You might also like

- The Beginning of Business PDFDocument10 pagesThe Beginning of Business PDFSalma AkilNo ratings yet

- or Read: Daf 1160 Engine PDF EbookDocument5 pagesor Read: Daf 1160 Engine PDF Ebookmohammadrohaizad0% (2)

- Free Download Indirect Tax Book For Ca Final Bangar PDFDocument4 pagesFree Download Indirect Tax Book For Ca Final Bangar PDFNikhil Agrawal0% (3)

- Questions On Value PF SupplyDocument4 pagesQuestions On Value PF SupplyMadhuram SharmaNo ratings yet

- GST - Notes For BU IV Sem PDFDocument149 pagesGST - Notes For BU IV Sem PDFSpring BaharNo ratings yet

- Syllabus - GST BeginnerDocument4 pagesSyllabus - GST Beginnernayra khanNo ratings yet

- Boarding PassDocument1 pageBoarding PassEsposito FilippoNo ratings yet

- E-Invoicing Under GST PPT TheTaxTellersDocument8 pagesE-Invoicing Under GST PPT TheTaxTellersThe Tax TellersNo ratings yet

- Eway BillDocument35 pagesEway BillShivaniNo ratings yet

- GST - ReturnsDocument30 pagesGST - ReturnsAniket Rastogi100% (2)

- 8 July-Absent - Kavya's Notes 9 JulyDocument57 pages8 July-Absent - Kavya's Notes 9 JulyAnurag SinghNo ratings yet

- Audit Checklist For Goods and Services TaxDocument4 pagesAudit Checklist For Goods and Services Taxmani1970% (1)

- GST STeps To File ReturnDocument22 pagesGST STeps To File ReturnAnnu KashyapNo ratings yet

- E Way Bill Under GST 1.2Document43 pagesE Way Bill Under GST 1.2Kunal KapadiaNo ratings yet

- ITC Provisions and Rules in GSTDocument8 pagesITC Provisions and Rules in GSTAnonymous ikQZphNo ratings yet

- AX Educted at Ource - I: KPPM & AssociatesDocument67 pagesAX Educted at Ource - I: KPPM & AssociatesSaksham JoshiNo ratings yet

- Impact of GST On Warehousing and Supply ChainDocument39 pagesImpact of GST On Warehousing and Supply ChainSundaravaradhan Iyengar100% (6)

- Bill of EntryDocument15 pagesBill of EntryAbhinav Verma0% (1)

- Return GST IndiaDocument56 pagesReturn GST IndiathecoltNo ratings yet

- GST Input Tax Credit NotesDocument13 pagesGST Input Tax Credit Notesa_bc691973No ratings yet

- GST PDFDocument81 pagesGST PDFPankaj JainNo ratings yet

- Central ExciseDocument22 pagesCentral ExcisesadathnooriNo ratings yet

- GST User ManuelDocument195 pagesGST User Manuelsakthi raoNo ratings yet

- Introduction to GST in IndiaDocument124 pagesIntroduction to GST in IndiaAruna RajappaNo ratings yet

- Advance Tax Payment DatesDocument11 pagesAdvance Tax Payment DatesAdv Aastha MakkarNo ratings yet

- E-Book On GST by CA. (DR.) G. S. Grewal - 2020Document58 pagesE-Book On GST by CA. (DR.) G. S. Grewal - 2020Aarav DhingraNo ratings yet

- ITC FundamentalsDocument114 pagesITC FundamentalsRAUNAQ SHARMANo ratings yet

- Everything You Need to Know About GST ReturnsDocument11 pagesEverything You Need to Know About GST ReturnsYukta AgrawalNo ratings yet

- GST Registration NotesDocument13 pagesGST Registration NotesNagashree RANo ratings yet

- Import Export Under GSTDocument9 pagesImport Export Under GSTVijaya PawarNo ratings yet

- TdsDocument22 pagesTdsFRANCIS JOSEPHNo ratings yet

- GST in India - Objectives, Concerns and ChallengesDocument44 pagesGST in India - Objectives, Concerns and Challengesakhilca87% (15)

- Ready Reckoner For Preparing GSTR-9Document12 pagesReady Reckoner For Preparing GSTR-9SATVINDER WALIANo ratings yet

- GST Impact On The Supply ChainDocument8 pagesGST Impact On The Supply ChainAamiTataiNo ratings yet

- Goods & Services Act FinalDocument78 pagesGoods & Services Act FinalParvesh AghiNo ratings yet

- Guide To CGST, SGST and IGST: Inter-State Vs Intra-StateDocument6 pagesGuide To CGST, SGST and IGST: Inter-State Vs Intra-StateSuman IndiaNo ratings yet

- GST PPT June19Document65 pagesGST PPT June19yash bhushanNo ratings yet

- GST ReturnsDocument3 pagesGST ReturnsTru TaxNo ratings yet

- GST GuideDocument46 pagesGST GuideVikasNo ratings yet

- GSTDocument51 pagesGSTINDERDEEPNo ratings yet

- GST impact on Income TaxDocument14 pagesGST impact on Income TaxNAMAN KANSALNo ratings yet

- Financial Statements SummaryDocument53 pagesFinancial Statements Summaryrachealll100% (1)

- Chargeble GSTDocument87 pagesChargeble GSTgopaljha84No ratings yet

- BCom Income Tax Procedure and PracticeDocument61 pagesBCom Income Tax Procedure and PracticeUjjwal KandhaweNo ratings yet

- Advanced AccountancyDocument202 pagesAdvanced Accountancybharat wankhede100% (1)

- PPT-on-GST Annual-ReturnDocument33 pagesPPT-on-GST Annual-Returnshrutha p jainNo ratings yet

- Chapter 5 GST - ProblemsDocument10 pagesChapter 5 GST - Problemsbalaji RNo ratings yet

- Customs Revision Notes PDFDocument10 pagesCustoms Revision Notes PDFShaan AmanNo ratings yet

- GST Return Business Process For GSTDocument72 pagesGST Return Business Process For GSTAccounting & Taxation100% (1)

- GST Question BankDocument109 pagesGST Question Bankneeraj goyalNo ratings yet

- Income Tax & GST: 2 Mark Questions With Answers - (Calicut University)Document2 pagesIncome Tax & GST: 2 Mark Questions With Answers - (Calicut University)Ashwini GanigerNo ratings yet

- 133 GST JudgmentsDocument224 pages133 GST Judgmentsrohit100% (1)

- Handbook On Interest, Late Fee and Penalties Under GSTDocument64 pagesHandbook On Interest, Late Fee and Penalties Under GSTLeenaNo ratings yet

- Topic: Page NoDocument21 pagesTopic: Page NoAcchu BajajNo ratings yet

- Vision Collage of Management Kanpur Submitted To, Miss Keerti Tiwari Submitted By, M/S. Anam FatimaDocument24 pagesVision Collage of Management Kanpur Submitted To, Miss Keerti Tiwari Submitted By, M/S. Anam FatimaAnam FatimaNo ratings yet

- GST Question Bank - by CA Yachana Mutha BhuratDocument349 pagesGST Question Bank - by CA Yachana Mutha BhuratP LAVANYA100% (1)

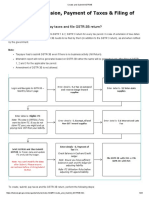

- File GSTR-3B and pay GST onlineDocument23 pagesFile GSTR-3B and pay GST onlineBala VinayagamNo ratings yet

- Indirect and Customs ActDocument95 pagesIndirect and Customs ActAyushi TiwariNo ratings yet

- Export Finance Blackbook ProjectDocument89 pagesExport Finance Blackbook ProjectkajalNo ratings yet

- Bank Reconciliation StatementDocument16 pagesBank Reconciliation StatementBilal Ali SyedNo ratings yet

- Final FinalDocument15 pagesFinal FinalRavi MehraNo ratings yet

- E WayBillDocument6 pagesE WayBillDharmesh ChauhanNo ratings yet

- E Way BillDocument44 pagesE Way BillRanju 08No ratings yet

- Project Budget Template 101Document8 pagesProject Budget Template 101Rachel LaguidaoNo ratings yet

- Rail Track Flaw Detection Using MATLABDocument28 pagesRail Track Flaw Detection Using MATLABeshuNo ratings yet

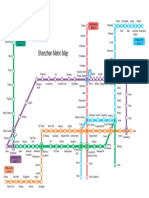

- Shenzhen Metro MapDocument1 pageShenzhen Metro Mapamirjoker646No ratings yet

- Manual Bridge Navigational Watchkeepers Alarm System Iss01 Rev05Document40 pagesManual Bridge Navigational Watchkeepers Alarm System Iss01 Rev05e3eriknNo ratings yet

- DNV - Comfort ClassDocument18 pagesDNV - Comfort ClasslonghvacNo ratings yet

- Srs Ticket PDFDocument1 pageSrs Ticket PDFTapan Chandratre0% (1)

- Turbofan - WikipediaDocument17 pagesTurbofan - WikipediaAnonymous tSYkkHToBPNo ratings yet

- CompanyCodes 20230404 1004Document87 pagesCompanyCodes 20230404 1004asd fdaNo ratings yet

- Manitowoc Cranes Machine Component Index for TMS760E Serial 222341Document1,315 pagesManitowoc Cranes Machine Component Index for TMS760E Serial 222341MOVILPETROL SAS50% (2)

- Air Canada v. CIR - Taxation Law - DebtDocument3 pagesAir Canada v. CIR - Taxation Law - DebtMichael VillalonNo ratings yet

- 30 kW Maintenance Free Stirling Engine for High Performance Dish CSPDocument15 pages30 kW Maintenance Free Stirling Engine for High Performance Dish CSPOmar HelmyNo ratings yet

- Aboitiz Shipping Corp V New India Assurance Co. (GR No 156978)Document1 pageAboitiz Shipping Corp V New India Assurance Co. (GR No 156978)Rav Bahri100% (2)

- Siemens PLM NX Automotive Packaging Fs 68168 A3 - tcm27 29307Document5 pagesSiemens PLM NX Automotive Packaging Fs 68168 A3 - tcm27 29307SoumenAtaNo ratings yet

- Teaching ResumeDocument1 pageTeaching Resumeapi-491671554No ratings yet

- VRYR Lauda Normal ChecklistDocument1 pageVRYR Lauda Normal Checklistchristopherchadwick79No ratings yet

- A Deep Learning Approach For Road Damage Detection From Smartphone ImagesDocument4 pagesA Deep Learning Approach For Road Damage Detection From Smartphone ImagesOsama AsifNo ratings yet

- Ata 22 Auto Flight Control System PDFDocument233 pagesAta 22 Auto Flight Control System PDFandres supelano100% (1)

- Organic Compounds Containing Nitrogen - JEE Main 2021 - 2019 Chapter-WiseDocument75 pagesOrganic Compounds Containing Nitrogen - JEE Main 2021 - 2019 Chapter-WiseSatyam KumarNo ratings yet

- Product CATLOG THAILAND - 1595282547Document39 pagesProduct CATLOG THAILAND - 1595282547walter sueroNo ratings yet

- Dinamic Self Levelling Chassis: Plug and Play "No Leaks of Time"Document2 pagesDinamic Self Levelling Chassis: Plug and Play "No Leaks of Time"ВасяNo ratings yet

- Manual Camilla Obstetrica Electrica B-48-InglesDocument15 pagesManual Camilla Obstetrica Electrica B-48-InglesBrevas CuchoNo ratings yet

- 2012 INT PCR CatalogDocument33 pages2012 INT PCR CatalogidulNo ratings yet

- Uas Semester Gasal Bahasa Inggris SMP Kelas Viii KTSPDocument8 pagesUas Semester Gasal Bahasa Inggris SMP Kelas Viii KTSPS NailusNo ratings yet

- LITERATURE REVIEW ON CONSUMER BUYING BEHAVIOUR TOWARDS FOUR WHEELERSDocument12 pagesLITERATURE REVIEW ON CONSUMER BUYING BEHAVIOUR TOWARDS FOUR WHEELERSzaidkhanNo ratings yet

- BPCL Jacketed GasketsDocument15 pagesBPCL Jacketed GasketsPinak VadherNo ratings yet

- Flight Ticket - Ranchi To Bangalore: Fare Rules & BaggageDocument2 pagesFlight Ticket - Ranchi To Bangalore: Fare Rules & Baggagesoni100% (2)

- New Zealand Trip (2017)Document20 pagesNew Zealand Trip (2017)nshamsundar7929No ratings yet