Aud689: Audit and Assurance Services Dec 2016 Question 1: Prepared For: Puan Khair Syakira

Aud689: Audit and Assurance Services Dec 2016 Question 1: Prepared For: Puan Khair Syakira

You might also like

- Fake IT - Fake The World - The Original Since 2011Document2 pagesFake IT - Fake The World - The Original Since 2011Tetsu Kun53% (15)

- Question Bank On Materials ManagementDocument12 pagesQuestion Bank On Materials ManagementMY NAME IS NEERAJ..:):)82% (55)

- Alia Syazwani Practical Training ReportDocument22 pagesAlia Syazwani Practical Training ReportAli Hisham GholamNo ratings yet

- Final Assessment S1, 2021Document5 pagesFinal Assessment S1, 2021Dilrukshi WanasingheNo ratings yet

- Tutorial 6 WIP - DIrector DutiesDocument2 pagesTutorial 6 WIP - DIrector DutiesGurrajvin SinghNo ratings yet

- Megan MediaDocument8 pagesMegan Mediarose0% (1)

- Fedai Objective Questions PDFDocument12 pagesFedai Objective Questions PDFpoonamgulati2000100% (5)

- BKAS3083 Topic1Document27 pagesBKAS3083 Topic1WEIWEICHONG93No ratings yet

- 3.0 Principles of Effective AccountabilityDocument10 pages3.0 Principles of Effective AccountabilityNor Ashqira KamarulNo ratings yet

- Lecture Tutorial - P, CL and CA (A)Document3 pagesLecture Tutorial - P, CL and CA (A)yym cindyy100% (1)

- Public Prosecutor V Mohamed Ezam Bin Mohd NoDocument14 pagesPublic Prosecutor V Mohamed Ezam Bin Mohd Nomykoda-10% (1)

- Answer Project FAR610Document15 pagesAnswer Project FAR610Syahrul Amirul100% (1)

- Bio Osmo - Announcement Dated 12 April 2018Document59 pagesBio Osmo - Announcement Dated 12 April 2018Ikhwan IlmiNo ratings yet

- Case 15 McDonalds QDocument5 pagesCase 15 McDonalds Qareep940% (1)

- Goldberg V JenkinsDocument3 pagesGoldberg V Jenkinsareep94No ratings yet

- Test Bank For Financial Reporting and Analysis 7th Edition by RevsineDocument34 pagesTest Bank For Financial Reporting and Analysis 7th Edition by Revsinea8634551530% (1)

- Fire Insurance ClaimsDocument17 pagesFire Insurance ClaimsRakshikaa V100% (1)

- Presentation AUD689 EDITED PDFDocument12 pagesPresentation AUD689 EDITED PDFZatyAriffinNo ratings yet

- MIA By-Laws (On Professional Ethics, Conduct and Practice)Document36 pagesMIA By-Laws (On Professional Ethics, Conduct and Practice)Nur IzzahNo ratings yet

- Maf651 Seminar 2 ReportDocument13 pagesMaf651 Seminar 2 Report2022908185No ratings yet

- HRM581 Compliance AnalysisDocument13 pagesHRM581 Compliance Analysis2021843868No ratings yet

- Universiti Teknologi Mara Test 2 Course: Corporate Finance Course Code: MAF603 Examination: 9 JANUARY 2021 Time: 1 Hour 15 MinutesDocument3 pagesUniversiti Teknologi Mara Test 2 Course: Corporate Finance Course Code: MAF603 Examination: 9 JANUARY 2021 Time: 1 Hour 15 MinutesPutri Naajihah 4GNo ratings yet

- Test Aud 689 - Apr 2018Document3 pagesTest Aud 689 - Apr 2018Nur Dina AbsbNo ratings yet

- Law485 c5 Officers of A CompanyDocument37 pagesLaw485 c5 Officers of A CompanyndhtzxNo ratings yet

- Tega Payment SystemDocument8 pagesTega Payment Systemzarfarie aron67% (3)

- Contoh - Fin-552-Group-Assignment-Bursa-Marketplace-Stock-Trading-GameDocument22 pagesContoh - Fin-552-Group-Assignment-Bursa-Marketplace-Stock-Trading-GameHuzairul Iqmar ShafiqNo ratings yet

- Aud 689 WWW Advanced AuditingDocument3 pagesAud 689 WWW Advanced AuditingNur SyafiqahNo ratings yet

- LAW485 Officers of The Company - AuditorDocument35 pagesLAW485 Officers of The Company - AuditorALIFP NAJMI SOFIANNo ratings yet

- PBL 2 Mac 2020Document4 pagesPBL 2 Mac 2020Ummu UmairahNo ratings yet

- Law Report Ques 41Document15 pagesLaw Report Ques 41Syahirah AliNo ratings yet

- Corporate Law - Law 485 Test 1 Business Entities, Formation & Separate Legal EntityDocument4 pagesCorporate Law - Law 485 Test 1 Business Entities, Formation & Separate Legal EntityewinzeNo ratings yet

- AP Cars SDN BHD - QuestionsDocument1 pageAP Cars SDN BHD - Questionsnadia0% (1)

- Solution Far450 - Jun 2014Document7 pagesSolution Far450 - Jun 2014Pablo EkskobaNo ratings yet

- Tutorial 1 3Document5 pagesTutorial 1 3Faiz MohamadNo ratings yet

- Question AIS AssignmentDocument4 pagesQuestion AIS Assignmentfaris ikhwanNo ratings yet

- Logbook Aisyah Athirah Abdul RazabDocument28 pagesLogbook Aisyah Athirah Abdul Razabauni fildzahNo ratings yet

- Quiz 2 QuestionDocument3 pagesQuiz 2 QuestionFatin NajihahNo ratings yet

- Test FAR 570 Feb 2021Document2 pagesTest FAR 570 Feb 2021Putri Naajihah 4GNo ratings yet

- Field Report Pac671 - Nur AzreenDocument16 pagesField Report Pac671 - Nur Azreen2021117961No ratings yet

- Ba2463d Assignment2Document36 pagesBa2463d Assignment2Aqilah PeiruzNo ratings yet

- Workshop 6 (Students) ADM657Document7 pagesWorkshop 6 (Students) ADM657Khairi N WanieNo ratings yet

- Group Assignment Opm554 ArticleDocument13 pagesGroup Assignment Opm554 ArticleAfiq Najmi RosmanNo ratings yet

- ACC 106 Chapter 1Document13 pagesACC 106 Chapter 1Firdaus Yahaya100% (4)

- Financial Derivative AssignmentDocument14 pagesFinancial Derivative AssignmentSriSaraswathyNo ratings yet

- Financial Derivatives InstrumentDocument18 pagesFinancial Derivatives InstrumentAfreen Redita100% (1)

- Fin430 - Dec2019Document6 pagesFin430 - Dec2019nurinsabyhahNo ratings yet

- Practical Report C2 Adm665 - Athirah 2021120107Document11 pagesPractical Report C2 Adm665 - Athirah 2021120107Liyana AzizNo ratings yet

- Mgt555 - Individual Assignment 2Document6 pagesMgt555 - Individual Assignment 22021230564No ratings yet

- Final Assessment - Suggested Solution & Marking Scheme Paper 1Document3 pagesFinal Assessment - Suggested Solution & Marking Scheme Paper 1Deidree Elsa100% (1)

- Androids Under AttackDocument7 pagesAndroids Under Attack42523317No ratings yet

- Role Play 20204 - Fin242Document2 pagesRole Play 20204 - Fin242Muhd Arreif Mohd AzzarainNo ratings yet

- Product Life CycleDocument5 pagesProduct Life CycleEkkala Naruttey0% (1)

- TAX Treatment For TAX267 and TAX317 Budget 2019Document5 pagesTAX Treatment For TAX267 and TAX317 Budget 2019nonameNo ratings yet

- Final Exam (Finalized) MaleDocument3 pagesFinal Exam (Finalized) Maleirfan sururiNo ratings yet

- Group Project 2 Far620Document8 pagesGroup Project 2 Far620NUR ATHIRAH SUKAIMINo ratings yet

- Read The Following Excerpt From A Complaint Filed by TheDocument1 pageRead The Following Excerpt From A Complaint Filed by TheLet's Talk With Hassan0% (1)

- Written Up AromaDocument3 pagesWritten Up AromaShikin YazidNo ratings yet

- Far660 - Group Project - October 2020Document2 pagesFar660 - Group Project - October 2020Nur ImanNo ratings yet

- AUD689 Tutorial Question Legal LiabilityDocument5 pagesAUD689 Tutorial Question Legal LiabilityJebatNo ratings yet

- Lotus KFM Berhad FADocument19 pagesLotus KFM Berhad FAGeorge BichangaNo ratings yet

- HRM648 Case Study Group AssignmentDocument9 pagesHRM648 Case Study Group Assignment2022753001No ratings yet

- Draft Ads530Document11 pagesDraft Ads530Izzianie HusinNo ratings yet

- Report Managerial Finance@UniklDocument18 pagesReport Managerial Finance@UniklLee WongNo ratings yet

- Datuk Yap Pak Leong v. Ketua Pengarah Hasil Dalam Negeri - BKI-14-1/2-2013Document7 pagesDatuk Yap Pak Leong v. Ketua Pengarah Hasil Dalam Negeri - BKI-14-1/2-2013Vasanth TamilselvanNo ratings yet

- Chapter 01 IntroductionDocument18 pagesChapter 01 IntroductionzamriNo ratings yet

- AUDITORDocument17 pagesAUDITORMalNo ratings yet

- Word FULLDocument7 pagesWord FULLfara_lianaNo ratings yet

- Current IssueDocument4 pagesCurrent Issueareep94No ratings yet

- Strategic Management (Maf661) : Submission DateDocument1 pageStrategic Management (Maf661) : Submission Dateareep94No ratings yet

- Hilton - Maher - SeltoDocument21 pagesHilton - Maher - Seltoareep94No ratings yet

- Chapter 3 MAF661Document26 pagesChapter 3 MAF661areep94No ratings yet

- Chapter 1Document48 pagesChapter 1areep94No ratings yet

- Chapter 3 MAF661Document26 pagesChapter 3 MAF661areep94No ratings yet

- KafalahDocument6 pagesKafalahareep94No ratings yet

- WadiahDocument11 pagesWadiahareep94100% (1)

- Law IndividualDocument5 pagesLaw Individualareep94No ratings yet

- Muhammad Nazri Bin Ramli Director of Group QualityDocument1 pageMuhammad Nazri Bin Ramli Director of Group Qualityareep94No ratings yet

- Head OfficeDocument1 pageHead Officeareep94No ratings yet

- InvoicouDocument16 pagesInvoicoustock18100% (1)

- Internship Report 2nd PartDocument89 pagesInternship Report 2nd PartAli Asgor RatonNo ratings yet

- Rekonsiliasi BankDocument3 pagesRekonsiliasi BankTata Intan TamaraNo ratings yet

- Suncoast Account Statement: Access Your Account: Sunnet Online Banking Sunmobile App Suntel Phone BankingDocument6 pagesSuncoast Account Statement: Access Your Account: Sunnet Online Banking Sunmobile App Suntel Phone BankingolaNo ratings yet

- Case Study On Letter of CreditDocument9 pagesCase Study On Letter of CreditPrahant KumarNo ratings yet

- Acct Statement - XX4767 - 24042023Document3 pagesAcct Statement - XX4767 - 24042023Tamil VaengaiNo ratings yet

- Tally Lab ManualDocument50 pagesTally Lab ManualDeepika Sharma100% (5)

- Muthoot Fincorp CalrificationsDocument6 pagesMuthoot Fincorp CalrificationslulughoshNo ratings yet

- Usage Guide - Rewards Plus PDFDocument8 pagesUsage Guide - Rewards Plus PDFHemant JainNo ratings yet

- Proof of Cash: By: LailaneDocument19 pagesProof of Cash: By: LailaneKyle BrianNo ratings yet

- PAT - Digest Compilation No. 6 (PARTNERSHIP)Document122 pagesPAT - Digest Compilation No. 6 (PARTNERSHIP)Jam PagsuyoinNo ratings yet

- Sanjeev CVDocument3 pagesSanjeev CVCYGNUSMLS ACCOUNTSNo ratings yet

- Support Package Terms and ConditionsDocument2 pagesSupport Package Terms and ConditionsArs OrpheusNo ratings yet

- The Cash Receipts JournalDocument3 pagesThe Cash Receipts JournalRandy AlbutraNo ratings yet

- Buss. Finance FinalDocument7 pagesBuss. Finance FinalAlvin Vin VinNo ratings yet

- INTACC1Document2 pagesINTACC1Ronalyn LajomNo ratings yet

- WeRPN Form FillableDocument2 pagesWeRPN Form FillablemiiszNo ratings yet

- Account Statement For Account:22112413000022: Branch DetailsDocument4 pagesAccount Statement For Account:22112413000022: Branch Detailsvishwak properties mangal avenueNo ratings yet

- Bank Liquidity Policy StatementDocument19 pagesBank Liquidity Policy StatementapluNo ratings yet

- 3 Woody v. National Bank of Rocky MountDocument2 pages3 Woody v. National Bank of Rocky MountrNo ratings yet

- Auditing The Expenditure CycleDocument4 pagesAuditing The Expenditure CycleIndri IswardhaniNo ratings yet

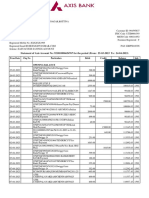

- Axis BankDocument20 pagesAxis BankXYZ909No ratings yet

- MC - Internal AuditDocument12 pagesMC - Internal AuditMegawati MediyaniNo ratings yet

- Import Form 2018Document6 pagesImport Form 2018tejasg82100% (2)

- Health Insurance Brochure - HDFC ERGO PREMIUMS PDFDocument4 pagesHealth Insurance Brochure - HDFC ERGO PREMIUMS PDFram_341No ratings yet

You might also like

- Fake IT - Fake The World - The Original Since 2011Document2 pagesFake IT - Fake The World - The Original Since 2011Tetsu Kun53% (15)

- Question Bank On Materials ManagementDocument12 pagesQuestion Bank On Materials ManagementMY NAME IS NEERAJ..:):)82% (55)

- Alia Syazwani Practical Training ReportDocument22 pagesAlia Syazwani Practical Training ReportAli Hisham GholamNo ratings yet

- Final Assessment S1, 2021Document5 pagesFinal Assessment S1, 2021Dilrukshi WanasingheNo ratings yet

- Tutorial 6 WIP - DIrector DutiesDocument2 pagesTutorial 6 WIP - DIrector DutiesGurrajvin SinghNo ratings yet

- Megan MediaDocument8 pagesMegan Mediarose0% (1)

- Fedai Objective Questions PDFDocument12 pagesFedai Objective Questions PDFpoonamgulati2000100% (5)

- BKAS3083 Topic1Document27 pagesBKAS3083 Topic1WEIWEICHONG93No ratings yet

- 3.0 Principles of Effective AccountabilityDocument10 pages3.0 Principles of Effective AccountabilityNor Ashqira KamarulNo ratings yet

- Lecture Tutorial - P, CL and CA (A)Document3 pagesLecture Tutorial - P, CL and CA (A)yym cindyy100% (1)

- Public Prosecutor V Mohamed Ezam Bin Mohd NoDocument14 pagesPublic Prosecutor V Mohamed Ezam Bin Mohd Nomykoda-10% (1)

- Answer Project FAR610Document15 pagesAnswer Project FAR610Syahrul Amirul100% (1)

- Bio Osmo - Announcement Dated 12 April 2018Document59 pagesBio Osmo - Announcement Dated 12 April 2018Ikhwan IlmiNo ratings yet

- Case 15 McDonalds QDocument5 pagesCase 15 McDonalds Qareep940% (1)

- Goldberg V JenkinsDocument3 pagesGoldberg V Jenkinsareep94No ratings yet

- Test Bank For Financial Reporting and Analysis 7th Edition by RevsineDocument34 pagesTest Bank For Financial Reporting and Analysis 7th Edition by Revsinea8634551530% (1)

- Fire Insurance ClaimsDocument17 pagesFire Insurance ClaimsRakshikaa V100% (1)

- Presentation AUD689 EDITED PDFDocument12 pagesPresentation AUD689 EDITED PDFZatyAriffinNo ratings yet

- MIA By-Laws (On Professional Ethics, Conduct and Practice)Document36 pagesMIA By-Laws (On Professional Ethics, Conduct and Practice)Nur IzzahNo ratings yet

- Maf651 Seminar 2 ReportDocument13 pagesMaf651 Seminar 2 Report2022908185No ratings yet

- HRM581 Compliance AnalysisDocument13 pagesHRM581 Compliance Analysis2021843868No ratings yet

- Universiti Teknologi Mara Test 2 Course: Corporate Finance Course Code: MAF603 Examination: 9 JANUARY 2021 Time: 1 Hour 15 MinutesDocument3 pagesUniversiti Teknologi Mara Test 2 Course: Corporate Finance Course Code: MAF603 Examination: 9 JANUARY 2021 Time: 1 Hour 15 MinutesPutri Naajihah 4GNo ratings yet

- Test Aud 689 - Apr 2018Document3 pagesTest Aud 689 - Apr 2018Nur Dina AbsbNo ratings yet

- Law485 c5 Officers of A CompanyDocument37 pagesLaw485 c5 Officers of A CompanyndhtzxNo ratings yet

- Tega Payment SystemDocument8 pagesTega Payment Systemzarfarie aron67% (3)

- Contoh - Fin-552-Group-Assignment-Bursa-Marketplace-Stock-Trading-GameDocument22 pagesContoh - Fin-552-Group-Assignment-Bursa-Marketplace-Stock-Trading-GameHuzairul Iqmar ShafiqNo ratings yet

- Aud 689 WWW Advanced AuditingDocument3 pagesAud 689 WWW Advanced AuditingNur SyafiqahNo ratings yet

- LAW485 Officers of The Company - AuditorDocument35 pagesLAW485 Officers of The Company - AuditorALIFP NAJMI SOFIANNo ratings yet

- PBL 2 Mac 2020Document4 pagesPBL 2 Mac 2020Ummu UmairahNo ratings yet

- Law Report Ques 41Document15 pagesLaw Report Ques 41Syahirah AliNo ratings yet

- Corporate Law - Law 485 Test 1 Business Entities, Formation & Separate Legal EntityDocument4 pagesCorporate Law - Law 485 Test 1 Business Entities, Formation & Separate Legal EntityewinzeNo ratings yet

- AP Cars SDN BHD - QuestionsDocument1 pageAP Cars SDN BHD - Questionsnadia0% (1)

- Solution Far450 - Jun 2014Document7 pagesSolution Far450 - Jun 2014Pablo EkskobaNo ratings yet

- Tutorial 1 3Document5 pagesTutorial 1 3Faiz MohamadNo ratings yet

- Question AIS AssignmentDocument4 pagesQuestion AIS Assignmentfaris ikhwanNo ratings yet

- Logbook Aisyah Athirah Abdul RazabDocument28 pagesLogbook Aisyah Athirah Abdul Razabauni fildzahNo ratings yet

- Quiz 2 QuestionDocument3 pagesQuiz 2 QuestionFatin NajihahNo ratings yet

- Test FAR 570 Feb 2021Document2 pagesTest FAR 570 Feb 2021Putri Naajihah 4GNo ratings yet

- Field Report Pac671 - Nur AzreenDocument16 pagesField Report Pac671 - Nur Azreen2021117961No ratings yet

- Ba2463d Assignment2Document36 pagesBa2463d Assignment2Aqilah PeiruzNo ratings yet

- Workshop 6 (Students) ADM657Document7 pagesWorkshop 6 (Students) ADM657Khairi N WanieNo ratings yet

- Group Assignment Opm554 ArticleDocument13 pagesGroup Assignment Opm554 ArticleAfiq Najmi RosmanNo ratings yet

- ACC 106 Chapter 1Document13 pagesACC 106 Chapter 1Firdaus Yahaya100% (4)

- Financial Derivative AssignmentDocument14 pagesFinancial Derivative AssignmentSriSaraswathyNo ratings yet

- Financial Derivatives InstrumentDocument18 pagesFinancial Derivatives InstrumentAfreen Redita100% (1)

- Fin430 - Dec2019Document6 pagesFin430 - Dec2019nurinsabyhahNo ratings yet

- Practical Report C2 Adm665 - Athirah 2021120107Document11 pagesPractical Report C2 Adm665 - Athirah 2021120107Liyana AzizNo ratings yet

- Mgt555 - Individual Assignment 2Document6 pagesMgt555 - Individual Assignment 22021230564No ratings yet

- Final Assessment - Suggested Solution & Marking Scheme Paper 1Document3 pagesFinal Assessment - Suggested Solution & Marking Scheme Paper 1Deidree Elsa100% (1)

- Androids Under AttackDocument7 pagesAndroids Under Attack42523317No ratings yet

- Role Play 20204 - Fin242Document2 pagesRole Play 20204 - Fin242Muhd Arreif Mohd AzzarainNo ratings yet

- Product Life CycleDocument5 pagesProduct Life CycleEkkala Naruttey0% (1)

- TAX Treatment For TAX267 and TAX317 Budget 2019Document5 pagesTAX Treatment For TAX267 and TAX317 Budget 2019nonameNo ratings yet

- Final Exam (Finalized) MaleDocument3 pagesFinal Exam (Finalized) Maleirfan sururiNo ratings yet

- Group Project 2 Far620Document8 pagesGroup Project 2 Far620NUR ATHIRAH SUKAIMINo ratings yet

- Read The Following Excerpt From A Complaint Filed by TheDocument1 pageRead The Following Excerpt From A Complaint Filed by TheLet's Talk With Hassan0% (1)

- Written Up AromaDocument3 pagesWritten Up AromaShikin YazidNo ratings yet

- Far660 - Group Project - October 2020Document2 pagesFar660 - Group Project - October 2020Nur ImanNo ratings yet

- AUD689 Tutorial Question Legal LiabilityDocument5 pagesAUD689 Tutorial Question Legal LiabilityJebatNo ratings yet

- Lotus KFM Berhad FADocument19 pagesLotus KFM Berhad FAGeorge BichangaNo ratings yet

- HRM648 Case Study Group AssignmentDocument9 pagesHRM648 Case Study Group Assignment2022753001No ratings yet

- Draft Ads530Document11 pagesDraft Ads530Izzianie HusinNo ratings yet

- Report Managerial Finance@UniklDocument18 pagesReport Managerial Finance@UniklLee WongNo ratings yet

- Datuk Yap Pak Leong v. Ketua Pengarah Hasil Dalam Negeri - BKI-14-1/2-2013Document7 pagesDatuk Yap Pak Leong v. Ketua Pengarah Hasil Dalam Negeri - BKI-14-1/2-2013Vasanth TamilselvanNo ratings yet

- Chapter 01 IntroductionDocument18 pagesChapter 01 IntroductionzamriNo ratings yet

- AUDITORDocument17 pagesAUDITORMalNo ratings yet

- Word FULLDocument7 pagesWord FULLfara_lianaNo ratings yet

- Current IssueDocument4 pagesCurrent Issueareep94No ratings yet

- Strategic Management (Maf661) : Submission DateDocument1 pageStrategic Management (Maf661) : Submission Dateareep94No ratings yet

- Hilton - Maher - SeltoDocument21 pagesHilton - Maher - Seltoareep94No ratings yet

- Chapter 3 MAF661Document26 pagesChapter 3 MAF661areep94No ratings yet

- Chapter 1Document48 pagesChapter 1areep94No ratings yet

- Chapter 3 MAF661Document26 pagesChapter 3 MAF661areep94No ratings yet

- KafalahDocument6 pagesKafalahareep94No ratings yet

- WadiahDocument11 pagesWadiahareep94100% (1)

- Law IndividualDocument5 pagesLaw Individualareep94No ratings yet

- Muhammad Nazri Bin Ramli Director of Group QualityDocument1 pageMuhammad Nazri Bin Ramli Director of Group Qualityareep94No ratings yet

- Head OfficeDocument1 pageHead Officeareep94No ratings yet

- InvoicouDocument16 pagesInvoicoustock18100% (1)

- Internship Report 2nd PartDocument89 pagesInternship Report 2nd PartAli Asgor RatonNo ratings yet

- Rekonsiliasi BankDocument3 pagesRekonsiliasi BankTata Intan TamaraNo ratings yet

- Suncoast Account Statement: Access Your Account: Sunnet Online Banking Sunmobile App Suntel Phone BankingDocument6 pagesSuncoast Account Statement: Access Your Account: Sunnet Online Banking Sunmobile App Suntel Phone BankingolaNo ratings yet

- Case Study On Letter of CreditDocument9 pagesCase Study On Letter of CreditPrahant KumarNo ratings yet

- Acct Statement - XX4767 - 24042023Document3 pagesAcct Statement - XX4767 - 24042023Tamil VaengaiNo ratings yet

- Tally Lab ManualDocument50 pagesTally Lab ManualDeepika Sharma100% (5)

- Muthoot Fincorp CalrificationsDocument6 pagesMuthoot Fincorp CalrificationslulughoshNo ratings yet

- Usage Guide - Rewards Plus PDFDocument8 pagesUsage Guide - Rewards Plus PDFHemant JainNo ratings yet

- Proof of Cash: By: LailaneDocument19 pagesProof of Cash: By: LailaneKyle BrianNo ratings yet

- PAT - Digest Compilation No. 6 (PARTNERSHIP)Document122 pagesPAT - Digest Compilation No. 6 (PARTNERSHIP)Jam PagsuyoinNo ratings yet

- Sanjeev CVDocument3 pagesSanjeev CVCYGNUSMLS ACCOUNTSNo ratings yet

- Support Package Terms and ConditionsDocument2 pagesSupport Package Terms and ConditionsArs OrpheusNo ratings yet

- The Cash Receipts JournalDocument3 pagesThe Cash Receipts JournalRandy AlbutraNo ratings yet

- Buss. Finance FinalDocument7 pagesBuss. Finance FinalAlvin Vin VinNo ratings yet

- INTACC1Document2 pagesINTACC1Ronalyn LajomNo ratings yet

- WeRPN Form FillableDocument2 pagesWeRPN Form FillablemiiszNo ratings yet

- Account Statement For Account:22112413000022: Branch DetailsDocument4 pagesAccount Statement For Account:22112413000022: Branch Detailsvishwak properties mangal avenueNo ratings yet

- Bank Liquidity Policy StatementDocument19 pagesBank Liquidity Policy StatementapluNo ratings yet

- 3 Woody v. National Bank of Rocky MountDocument2 pages3 Woody v. National Bank of Rocky MountrNo ratings yet

- Auditing The Expenditure CycleDocument4 pagesAuditing The Expenditure CycleIndri IswardhaniNo ratings yet

- Axis BankDocument20 pagesAxis BankXYZ909No ratings yet

- MC - Internal AuditDocument12 pagesMC - Internal AuditMegawati MediyaniNo ratings yet

- Import Form 2018Document6 pagesImport Form 2018tejasg82100% (2)

- Health Insurance Brochure - HDFC ERGO PREMIUMS PDFDocument4 pagesHealth Insurance Brochure - HDFC ERGO PREMIUMS PDFram_341No ratings yet