You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5814)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

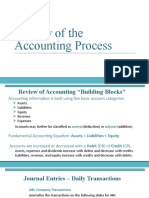

- Review of The Accounting ProcessDocument17 pagesReview of The Accounting ProcessLucy UnNo ratings yet

- Accounting Equation AssignmentDocument6 pagesAccounting Equation AssignmentDipika tasfannum salamNo ratings yet

- Ans Mini Case 2 - A171 - LecturerDocument14 pagesAns Mini Case 2 - A171 - LecturerXue Yin Lew100% (1)

- Test Bank ACC101-300cauDocument91 pagesTest Bank ACC101-300cauNguyễn Thanh HươngNo ratings yet

- Bajaj Consumer Care Limited: Detailed ReportDocument15 pagesBajaj Consumer Care Limited: Detailed Reportb0gm3n0tNo ratings yet

- Chapter+2 3Document14 pagesChapter+2 3kanasanNo ratings yet

- Module 6: What You Will LearnDocument30 pagesModule 6: What You Will Learn刘宝英No ratings yet

- Dokumen - Tips - Accounting Auditing Board of Ethiopia Aabe A Ipsas Are Being DevelopedDocument34 pagesDokumen - Tips - Accounting Auditing Board of Ethiopia Aabe A Ipsas Are Being DevelopedOUSMAN SEIDNo ratings yet

- Course Topics and Objectives: Topic Lesson Topic Subtopics ObjectivesDocument15 pagesCourse Topics and Objectives: Topic Lesson Topic Subtopics Objectivessiewsuan82No ratings yet

- ACC 101 - Module 4Document12 pagesACC 101 - Module 4Kyla Renz de LeonNo ratings yet

- IFRS Framework-Based Case Study - Barrick Gold Corporation-Goodwill For GoldDocument17 pagesIFRS Framework-Based Case Study - Barrick Gold Corporation-Goodwill For GoldJulio Marcos GansoNo ratings yet

- QUIZZES Soln Ap 2015Document51 pagesQUIZZES Soln Ap 2015Din Rose Gonzales100% (1)

- CH 03 Alt ProbDocument8 pagesCH 03 Alt ProbMuhammad Usman25% (4)

- NXU ACC6050 AssignmentDocument4 pagesNXU ACC6050 AssignmentFavourNo ratings yet

- Direct Non ControllingDocument24 pagesDirect Non ControllingJamie ZhangNo ratings yet

- Ajc - Fabm 10.5Document4 pagesAjc - Fabm 10.5Ashley Jean CosmianoNo ratings yet

- Pro Forma Balance Sheet Template: Company NameDocument5 pagesPro Forma Balance Sheet Template: Company NamePhương ĐinhNo ratings yet

- Accounts CIA 3 FinalDocument6 pagesAccounts CIA 3 FinalTanmay AroraNo ratings yet

- FORM 20K) For Other Countries: Annual Report Is Not A Substitute For This. SemiannuallyDocument2 pagesFORM 20K) For Other Countries: Annual Report Is Not A Substitute For This. SemiannuallyNeeraj SharmaNo ratings yet

- CH 02Document56 pagesCH 02AL SeneedaNo ratings yet

- 1000 2000 Corp Action 20220510Document82 pages1000 2000 Corp Action 20220510Contra Value BetsNo ratings yet

- Estados Financieros Mercadona ... NavarroDocument19 pagesEstados Financieros Mercadona ... NavarroRichard NavarroNo ratings yet

- Consolidated Technique Procedure4Document45 pagesConsolidated Technique Procedure4imamNo ratings yet

- MFRS 5Document22 pagesMFRS 5mzsanjay8131No ratings yet

- FABM1 Q4 Module 1Document23 pagesFABM1 Q4 Module 1Earl Christian BonaobraNo ratings yet

- Financial Statements, Taxes, and Cash Flow: Lecturer Dr. Le Thanh HuyenDocument47 pagesFinancial Statements, Taxes, and Cash Flow: Lecturer Dr. Le Thanh HuyenLê naNo ratings yet

- Introduction To Accounting JGF - July 31 and Aug 1Document26 pagesIntroduction To Accounting JGF - July 31 and Aug 1LARINGO IanNo ratings yet

- Camposol Real Food For Life: CAMPOSOL Holding LTD Fourth Quarter and Preliminary Full Year 2016 ReportDocument24 pagesCamposol Real Food For Life: CAMPOSOL Holding LTD Fourth Quarter and Preliminary Full Year 2016 ReportAlbert PizarroNo ratings yet

- Financial Statement AnalysisDocument8 pagesFinancial Statement AnalysiszhangxuNo ratings yet

- Soal Tugas Akm Is - ST o FP - CFDocument6 pagesSoal Tugas Akm Is - ST o FP - CFElyssa Fiqri Fauziah0% (1)