You might also like

- IFM8e ch07Document20 pagesIFM8e ch07adnanNo ratings yet

- If Jeff Medora CHP 07Document25 pagesIf Jeff Medora CHP 07Naoman ChNo ratings yet

- Fixed Income Securities: A Beginner's Guide to Understand, Invest and Evaluate Fixed Income Securities: Investment series, #2From EverandFixed Income Securities: A Beginner's Guide to Understand, Invest and Evaluate Fixed Income Securities: Investment series, #2No ratings yet

- International ArbitrageDocument27 pagesInternational ArbitragehasnainNo ratings yet

- Fin 444 - Chapter 7 SlidesDocument28 pagesFin 444 - Chapter 7 SlidesBappi MahiNo ratings yet

- CH 7Document25 pagesCH 7Zuhaib SultanNo ratings yet

- Topic - IRPDocument25 pagesTopic - IRPAditya RajNo ratings yet

- Summary MKI Chapter 7Document5 pagesSummary MKI Chapter 7DeviNo ratings yet

- International Arbitrage: International Financial Management (FIN 263) Dr. Abdul Haseeb Spring-2021Document15 pagesInternational Arbitrage: International Financial Management (FIN 263) Dr. Abdul Haseeb Spring-2021Furqan AhmedNo ratings yet

- International Financial Management 8Document31 pagesInternational Financial Management 8胡依然No ratings yet

- International Arbitrage and Interest Rate ParityDocument19 pagesInternational Arbitrage and Interest Rate ParitysajjadNo ratings yet

- L4 International Arbitrage and IRPDocument25 pagesL4 International Arbitrage and IRPKent ChinNo ratings yet

- CH 07 - International Arbitrage and IRPDocument31 pagesCH 07 - International Arbitrage and IRPRim RimNo ratings yet

- 70-398 International Finance SPRING 2023: Prof. Serkan AkgucDocument29 pages70-398 International Finance SPRING 2023: Prof. Serkan AkgucAmiko GogitidzeNo ratings yet

- Currency Exchange Rates: Determination and Forecasting: Presenter's Name Presenter's Title DD Month YyyyDocument39 pagesCurrency Exchange Rates: Determination and Forecasting: Presenter's Name Presenter's Title DD Month YyyybingoNo ratings yet

- Chapter Review International Arbitrage and Interest Rate Parity International ArbitrageDocument9 pagesChapter Review International Arbitrage and Interest Rate Parity International ArbitrageWi SilalahiNo ratings yet

- 3.1 International Parity ConditionsDocument41 pages3.1 International Parity ConditionsSanaFatimaNo ratings yet

- Managing Transaction ExposureDocument30 pagesManaging Transaction ExposureImtiaz MasroorNo ratings yet

- Lecture 4Document64 pagesLecture 4James1331No ratings yet

- Interest Rate Parity PresentationDocument31 pagesInterest Rate Parity Presentationviki12334No ratings yet

- Chapter+4 +time+value+of+moneyDocument109 pagesChapter+4 +time+value+of+moneyThảo Nhi LêNo ratings yet

- Chapter 2 - Security ValuationDocument65 pagesChapter 2 - Security ValuationTín TrungNo ratings yet

- Ch5 Interest RatesDocument25 pagesCh5 Interest Rateszey9991No ratings yet

- Departure From PPPDocument27 pagesDeparture From PPPBhuvan AwasthiNo ratings yet

- Chapter 2 Part 2 IFMDocument15 pagesChapter 2 Part 2 IFMVaibhav PandeyNo ratings yet

- Financial Management: by K Lubza NiharDocument21 pagesFinancial Management: by K Lubza NiharAashutosh MishraNo ratings yet

- Corporate Valuation Session 4: Shobhit Aggarwal 11 July 2021 IIM UdaipurDocument31 pagesCorporate Valuation Session 4: Shobhit Aggarwal 11 July 2021 IIM UdaipurRohan LunawatNo ratings yet

- 5.2 Interest Rate ParityDocument30 pages5.2 Interest Rate ParityRammohanreddy RajidiNo ratings yet

- Madura14e Ch07 FinalDocument33 pagesMadura14e Ch07 FinalfabianngxinlongNo ratings yet

- Lecture07 Operating StudentDocument20 pagesLecture07 Operating StudentMit DaveNo ratings yet

- Bonds Valuation (Part Two)Document16 pagesBonds Valuation (Part Two)rrrrokayaaashrafNo ratings yet

- FIN430 ch.5Document18 pagesFIN430 ch.5Danial TorabianNo ratings yet

- Statistical Measures For RiskDocument17 pagesStatistical Measures For RiskShyamal75% (4)

- International Arbitrage and Interest Rate ParityDocument16 pagesInternational Arbitrage and Interest Rate ParityBaek AerinNo ratings yet

- International Parity RelationshipsDocument45 pagesInternational Parity RelationshipsDr RizwanaNo ratings yet

- International Arbitrage and Interest Rate Parity: From International Finance by Jeff MaduraDocument49 pagesInternational Arbitrage and Interest Rate Parity: From International Finance by Jeff Maduraabdullah.zhayatNo ratings yet

- Madura14e Ch07 FinalDocument33 pagesMadura14e Ch07 FinalVũ Trần Nhật ViNo ratings yet

- Transaction Exposure: Management: South-Western/Thomson Learning © 2006Document30 pagesTransaction Exposure: Management: South-Western/Thomson Learning © 2006Adi PhasaNo ratings yet

- The Valuation of Bonds PPT at Bec Doms FinanceDocument37 pagesThe Valuation of Bonds PPT at Bec Doms FinanceBabasab Patil (Karrisatte)No ratings yet

- If PPTSDocument31 pagesIf PPTSPriti BidasariaNo ratings yet

- International Parity Relationships and Forecasting Foreign Exchange RatesDocument30 pagesInternational Parity Relationships and Forecasting Foreign Exchange RatesiMQSxNo ratings yet

- Security Valuation: Bond, Equity and Preferred StockDocument40 pagesSecurity Valuation: Bond, Equity and Preferred StockMohamed KoneNo ratings yet

- SwapsDocument19 pagesSwapsUtsav ThakkarNo ratings yet

- Lecture04 Derivatives StudentDocument22 pagesLecture04 Derivatives StudentMit DaveNo ratings yet

- Lecture 6 - Interest Rates and Bond ValuationDocument61 pagesLecture 6 - Interest Rates and Bond ValuationDaniel HakimNo ratings yet

- International Financial ManagementDocument15 pagesInternational Financial ManagementraviNo ratings yet

- Session 4: An Overview of Innovative Financial Instruments and Their Implications For Tax Policy Sample Financial Instrument TransactionsDocument19 pagesSession 4: An Overview of Innovative Financial Instruments and Their Implications For Tax Policy Sample Financial Instrument TransactionsDP DileepkumarNo ratings yet

- Chapter 11 Bond ValuationDocument24 pagesChapter 11 Bond Valuationfiq8809No ratings yet

- Lecture Interest Rate ParityDocument10 pagesLecture Interest Rate ParityomeedjanNo ratings yet

- Valuation and Rates of Return: Mcgraw-Hill/IrwinDocument11 pagesValuation and Rates of Return: Mcgraw-Hill/IrwinAhmed ShantoNo ratings yet

- IFM 04 Parity RelationshipsDocument24 pagesIFM 04 Parity RelationshipsTanu GuptaNo ratings yet

- CHAPTER 3.1 - INTEREST RATE - Understanding Interest RateDocument39 pagesCHAPTER 3.1 - INTEREST RATE - Understanding Interest Ratek60.2112340086No ratings yet

- Time Value of MoneyDocument60 pagesTime Value of MoneyZain AbbasNo ratings yet

- CHP 6Document49 pagesCHP 6Khaled A. M. El-sherifNo ratings yet

- FINS3630: UNSW Business SchoolDocument32 pagesFINS3630: UNSW Business SchoolcarolinetsangNo ratings yet

- Eun 9e International Financial Management PPT CH06 AccessibleDocument31 pagesEun 9e International Financial Management PPT CH06 AccessibleDao Dang Khoa FUG CTNo ratings yet

- M06 Gitman50803X 14 MF C06Document16 pagesM06 Gitman50803X 14 MF C06Levan TsipianiNo ratings yet

- Key Features of Bonds Bond Valuation Measuring Yield Assessing RiskDocument28 pagesKey Features of Bonds Bond Valuation Measuring Yield Assessing RiskShuja GhayasNo ratings yet

- The Time Management Matrix: Manage FocusDocument1 pageThe Time Management Matrix: Manage FocusFarhanAwaisiNo ratings yet

- Current Affairs February 1st Week 2021Document27 pagesCurrent Affairs February 1st Week 2021FarhanAwaisiNo ratings yet

- 1000 MCQs One Paper Book (Everydays Science) by TestPoint - PKDocument65 pages1000 MCQs One Paper Book (Everydays Science) by TestPoint - PKFarhanAwaisi100% (2)

- Constitution 1973 MCQsDocument29 pagesConstitution 1973 MCQsFarhanAwaisiNo ratings yet

- Tehsil Markaz U.C Segment Name: BarleyDocument55 pagesTehsil Markaz U.C Segment Name: BarleyFarhanAwaisiNo ratings yet

- Lecturer Seats Subject Wise Break Up 2021Document10 pagesLecturer Seats Subject Wise Break Up 2021FarhanAwaisiNo ratings yet

- Steven Covey Time QuadrntsDocument3 pagesSteven Covey Time QuadrntsnetwrkengeerNo ratings yet

- Punjab Public Service Commission, Lahore: NoticeDocument3 pagesPunjab Public Service Commission, Lahore: NoticeFarhanAwaisiNo ratings yet

- 1000 MCQs One Paper Book (Everydays Science) by TestPoint - PKDocument65 pages1000 MCQs One Paper Book (Everydays Science) by TestPoint - PKFarhanAwaisi100% (2)

- CamScanner 11-12-2020 10.18.47Document20 pagesCamScanner 11-12-2020 10.18.47FarhanAwaisiNo ratings yet

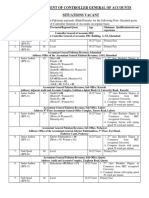

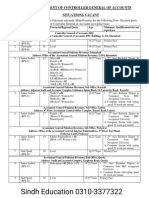

- Controller General of Accounts: As Per AdvertisementDocument2 pagesController General of Accounts: As Per AdvertisementDarshan KhatriNo ratings yet

- Paper 1Document5 pagesPaper 1FarhanAwaisiNo ratings yet

- CamScanner 11-26-2020 09.36Document16 pagesCamScanner 11-26-2020 09.36FarhanAwaisiNo ratings yet

- CamScanner 11-19-2020 12.22.52Document4 pagesCamScanner 11-19-2020 12.22.52FarhanAwaisiNo ratings yet

- Monetary Fiscal PolicyDocument2 pagesMonetary Fiscal PolicyFarhanAwaisiNo ratings yet

- Advt No.34-2020 13-11-2020 X7 VersionDocument1 pageAdvt No.34-2020 13-11-2020 X7 VersionSheikh JunaidNo ratings yet

- 2018-19 TomatoDocument1 page2018-19 TomatoShafiqueNo ratings yet

- Punjab Public Service CommissionDocument2 pagesPunjab Public Service CommissionFarhanAwaisiNo ratings yet

- Commission,: Punjab Public ServiceDocument1 pageCommission,: Punjab Public ServiceFarhanAwaisiNo ratings yet

- Department of Controller General of Accounts Situations VacantDocument4 pagesDepartment of Controller General of Accounts Situations VacantDarshan KhatriNo ratings yet

- Junior Clerk Accountant PaperDocument4 pagesJunior Clerk Accountant PaperFarhanAwaisiNo ratings yet

- 22M2019Document12 pages22M2019FarhanAwaisiNo ratings yet

- 650+ Jobs Federal GovtDocument4 pages650+ Jobs Federal GovtFarhanAwaisiNo ratings yet

- Advertisement No 31 2019Document2 pagesAdvertisement No 31 2019usama maqsoodNo ratings yet

- InterviewDocument9 pagesInterviewFarhanAwaisiNo ratings yet

- Most Important Current Affairs MCQs About All Provincial and National AssemblyDocument5 pagesMost Important Current Affairs MCQs About All Provincial and National AssemblyFarhanAwaisiNo ratings yet

- R&DDocument25 pagesR&Dmotty123456No ratings yet

- 326 1018 1 PBDocument6 pages326 1018 1 PBWajahat GhafoorNo ratings yet

- Effective Interview Techniques For Hiring Internal AuditorsDocument21 pagesEffective Interview Techniques For Hiring Internal AuditorsstudydatadownloadNo ratings yet

- PovertyReduction 13 Oct 05Document7 pagesPovertyReduction 13 Oct 05FarhanAwaisiNo ratings yet

- Micro Takaful Vs MicroinsuranceDocument5 pagesMicro Takaful Vs MicroinsuranceSiful Islam AnikNo ratings yet

- Aviva Hy2019 Analyst PackDocument112 pagesAviva Hy2019 Analyst PackGioan DuyNo ratings yet

- Pivot FormulaDocument1 pagePivot Formulaviral1622100% (1)

- FR M1 - Module Quiz 1 (Part 1) - KnowledgEquityDocument11 pagesFR M1 - Module Quiz 1 (Part 1) - KnowledgEquityThế Dân NguyễnNo ratings yet

- ACBP5122wA1 PDFDocument9 pagesACBP5122wA1 PDFAmmarah Ramnarain0% (1)

- 2.0 Price Action Chart Patterns (Eng & Hindi) VersionDocument81 pages2.0 Price Action Chart Patterns (Eng & Hindi) VersionSuman Saha25% (8)

- Reserve Bank of IndiaDocument40 pagesReserve Bank of IndiahakecNo ratings yet

- Accounting For Installment SalesDocument16 pagesAccounting For Installment SalesLeimonadeNo ratings yet

- Chief Sustainability Officers at Work (Excerpt)Document15 pagesChief Sustainability Officers at Work (Excerpt)arunah subramaniamNo ratings yet

- 04 - Chapter 2Document33 pages04 - Chapter 2baby0310No ratings yet

- DILG Resources 2011216 85e96b8954Document402 pagesDILG Resources 2011216 85e96b8954jennifertong82No ratings yet

- Himatsingka Seida LTD.: Ratio Analysis SheetDocument1 pageHimatsingka Seida LTD.: Ratio Analysis SheetNeetesh DohareNo ratings yet

- Cece and SusanDocument28 pagesCece and SusanCece J MarieNo ratings yet

- Eiot Year First Semester Qualifying Exam: Kingfisher School of Business and Finance Curriculum of AccountancyDocument4 pagesEiot Year First Semester Qualifying Exam: Kingfisher School of Business and Finance Curriculum of AccountancyGeorizz Kristine EscañoNo ratings yet

- Abm 3 Exam ReviewerDocument7 pagesAbm 3 Exam Reviewerjoshua korylle mahinayNo ratings yet

- Chapter 20 - Teacher's Manual - Far Part 1BDocument8 pagesChapter 20 - Teacher's Manual - Far Part 1BPacifico HernandezNo ratings yet

- IFM Assignment On International Business Finance 2009Document10 pagesIFM Assignment On International Business Finance 2009Melese ewnetie89% (9)

- Invoice TemplateDocument4 pagesInvoice TemplateObulesu NanganuruNo ratings yet

- Busn Introduction To Business Canadian 3rd Edition Kelly Test BankDocument33 pagesBusn Introduction To Business Canadian 3rd Edition Kelly Test Bankthomasriddledisrgzembc100% (28)

- AralPan9 q3 Mod16-17 PatakarangPananalapi v5-1Document23 pagesAralPan9 q3 Mod16-17 PatakarangPananalapi v5-1Ronald Montecillo AresNo ratings yet

- FileDocument11 pagesFileRiza GallardoNo ratings yet

- My Subscriptions Courses ACC410-Advanced Accounting Chapter 2 HomeworkDocument29 pagesMy Subscriptions Courses ACC410-Advanced Accounting Chapter 2 Homeworksuruth242No ratings yet

- 무역영어1급 (2020년 2회 A형)Document11 pages무역영어1급 (2020년 2회 A형)Rina DrozdNo ratings yet

- Negative and Positive Effects of Foreign Direct InvestmentDocument11 pagesNegative and Positive Effects of Foreign Direct InvestmentHarsha PremNo ratings yet

- Tata MotorsDocument24 pagesTata MotorsApurvAdarshNo ratings yet

- Hfa 021313Document8 pagesHfa 021313afaceanNo ratings yet

- Exercise 7 To 9Document4 pagesExercise 7 To 9No NotreallyNo ratings yet

- 1 - Project Selection I - V22Document81 pages1 - Project Selection I - V22Chiara Del PizzoNo ratings yet

- Unit 22: Government and Taxation (Handout)Document7 pagesUnit 22: Government and Taxation (Handout)Hannah KhuongNo ratings yet

- Growrich PinoyDocument59 pagesGrowrich PinoyMarites FerolinoNo ratings yet