You might also like

- Private Retirement Plans in The PhilippinesDocument55 pagesPrivate Retirement Plans in The Philippineschane15100% (2)

- Sept Briefing National Institute For Retirement SecurityDocument37 pagesSept Briefing National Institute For Retirement Securitypcapineri8399No ratings yet

- Salient Features of The Employees Provident Funds and Miscellaneous Provisions Act, 1952Document3 pagesSalient Features of The Employees Provident Funds and Miscellaneous Provisions Act, 1952Fency Jenus75% (4)

- SMChap 013Document49 pagesSMChap 013testbank100% (5)

- Foundations of Financial Markets and Institutions 4th Edition Fabozzi Solutions ManualDocument8 pagesFoundations of Financial Markets and Institutions 4th Edition Fabozzi Solutions Manualfinificcodille6d3h100% (23)

- Provident Fund ActDocument14 pagesProvident Fund ActAkanksha Dubey0% (1)

- Chapter 25 (Pension Fund Operation)Document20 pagesChapter 25 (Pension Fund Operation)Aguntuk ShawonNo ratings yet

- Survey Research MethodDocument19 pagesSurvey Research Methodchhassan7No ratings yet

- Employee BenefitDocument32 pagesEmployee BenefitnatiNo ratings yet

- Employee BenefitsDocument27 pagesEmployee BenefitsS- Ajmeri100% (1)

- Session 18-19Document19 pagesSession 18-19Muhammad Ubaid UllahNo ratings yet

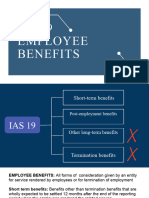

- Ias 19Document43 pagesIas 19Reever RiverNo ratings yet

- Chapter 14Document23 pagesChapter 14YolandaNo ratings yet

- Pension Chap 1 IntroductionDocument5 pagesPension Chap 1 IntroductionJoe KimNo ratings yet

- E.Types of Retirement Plans-1Document13 pagesE.Types of Retirement Plans-1Madhu dollyNo ratings yet

- April 7 - CH 20 Part IDocument21 pagesApril 7 - CH 20 Part IMichael NguyenNo ratings yet

- Asset Management-Pension FundsDocument9 pagesAsset Management-Pension FundsKen BiiNo ratings yet

- Monika Rehman Roll No 10Document19 pagesMonika Rehman Roll No 10Monika RehmanNo ratings yet

- IAS 19 - Employee BenefitDocument33 pagesIAS 19 - Employee BenefitlaaybaNo ratings yet

- Unit 03Document9 pagesUnit 03bobo tangaNo ratings yet

- MGFC20 Ch10 More InsurancesDocument5 pagesMGFC20 Ch10 More Insurancesbingus dingusNo ratings yet

- BF-Sources and Uses of Short-Term andDocument19 pagesBF-Sources and Uses of Short-Term andLarhAine Talisaysay - PongosNo ratings yet

- Chapter 18Document5 pagesChapter 18Le QuangNo ratings yet

- Summarizing Chapter 17 Herring Ton The Risk ManagementDocument4 pagesSummarizing Chapter 17 Herring Ton The Risk ManagementMd Shohag AliNo ratings yet

- Public and Private PensionDocument7 pagesPublic and Private PensionMelvyn LedesmaNo ratings yet

- Chapter 20Document21 pagesChapter 20Diana SantosNo ratings yet

- Employee Benefits: Retirement PlansDocument28 pagesEmployee Benefits: Retirement Plansbose3508No ratings yet

- Cliff Notes - PM RetirementDocument5 pagesCliff Notes - PM RetirementJohnathan JohnsonNo ratings yet

- Case Study Ch03Document3 pagesCase Study Ch03Munya Chawana0% (1)

- Executive Benefits: Recruit, Retain and Reward Your Top TalentDocument8 pagesExecutive Benefits: Recruit, Retain and Reward Your Top Talentalmirb7No ratings yet

- Edu 2013 10 Ret Plan Exam Case Kuk671xDocument20 pagesEdu 2013 10 Ret Plan Exam Case Kuk671xjusttestitNo ratings yet

- Chapter 08 FINDocument32 pagesChapter 08 FINUnoNo ratings yet

- 7-RETIREMENT AND PENSION PLANNING (Starting Early Retirement Planning)Document34 pages7-RETIREMENT AND PENSION PLANNING (Starting Early Retirement Planning)adib palidoNo ratings yet

- Employee Benefits Ias19Document42 pagesEmployee Benefits Ias19krishnaguptaNo ratings yet

- Cash Balance PlansDocument11 pagesCash Balance Plansmphillips36111No ratings yet

- Twelve Point Pension Reform PlanDocument4 pagesTwelve Point Pension Reform PlanGregory Flap ColeNo ratings yet

- Demas - Task 2Document7 pagesDemas - Task 2DemastaufiqNo ratings yet

- Ensions: DFA 2104 YDocument13 pagesEnsions: DFA 2104 YYoven VeerasamyNo ratings yet

- Defined Benefit Pension PlanDocument8 pagesDefined Benefit Pension Planhenok AbebeNo ratings yet

- Hbs Case Fund Management Group 7: Erika 410636061 Nokwanda 410636064 Franklin 410532065Document21 pagesHbs Case Fund Management Group 7: Erika 410636061 Nokwanda 410636064 Franklin 410532065Martina InaNo ratings yet

- Defined Benefit Pension Schemes: Questions and Answers: GuidanceDocument8 pagesDefined Benefit Pension Schemes: Questions and Answers: GuidanceSewale AbateNo ratings yet

- G8 Compensation and BenefitsDocument19 pagesG8 Compensation and BenefitsAngelu ReboiraNo ratings yet

- Group InsuranceDocument43 pagesGroup InsuranceSonia JainNo ratings yet

- HRM648 Chapter 13Document28 pagesHRM648 Chapter 132021485676No ratings yet

- Employee Benefits: Retirement PlansDocument28 pagesEmployee Benefits: Retirement PlansFaiza OmarNo ratings yet

- Q2 WordDocument22 pagesQ2 WordNishita DagaNo ratings yet

- Chapter 2 Lecture Notes.2021Document15 pagesChapter 2 Lecture Notes.2021Hoyin SinNo ratings yet

- Employee Benefit (Ias 19) FinalDocument36 pagesEmployee Benefit (Ias 19) FinalKanbiro OrkaidoNo ratings yet

- Group 10 (Pension Funds) .Document18 pagesGroup 10 (Pension Funds) .Odunukwe ChiamakaNo ratings yet

- Demographic Bases Investment Linked Insurance Plan Insurance Products Pensions & Annuities Risks and Solvency of InsuranceDocument24 pagesDemographic Bases Investment Linked Insurance Plan Insurance Products Pensions & Annuities Risks and Solvency of InsurancePraveen PanigrahiNo ratings yet

- Nondepository Financial InstitutionsDocument42 pagesNondepository Financial Institutionsdahlia oritNo ratings yet

- What Does Plan Sponsor Mean?Document7 pagesWhat Does Plan Sponsor Mean?moeed8393No ratings yet

- MGT 352 Chapter 11 SlidesDocument36 pagesMGT 352 Chapter 11 SlidesambermebakerNo ratings yet

- Unit 9 - Comp. - BenefitsDocument42 pagesUnit 9 - Comp. - BenefitsKeesha CharayaNo ratings yet

- Tax Chapter 13 14th EditionDocument47 pagesTax Chapter 13 14th Editiontrenn175% (4)

- Part 3 Pension FundsDocument4 pagesPart 3 Pension FundsAnNo ratings yet

- Ias 19 Employee BeneftDocument24 pagesIas 19 Employee Beneftesulawyer2001No ratings yet

- Maximizing Your Wealth: A Comprehensive Guide to Understanding Gross and Net SalaryFrom EverandMaximizing Your Wealth: A Comprehensive Guide to Understanding Gross and Net SalaryNo ratings yet

- CH 3 PosioningDocument24 pagesCH 3 Posioningchhassan7No ratings yet

- Ob13 13Document25 pagesOb13 13chhassan7No ratings yet

- The Mortgage Market: Presented By: Brady Anderson Chad Atkinson Charles Jones Mcleod Robinson Laura RogersDocument31 pagesThe Mortgage Market: Presented By: Brady Anderson Chad Atkinson Charles Jones Mcleod Robinson Laura Rogerschhassan7No ratings yet

- Pension FundsDocument26 pagesPension Fundschhassan7No ratings yet

- Stock Markets Around The WorldDocument15 pagesStock Markets Around The Worldchhassan7No ratings yet

- Depository Institutions: Activities and CharacteristicsDocument15 pagesDepository Institutions: Activities and Characteristicschhassan7No ratings yet

- Organizational Behavior: Robbins & JudgeDocument20 pagesOrganizational Behavior: Robbins & JudgedjlakshNo ratings yet

- Ob13 05Document21 pagesOb13 05Shreyansh RavalNo ratings yet

- Chapter 1: What Is Organizational Behavior?Document27 pagesChapter 1: What Is Organizational Behavior?chhassan7No ratings yet

- Operational DefinitionDocument9 pagesOperational Definitionchhassan7No ratings yet

- CH 3 The Communicator (Objectives and Credibility)Document12 pagesCH 3 The Communicator (Objectives and Credibility)chhassan7No ratings yet

- CH 1 Introduction To CommunicationDocument12 pagesCH 1 Introduction To Communicationchhassan7No ratings yet