You might also like

- Crosswalk CPA Review: Tax Inflation Adjustments 2021Document15 pagesCrosswalk CPA Review: Tax Inflation Adjustments 2021Adhira VenkatNo ratings yet

- Crosswalk CPA Review: Tax UpdateDocument4 pagesCrosswalk CPA Review: Tax UpdateAdhira VenkatNo ratings yet

- Ea Ea1 Su1 CCDocument2 pagesEa Ea1 Su1 CCAnkit chouhanNo ratings yet

- S S 'S A: Dule37 Taxes: Gift ND EstateDocument2 pagesS S 'S A: Dule37 Taxes: Gift ND EstateEl-Sayed MohammedNo ratings yet

- Pearsons Federal Taxation 2019 Individuals 32nd Edition Rupert Test BankDocument25 pagesPearsons Federal Taxation 2019 Individuals 32nd Edition Rupert Test BankMarkHalldxaj100% (40)

- Pearsons Federal Taxation 2019 Individuals 32nd Edition Rupert Test BankDocument36 pagesPearsons Federal Taxation 2019 Individuals 32nd Edition Rupert Test Bankresegluerud59d100% (20)

- 333 LineDocument25 pages333 LineTiffany BrooksNo ratings yet

- TaxDocument14 pagesTaxXinyi JiangNo ratings yet

- Individual Deductions Solutions Manual ProblemsDocument10 pagesIndividual Deductions Solutions Manual ProblemsSarah Marie Layton50% (2)

- Chapter 2BDocument28 pagesChapter 2BAlmira Alic TurcinovicNo ratings yet

- Accuracy Checking - US TaxationTestDocument10 pagesAccuracy Checking - US TaxationTestAmit ManyalNo ratings yet

- REG-02 F8fe2e8Document52 pagesREG-02 F8fe2e8Vidyadhar TRNo ratings yet

- Dwnload Full Pearsons Federal Taxation 2019 Individuals 32nd Edition Rupert Test Bank PDFDocument20 pagesDwnload Full Pearsons Federal Taxation 2019 Individuals 32nd Edition Rupert Test Bank PDFsportfulscenefulzb3nh100% (13)

- A. The Constitution and The Income Tax: Federal Income Tax Professor Morrison Fall 2003 CHAPTER 1: IntroductionDocument67 pagesA. The Constitution and The Income Tax: Federal Income Tax Professor Morrison Fall 2003 CHAPTER 1: IntroductioncjleopNo ratings yet

- Ch4-Recordedlecture-Fall2023 17 5166787619170306Document38 pagesCh4-Recordedlecture-Fall2023 17 5166787619170306ronny nyagakaNo ratings yet

- BUS 168A Midterm ReviewDocument5 pagesBUS 168A Midterm ReviewcalebrmanNo ratings yet

- OutlineDocument71 pagesOutlineMaxwell NdunguNo ratings yet

- South Western Federal Taxation 2017 Comprehensive 40Th Edition Hoffman Solutions Manual Full Chapter PDFDocument36 pagesSouth Western Federal Taxation 2017 Comprehensive 40Th Edition Hoffman Solutions Manual Full Chapter PDFfred.henderson352100% (10)

- South-Western Federal Taxation 2016 Individual Income Taxes 39th Edition Hoffman Solutions Manual 1Document26 pagesSouth-Western Federal Taxation 2016 Individual Income Taxes 39th Edition Hoffman Solutions Manual 1alisha100% (48)

- South Western Federal Taxation 2016 Individual Income Taxes 39Th Edition Hoffman Solutions Manual Full Chapter PDFDocument36 pagesSouth Western Federal Taxation 2016 Individual Income Taxes 39Th Edition Hoffman Solutions Manual Full Chapter PDFfred.henderson352100% (11)

- Filling For Claim For RefundDocument8 pagesFilling For Claim For RefundsheldonNo ratings yet

- Individual Taxation 2013 Pratt 7th Edition Test BankDocument19 pagesIndividual Taxation 2013 Pratt 7th Edition Test Bankbrianbradyogztekbndm100% (42)

- South Western Federal Taxation 2016 Essentials of Taxation Individuals and Business Entities 19th Edition Raabe Solutions ManualDocument44 pagesSouth Western Federal Taxation 2016 Essentials of Taxation Individuals and Business Entities 19th Edition Raabe Solutions Manualvernier.decyliclnn4100% (22)

- Chapter 10Document4 pagesChapter 10张心怡No ratings yet

- Trusts and EstatesDocument140 pagesTrusts and EstatesSam Bam100% (1)

- Assignment: Taxation LawDocument9 pagesAssignment: Taxation Lawtanmay agrawalNo ratings yet

- IG CH 03Document20 pagesIG CH 03Basa TanyNo ratings yet

- Personal Financial PlanningDocument10 pagesPersonal Financial PlanningTam PhamNo ratings yet

- Individual Taxation 2013 Pratt 7th Edition Test BankDocument19 pagesIndividual Taxation 2013 Pratt 7th Edition Test BankCharles Davis100% (34)

- The Saver's Tax Credit: Are You Saving in A 401 (K) or 403 (B) Plan?Document1 pageThe Saver's Tax Credit: Are You Saving in A 401 (K) or 403 (B) Plan?Gina McCaffreyNo ratings yet

- IND 14 CHP 04 2A Textbook Problems 2012 SolutionsDocument20 pagesIND 14 CHP 04 2A Textbook Problems 2012 SolutionsrakutenmeeshoNo ratings yet

- Regulation MyNotesDocument50 pagesRegulation MyNotesaudalogy100% (1)

- 1 What Is The Deadline For Making A Contribution ToDocument1 page1 What Is The Deadline For Making A Contribution Tohassan taimourNo ratings yet

- Individual Federal Tax UpdatesDocument17 pagesIndividual Federal Tax Updatessean dale porlaresNo ratings yet

- 529credit SS1Document1 page529credit SS1loristurdevantNo ratings yet

- 5 Big Social Security Changes Took Effect in January 2024Document4 pages5 Big Social Security Changes Took Effect in January 2024617249399No ratings yet

- REG QuestionsDocument133 pagesREG Questionsalisha0104No ratings yet

- Income Tax Fundamentals 2019 37th Edition Whittenburg Solutions ManualDocument15 pagesIncome Tax Fundamentals 2019 37th Edition Whittenburg Solutions ManualMarvinGarnerfedpm100% (14)

- Lifetime Giving AND Inter Vivos Gifts: Greenfield Stein & Senior LLP New York, Ny Updated and Co-Authored byDocument30 pagesLifetime Giving AND Inter Vivos Gifts: Greenfield Stein & Senior LLP New York, Ny Updated and Co-Authored byVlad ZernovNo ratings yet

- 5 Big Social Security Changes Took Effect in January 2024Document4 pages5 Big Social Security Changes Took Effect in January 2024617249399No ratings yet

- Text 67C92BDA872B 1Document3 pagesText 67C92BDA872B 1AVNo ratings yet

- Tax Cuts and Jobs Act of 2017: Reduced Individual Tax RatesDocument3 pagesTax Cuts and Jobs Act of 2017: Reduced Individual Tax RatesAlex SimonettiNo ratings yet

- ACC-553 Federal Taxation Midterm Exam (Keller)Document9 pagesACC-553 Federal Taxation Midterm Exam (Keller)robertmoreno0% (1)

- F 1040 EsDocument12 pagesF 1040 EsEndu EnduroNo ratings yet

- 2021 T2 TPLA601 Final Exam STUDENT v1Document16 pages2021 T2 TPLA601 Final Exam STUDENT v1Anas HassanNo ratings yet

- 2009 R-1 Class Questions PreviewDocument11 pages2009 R-1 Class Questions PreviewJaffery143No ratings yet

- Tax Compliance, The IRS, and Tax Authorities: 2020 EditionDocument44 pagesTax Compliance, The IRS, and Tax Authorities: 2020 EditionAhmed AdamjeeNo ratings yet

- Solution 1: Calculation of Total Assessable Income, Taxable Income, Tax LiabilityDocument14 pagesSolution 1: Calculation of Total Assessable Income, Taxable Income, Tax LiabilityDevender SharmaNo ratings yet

- CH 4 & 5 Extra Practic Summer 2023Document9 pagesCH 4 & 5 Extra Practic Summer 2023Ruth KatakaNo ratings yet

- Acct 4220 Additional Review Questions For Final ExamDocument5 pagesAcct 4220 Additional Review Questions For Final ExamrakutenmeeshoNo ratings yet

- LEGT2751 Lecture 1Document14 pagesLEGT2751 Lecture 1reflecti0nNo ratings yet

- Chapter 7 TBDocument25 pagesChapter 7 TBJaasdeepSingh0% (1)

- US and Canada Tax ChangesDocument11 pagesUS and Canada Tax ChangesGANYA JOKERNo ratings yet

- ACCT226 Final ReviewDocument41 pagesACCT226 Final ReviewMahesh YadavNo ratings yet

- Acc - 401 Week 4Document3 pagesAcc - 401 Week 4Accounting GuyNo ratings yet

- 1 Corporate Operations - Part 3Document22 pages1 Corporate Operations - Part 3Van DinhNo ratings yet

- American Rescue Plan Act of 2021 - An AnalysisDocument37 pagesAmerican Rescue Plan Act of 2021 - An Analysisanthony jassoNo ratings yet

- MT Test Review-Taxation 1-Win 2024Document4 pagesMT Test Review-Taxation 1-Win 2024Mariola AlkuNo ratings yet

- Fire Your Over-Priced Financial Advisor and Retire SoonerFrom EverandFire Your Over-Priced Financial Advisor and Retire SoonerRating: 5 out of 5 stars5/5 (1)

- Module 22 F Deral Sec Rities Cts and Antitrust La WDocument2 pagesModule 22 F Deral Sec Rities Cts and Antitrust La WHazem El SayedNo ratings yet

- Module 22 Federal Securities Acts and Antitrust Law: A. Securities Act ofDocument2 pagesModule 22 Federal Securities Acts and Antitrust Law: A. Securities Act ofHazem El SayedNo ratings yet

- 2 Eptanc: C Offer C - Acc eDocument3 pages2 Eptanc: C Offer C - Acc eHazem El SayedNo ratings yet

- CO Tracts: T U R Li Ui HM N LDocument2 pagesCO Tracts: T U R Li Ui HM N LHazem El SayedNo ratings yet

- Module 22 Federal Securities CTS D Antitrust L: A AN AWDocument2 pagesModule 22 Federal Securities CTS D Antitrust L: A AN AWHazem El SayedNo ratings yet

- Module 21 Professional Responsi Ilities: MU EADocument1 pageModule 21 Professional Responsi Ilities: MU EAHazem El SayedNo ratings yet

- Module 21 P Fessional Responsi I ES: RO B LitiDocument2 pagesModule 21 P Fessional Responsi I ES: RO B LitiHazem El SayedNo ratings yet

- Testing Application Control Activi Ies (Continued) : Auditing With Technology - Module 6Document1 pageTesting Application Control Activi Ies (Continued) : Auditing With Technology - Module 6Hazem El SayedNo ratings yet

- Module 21 Professional Responsibilities: Statutory Liabi Ity To Third Parties Securities Exchange Act ofDocument2 pagesModule 21 Professional Responsibilities: Statutory Liabi Ity To Third Parties Securities Exchange Act ofHazem El SayedNo ratings yet

- Secured Transactions: MU IP E C Ce A Swe SDocument1 pageSecured Transactions: MU IP E C Ce A Swe SHazem El SayedNo ratings yet

- Q: BANK-0001: AnswersDocument48 pagesQ: BANK-0001: AnswersHazem El SayedNo ratings yet

- United States Estate (And Generation-Skipping Transfer) Tax ReturnDocument31 pagesUnited States Estate (And Generation-Skipping Transfer) Tax ReturnHazem El SayedNo ratings yet

- Form - 1065 - Schedule - k1 PDFDocument2 pagesForm - 1065 - Schedule - k1 PDFHazem El SayedNo ratings yet

- Net Income (Loss) Reconciliation For Corporations With Total Assets of $10 Million or MoreDocument3 pagesNet Income (Loss) Reconciliation For Corporations With Total Assets of $10 Million or MoreHazem El SayedNo ratings yet

- f1040 PDFDocument2 pagesf1040 PDFHazem El SayedNo ratings yet

- Study Unit 20Document13 pagesStudy Unit 20Hazem El SayedNo ratings yet

- United States Gift (And Generation-Skipping Transfer) Tax ReturnDocument4 pagesUnited States Gift (And Generation-Skipping Transfer) Tax ReturnHazem El SayedNo ratings yet

- Subsequent Events (Continued)Document1 pageSubsequent Events (Continued)Hazem El SayedNo ratings yet

- Management Representations (Continued) : Evidence - Module 3Document2 pagesManagement Representations (Continued) : Evidence - Module 3Hazem El SayedNo ratings yet

- Subsequent Discovery of Facts: Evidence - Module 3Document1 pageSubsequent Discovery of Facts: Evidence - Module 3Hazem El SayedNo ratings yet

- Internal Auditors: Evidence - Module 3Document2 pagesInternal Auditors: Evidence - Module 3Hazem El SayedNo ratings yet

- Invento : Auditing (Continued)Document1 pageInvento : Auditing (Continued)Hazem El SayedNo ratings yet

- Related Parties (Continued) : Evidence - Module 3Document2 pagesRelated Parties (Continued) : Evidence - Module 3Hazem El SayedNo ratings yet

- Working Papers (Continued) : Evidence - Module 3Document2 pagesWorking Papers (Continued) : Evidence - Module 3Hazem El SayedNo ratings yet

- Working Papers (Continued) : Evidence - Module 3Document1 pageWorking Papers (Continued) : Evidence - Module 3Hazem El SayedNo ratings yet

- Auditing Accounts Payable Purchases (Continued) : Evidence - Module 3Document1 pageAuditing Accounts Payable Purchases (Continued) : Evidence - Module 3Hazem El SayedNo ratings yet

- Litigation, Claims, Assessments (Continued) : Evidence - Module 3Document2 pagesLitigation, Claims, Assessments (Continued) : Evidence - Module 3Hazem El SayedNo ratings yet

- Specialists: Evidence - Module 3Document2 pagesSpecialists: Evidence - Module 3Hazem El SayedNo ratings yet

- Litigation, Claims Assessments: Evidence - Module 3Document2 pagesLitigation, Claims Assessments: Evidence - Module 3Hazem El SayedNo ratings yet

- Invento : Auditing (Continued)Document1 pageInvento : Auditing (Continued)Hazem El SayedNo ratings yet

- Uttar Pradesh Police - Employee Salary System-1Document1 pageUttar Pradesh Police - Employee Salary System-1VinNeet KumarNo ratings yet

- Traces: Details of SalaryDocument4 pagesTraces: Details of SalaryMadu JaguNo ratings yet

- Thomas Green of Laramie Wyoming Has Been A Retail SalesclerkDocument2 pagesThomas Green of Laramie Wyoming Has Been A Retail Salesclerktrilocksp SinghNo ratings yet

- Credit Card Debt AssignmentDocument4 pagesCredit Card Debt Assignmentapi-325884538No ratings yet

- Week 8: Quiz Instructions: Alice B. Habla HUMSS 11-9Document12 pagesWeek 8: Quiz Instructions: Alice B. Habla HUMSS 11-9Alice HablaNo ratings yet

- Income Tax Calculator Fy 2020 21 v1Document8 pagesIncome Tax Calculator Fy 2020 21 v1Yogesh BajajNo ratings yet

- Foreclosure Letter 23-41-25Document3 pagesForeclosure Letter 23-41-25आम्हीं मालवणीNo ratings yet

- HDFC Statement PDFDocument12 pagesHDFC Statement PDFAshok RajaputNo ratings yet

- Unit 4 TdsDocument18 pagesUnit 4 TdsAnshu kumarNo ratings yet

- Personal Financial Planning 14th Edition Billingsley Test BankDocument56 pagesPersonal Financial Planning 14th Edition Billingsley Test BankBen Williams100% (37)

- VOCABULARY Money Book 3Document1 pageVOCABULARY Money Book 3Edison Estalla CutipaNo ratings yet

- Loan AgreementDocument5 pagesLoan AgreementAdv RINKY JAISWALNo ratings yet

- Simple InterestDocument7 pagesSimple InterestmecitfuturedreamsNo ratings yet

- Rate of Interest of Retail Lending Schemes Updated On 01.08.2021Document6 pagesRate of Interest of Retail Lending Schemes Updated On 01.08.2021kanduri saicharanNo ratings yet

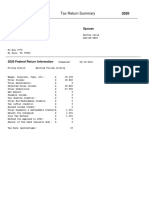

- Tax Return SummaryDocument14 pagesTax Return Summaryevalle13No ratings yet

- Issue of Debenture QuestionsDocument9 pagesIssue of Debenture QuestionsSailesh GoenkkaNo ratings yet

- AcknowledgmentDocument1 pageAcknowledgmentSatyam MaramNo ratings yet

- Quiz 101Document1 pageQuiz 101Mohammad Lomondot AmpasoNo ratings yet

- Lab 1-1 CreditDocument4 pagesLab 1-1 CreditKimberly Anne SP PadillaNo ratings yet

- Kak Luk April 23Document2 pagesKak Luk April 23supri adiNo ratings yet

- CH.3 Annuity PDFDocument29 pagesCH.3 Annuity PDFJenalyn MacarilayNo ratings yet

- Callenmaycongdasan: Page1of3 Blk10Lot9Brgysilingbatapandi 3 1 8 9 - 3 7 3 5 - 3 7 Villagei Pandibulacanprovince 3 0 1 4Document4 pagesCallenmaycongdasan: Page1of3 Blk10Lot9Brgysilingbatapandi 3 1 8 9 - 3 7 3 5 - 3 7 Villagei Pandibulacanprovince 3 0 1 4Callen DasanNo ratings yet

- Kavita 2Document2 pagesKavita 2api-3721187No ratings yet

- Business and Accounting Studies - Grade 11 Worksheet 5: Record The Below Transactions in AccountsDocument2 pagesBusiness and Accounting Studies - Grade 11 Worksheet 5: Record The Below Transactions in AccountsDinukshiya SelvaduraiNo ratings yet

- AUZao 3 IPv 2 LR 2 AZIDocument7 pagesAUZao 3 IPv 2 LR 2 AZIrajarao001No ratings yet

- Rs. 13.00 Rs. 1,318.22 Rs. 1,311.00: 11 Feb 2023 To 10 Mar 2023Document3 pagesRs. 13.00 Rs. 1,318.22 Rs. 1,311.00: 11 Feb 2023 To 10 Mar 2023Aayush KumarNo ratings yet

- Gen Math Periodical Test October For PrintingDocument2 pagesGen Math Periodical Test October For PrintingDerek AsejoNo ratings yet

- Minggu 2 - 3 - Time Value of MoneyDocument79 pagesMinggu 2 - 3 - Time Value of MoneylisdhiyantoNo ratings yet

- Closing Disclosure: Loan TermsDocument3 pagesClosing Disclosure: Loan TermsSupreet KaurNo ratings yet

- Statement From-01 03 2021to-20 03 2023 PDFDocument2 pagesStatement From-01 03 2021to-20 03 2023 PDFAniket Singh SengarNo ratings yet