceptual Framework - Part 1Document7 pagesHW On Conceptual Framework - Part 1Cha PampolinaNo ratings yet

- Inventory Management: Russell and Taylor Operations Management, 8th EditionDocument54 pagesInventory Management: Russell and Taylor Operations Management, 8th EditionLie Jasen100% (1)

- Accounting For Zoo AnimalsDocument20 pagesAccounting For Zoo AnimalsAnonymous C722KPSNo ratings yet

- Chapter 3 Corporate Liquidation and Reorganization-PROFE01Document3 pagesChapter 3 Corporate Liquidation and Reorganization-PROFE01Steffany RoqueNo ratings yet

- Liquidation of Companies - 230717 - 124515Document7 pagesLiquidation of Companies - 230717 - 124515Ruchita JanakiramNo ratings yet

- Working Capital ManagementDocument78 pagesWorking Capital ManagementPriya GowdaNo ratings yet

- Master Budget ProblemDocument2 pagesMaster Budget ProblemCillian ReevesNo ratings yet

- Chapter 20Document56 pagesChapter 20insyed9No ratings yet

- Ex Mi1Document8 pagesEx Mi1220h0367No ratings yet

- Audit Working Paper (Contoh)Document65 pagesAudit Working Paper (Contoh)Trick1 HahaNo ratings yet

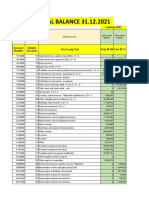

- Trial - Balance 2021-2Document24 pagesTrial - Balance 2021-2AlexandrinaCojocaruNo ratings yet

- Chapter 4 Report Problems 1 4Document8 pagesChapter 4 Report Problems 1 4Nyster Ann Rebenito100% (1)

- 3 Persed BRG-Lat2Document2 pages3 Persed BRG-Lat2hasnaglowNo ratings yet

- Statement of Financial Position 2Document25 pagesStatement of Financial Position 2Daphne Gesto SiaresNo ratings yet

- Valuation of Mineral Resources in Selected FinanciDocument12 pagesValuation of Mineral Resources in Selected FinanciBill LiNo ratings yet