You might also like

- Treasury Overview Sesssion 1Document30 pagesTreasury Overview Sesssion 1ravitmadanNo ratings yet

- International Parity ConditionsDocument62 pagesInternational Parity ConditionsHaimanot tessemaNo ratings yet

- IFM Notes 1Document90 pagesIFM Notes 1Tarini MohantyNo ratings yet

- Lecture04 Derivatives StudentDocument22 pagesLecture04 Derivatives StudentMit DaveNo ratings yet

- Exchange RatesDocument34 pagesExchange RatesthebfilesNo ratings yet

- Lecture03 Parity StudentDocument23 pagesLecture03 Parity StudentMit DaveNo ratings yet

- Lecture 6 Currency Derivatives (1) : - The End of This Session Students Should Be Able ToDocument24 pagesLecture 6 Currency Derivatives (1) : - The End of This Session Students Should Be Able ToSaurabh MalikNo ratings yet

- Exchange RateDocument32 pagesExchange RateCharlene Ann EbiteNo ratings yet

- Management of Transaction ExposureDocument53 pagesManagement of Transaction ExposureParminder SalujaNo ratings yet

- Money and Banking 2009 SpringDocument117 pagesMoney and Banking 2009 SpringborchaliNo ratings yet

- Unit - Iii: Foreign Exchange Determination Systems &international InstitutionsDocument97 pagesUnit - Iii: Foreign Exchange Determination Systems &international InstitutionsShaziyaNo ratings yet

- Exchange Rate Determination and PolicyDocument33 pagesExchange Rate Determination and PolicyJunius Markov OlivierNo ratings yet

- Fixed Rates Macro PolicyDocument10 pagesFixed Rates Macro PolicyJelenaJovanovicNo ratings yet

- Short-Term Asset and Liability ManagementDocument36 pagesShort-Term Asset and Liability ManagementTanvir SazzadNo ratings yet

- International Parity Relationships & Forecasting Exchange RatesDocument33 pagesInternational Parity Relationships & Forecasting Exchange RatesKARISHMAATA2No ratings yet

- FRM Lecture 4 2020 2021 HandoutDocument41 pagesFRM Lecture 4 2020 2021 HandoutDaanNo ratings yet

- Macroeconomics ConsolidatedDocument118 pagesMacroeconomics ConsolidatedViral SavlaNo ratings yet

- Forward and Futures PricingDocument13 pagesForward and Futures PricingMandar Priya PhatakNo ratings yet

- L2 Exchange Rate DeterminationDocument25 pagesL2 Exchange Rate DeterminationKent ChinNo ratings yet

- International Monetary FundDocument19 pagesInternational Monetary FundSunni ZaraNo ratings yet

- EMEA Group2 EgyptDocument11 pagesEMEA Group2 EgyptRAJARSHI ROY CHOUDHURYNo ratings yet

- FRM Lecture 9 2020 2021 HandoutDocument39 pagesFRM Lecture 9 2020 2021 HandoutDaanNo ratings yet

- Interest Rate DeteminationnDocument13 pagesInterest Rate DeteminationnkafiNo ratings yet

- DBA 5035 - Financial Derivatives ManagementDocument277 pagesDBA 5035 - Financial Derivatives ManagementShrividhyaNo ratings yet

- Topic 4: Macroeconomic Objectives: EconomicsDocument19 pagesTopic 4: Macroeconomic Objectives: EconomicsAlvin Chai Win LockNo ratings yet

- MBA 3 Sem Finance Notes (Bangalore University)Document331 pagesMBA 3 Sem Finance Notes (Bangalore University)Pramod AiyappaNo ratings yet

- Inflation Persistence and The Taylor Rule: Christian Murray, David Papell, and Oleksandr RzhevskyyDocument18 pagesInflation Persistence and The Taylor Rule: Christian Murray, David Papell, and Oleksandr RzhevskyybilalalishahNo ratings yet

- Financial Markets: Lectures 3 - 4Document48 pagesFinancial Markets: Lectures 3 - 4Lê Mai Huyền LinhNo ratings yet

- Risk Management and Basel II: Bank Alfalah LimitedDocument72 pagesRisk Management and Basel II: Bank Alfalah LimitedMuhammad ArslanNo ratings yet

- MMS Derivatives Lec 4Document64 pagesMMS Derivatives Lec 4AzharNo ratings yet

- FRM Lecture 11 2020 2021 HandoutDocument31 pagesFRM Lecture 11 2020 2021 HandoutDaanNo ratings yet

- 12 FinancialInstrumentsandTheirRelevanceDocument39 pages12 FinancialInstrumentsandTheirRelevanceRizki Fazlur RachmanNo ratings yet

- Financial Risk Management: Martien Lamers // 7-12-2020Document93 pagesFinancial Risk Management: Martien Lamers // 7-12-2020DaanNo ratings yet

- DerivativesDocument21 pagesDerivativesMandar Priya PhatakNo ratings yet

- Swapclear: LCH - Clearnet LTD European Central Bank 9Th July 2009Document9 pagesSwapclear: LCH - Clearnet LTD European Central Bank 9Th July 2009Aleis RiquelmeNo ratings yet

- Currency BasicsDocument18 pagesCurrency BasicsChandan AgarwalNo ratings yet

- Econometric Methods: Theory Mathematics StatisticsDocument22 pagesEconometric Methods: Theory Mathematics StatisticsGiri PrasadNo ratings yet

- Chapter+2.+Financial+markets-đã GộpDocument232 pagesChapter+2.+Financial+markets-đã GộpThảo Nhi LêNo ratings yet

- 1.4 Market FailureDocument42 pages1.4 Market FailureRuban PaulNo ratings yet

- "Introduction To International Financial System": "International Finance and Payments"Document425 pages"Introduction To International Financial System": "International Finance and Payments"Ioan 23No ratings yet

- Salvatore Chapter 08Document27 pagesSalvatore Chapter 08Umair NizamiNo ratings yet

- International Business NotesDocument118 pagesInternational Business NotesJason CaiNo ratings yet

- By: Domodar N. Gujarati: Prof. M. El-SakkaDocument19 pagesBy: Domodar N. Gujarati: Prof. M. El-SakkarohanpjadhavNo ratings yet

- Quick Overview of The FX MarketDocument24 pagesQuick Overview of The FX MarketpatrocompsNo ratings yet

- Nontariff Trade Barriers: Powerpoint Slides Prepared By: Andreea Chiritescu Eastern Illinois UniversityDocument33 pagesNontariff Trade Barriers: Powerpoint Slides Prepared By: Andreea Chiritescu Eastern Illinois UniversityHengyi LimNo ratings yet

- Financial Markets and Institutions: Abridged 10 EditionDocument32 pagesFinancial Markets and Institutions: Abridged 10 EditionrynajaeNo ratings yet

- Business Climate in EgyptDocument24 pagesBusiness Climate in EgyptStefan AlexandruNo ratings yet

- Introduction To Financial EconometricsDocument38 pagesIntroduction To Financial EconometricsMohd ZahidNo ratings yet

- Egypt StrategyDocument32 pagesEgypt Strategymohamed hamdiNo ratings yet

- ch03 ptg01Document9 pagesch03 ptg01Tran Kim NganNo ratings yet

- Chapter 1Document26 pagesChapter 1Hamid UllahNo ratings yet

- Transaction Exposure Chapter 11Document57 pagesTransaction Exposure Chapter 11armando.chappell1005No ratings yet

- Determining Exchange RatesDocument35 pagesDetermining Exchange Ratesayush_singhal27No ratings yet

- Money Market Black SwanDocument29 pagesMoney Market Black SwanZerohedgeNo ratings yet

- Parity Conditions in International Finance and Currency ForecastingDocument31 pagesParity Conditions in International Finance and Currency ForecastingMahima AgrawalNo ratings yet

- Chapter 3 International Financial MarketsDocument93 pagesChapter 3 International Financial Marketsธชพร พรหมสีดาNo ratings yet

- BOP TheoriesDocument33 pagesBOP TheoriesOlawale Oluwatoyin BolajiNo ratings yet

- Chapter 1 National Income Accounting and BOPDocument44 pagesChapter 1 National Income Accounting and BOPnguyenphamngocmy01082003No ratings yet

- Chapter FourDocument22 pagesChapter Fourhaile girmaNo ratings yet

- Participatory Governance - ReportDocument12 pagesParticipatory Governance - ReportAslamKhayerNo ratings yet

- Bookmakers NightmareDocument50 pagesBookmakers NightmarefabihdroNo ratings yet

- TerraCycle Investment GuideDocument21 pagesTerraCycle Investment GuideMaria KennedyNo ratings yet

- In Re: Rnnkeepers Usa Trust. Debtors. - Chapter LL Case No. 10 13800 (SCC)Document126 pagesIn Re: Rnnkeepers Usa Trust. Debtors. - Chapter LL Case No. 10 13800 (SCC)Chapter 11 DocketsNo ratings yet

- Sim CBM 122 Lesson 3Document9 pagesSim CBM 122 Lesson 3Andrew Sy ScottNo ratings yet

- PNB v. AtendidoDocument2 pagesPNB v. AtendidoAntonio RebosaNo ratings yet

- Veit Tunel 1Document7 pagesVeit Tunel 1Bladimir SolizNo ratings yet

- Textile Conv Belt - 4410-155R-QVM-Q-002-01 PDFDocument10 pagesTextile Conv Belt - 4410-155R-QVM-Q-002-01 PDFCaspian DattaNo ratings yet

- IELTS Writing Task 1 Sample - Bar Chart - ZIMDocument28 pagesIELTS Writing Task 1 Sample - Bar Chart - ZIMPhương Thư Nguyễn HoàngNo ratings yet

- LiberalisationDocument6 pagesLiberalisationkadamabariNo ratings yet

- FOR Office USE Only: HDFC Life Sb/Ca/Cc/Sb-Nre/Sb-Nro/OtherDocument2 pagesFOR Office USE Only: HDFC Life Sb/Ca/Cc/Sb-Nre/Sb-Nro/OtherVIkashNo ratings yet

- 13 Chapter V (Swot Analysis and Compitetor Analysis)Document3 pages13 Chapter V (Swot Analysis and Compitetor Analysis)hari tejaNo ratings yet

- Effect of Vishal Mega Mart On Traditional RetailingDocument7 pagesEffect of Vishal Mega Mart On Traditional RetailingAnuradha KathaitNo ratings yet

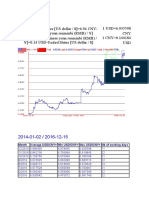

- Month Average USD/CNY Min USD/CNY Max USD/CNY NB of Working DaysDocument3 pagesMonth Average USD/CNY Min USD/CNY Max USD/CNY NB of Working DaysZahid RizvyNo ratings yet

- Rethinking Social Protection Paradigm-1Document22 pagesRethinking Social Protection Paradigm-1herryansharyNo ratings yet

- MKT 465 ch2 SehDocument51 pagesMKT 465 ch2 SehNaimul KaderNo ratings yet

- Full Download Business in Action 6th Edition Bovee Solutions ManualDocument35 pagesFull Download Business in Action 6th Edition Bovee Solutions Manuallincolnpatuc8100% (32)

- Draft LA Ghana Country Study, En-1Document35 pagesDraft LA Ghana Country Study, En-1agyenimboatNo ratings yet

- Fees and ChecklistDocument3 pagesFees and ChecklistAdenuga SantosNo ratings yet

- N 1415 Iso - CD - 3408-5 - (E) - 2003 - 08Document16 pagesN 1415 Iso - CD - 3408-5 - (E) - 2003 - 08brunoagandraNo ratings yet

- BS 2010-11 PDFDocument63 pagesBS 2010-11 PDFnarendra kumarNo ratings yet

- 3M Knowledge Management-Group 1Document22 pages3M Knowledge Management-Group 1Siddharth Sourav PadheeNo ratings yet

- 6 The Neoclassical Summary Free Trade As Economic GoalDocument4 pages6 The Neoclassical Summary Free Trade As Economic GoalOlga LiNo ratings yet

- Abstract, Attestation & AcknowledgementDocument6 pagesAbstract, Attestation & AcknowledgementDeedar.RaheemNo ratings yet

- Day Balance Daily % Growth Daily Profit Goal TP: Necessary Lot Size Based On One Trade Per Daynecessary Lot Size Based On One Trade Per DayDocument8 pagesDay Balance Daily % Growth Daily Profit Goal TP: Necessary Lot Size Based On One Trade Per Daynecessary Lot Size Based On One Trade Per DayVeeraesh MSNo ratings yet

- Team Energy Corporation, V. Cir G.R. No. 197770, March 14, 2018 Cir V. Covanta Energy Philippine Holdings, Inc., G.R. No. 203160, January 24, 2018Document5 pagesTeam Energy Corporation, V. Cir G.R. No. 197770, March 14, 2018 Cir V. Covanta Energy Philippine Holdings, Inc., G.R. No. 203160, January 24, 2018Raymarc Elizer AsuncionNo ratings yet

- 2022 06 15 LT Hyderabad Metro Rail Unveils Metro Bazar ShoppingonthegoDocument2 pages2022 06 15 LT Hyderabad Metro Rail Unveils Metro Bazar ShoppingonthegoKathir JeNo ratings yet

- A Renewable WorldDocument257 pagesA Renewable WorldMiguel MendoncaNo ratings yet

- 11th 12th Economics Q EM Sample PagesDocument27 pages11th 12th Economics Q EM Sample PagesKirthika RajaNo ratings yet

- Example of A Project CharterDocument9 pagesExample of A Project CharterHenry Sithole100% (1)