You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5806)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Chapter 3 - Forms of Small Business OwnershipDocument13 pagesChapter 3 - Forms of Small Business OwnershipKristina ChernitskayaNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Option Trading Guide - Introduction PDFDocument65 pagesOption Trading Guide - Introduction PDFRAHUL RAI100% (1)

- Final Exam in Corporation Law Under Atty. Ruben C. Ladia: Arceo, Aveo, Gomez, Nazareno, Samia, TurarayDocument9 pagesFinal Exam in Corporation Law Under Atty. Ruben C. Ladia: Arceo, Aveo, Gomez, Nazareno, Samia, TurarayAlphaphilea Ps100% (1)

- WM 3Document7 pagesWM 3Konsul Detox100% (1)

- Personal Profile Form-BocDocument1 pagePersonal Profile Form-BocMhilet67% (3)

- Application Form For Bir-Broker Clearance Certificate (BCC) For Non-IndividualDocument1 pageApplication Form For Bir-Broker Clearance Certificate (BCC) For Non-IndividualMhiletNo ratings yet

- Special Power of Attorney Know All Men by These PresentsDocument1 pageSpecial Power of Attorney Know All Men by These PresentsMhiletNo ratings yet

- Sample Certification of IncomeDocument1 pageSample Certification of IncomeMhilet100% (1)

- Request Letter To BIR For TCCDocument1 pageRequest Letter To BIR For TCCMhilet100% (3)

- Annex B-1 RR 11-2018 Sworn Statement of Declaration of Gross Sales and ReceiptsDocument1 pageAnnex B-1 RR 11-2018 Sworn Statement of Declaration of Gross Sales and ReceiptsEliza Corpuz Gadon89% (19)

- Agreement For The Sale of ScrapDocument4 pagesAgreement For The Sale of ScrapMhilet57% (23)

- Training AgreementDocument2 pagesTraining AgreementMhilet100% (1)

- MCQDocument19 pagesMCQMhiletNo ratings yet

- GFFS CertificationDocument1 pageGFFS CertificationMhiletNo ratings yet

- Cpale UpdateDocument3 pagesCpale UpdateMhiletNo ratings yet

- Argument On MarijuanaDocument3 pagesArgument On MarijuanaMhiletNo ratings yet

- Cheat Notes-GblDocument4 pagesCheat Notes-GblMhiletNo ratings yet

- Oblicon Quiz 10-2Document1 pageOblicon Quiz 10-2MhiletNo ratings yet

- DOLE Advisory No 01 Guidelines On COmputation of Salary DifferentialDocument7 pagesDOLE Advisory No 01 Guidelines On COmputation of Salary DifferentialMhiletNo ratings yet

- 14 Center Village, Paciano Rizal, Calamba City, Laguna, PhilippinesDocument2 pages14 Center Village, Paciano Rizal, Calamba City, Laguna, PhilippinesMhiletNo ratings yet

- Hiploid and HaploidDocument1 pageHiploid and HaploidMhiletNo ratings yet

- Module CoopDocument1 pageModule CoopMhiletNo ratings yet

- PEZA-registered Firms and Local Business Taxes: Taxwise or OtherwiseDocument3 pagesPEZA-registered Firms and Local Business Taxes: Taxwise or OtherwiseMhiletNo ratings yet

- Cash Surrender ValueDocument2 pagesCash Surrender ValueLourdes AnolNo ratings yet

- Duties and Responsibilities of A Director of A Private Limited Company - IpleadersDocument5 pagesDuties and Responsibilities of A Director of A Private Limited Company - IpleadersvinayakraaoNo ratings yet

- Organisation Commerce Notes of H.S.C.Document176 pagesOrganisation Commerce Notes of H.S.C.Rajan Anthony Parayar78% (9)

- WdmlistDocument267 pagesWdmlistHarshitNo ratings yet

- Assignment CG AnalysisDocument2 pagesAssignment CG AnalysisankitNo ratings yet

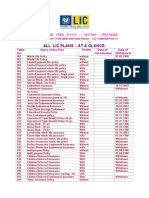

- All LIC PlansDocument4 pagesAll LIC Planslicvivek100% (1)

- ESOPDocument8 pagesESOPKiran GvNo ratings yet

- Form mgt777Document46 pagesForm mgt777fdfladdNo ratings yet

- Corp Law I Research Paper Titles 2020-21Document5 pagesCorp Law I Research Paper Titles 2020-21BatmanNo ratings yet

- Agency ProblemDocument6 pagesAgency ProblemZarkaif KhanNo ratings yet

- Utopia Corporation Law Reviewer 2008Document172 pagesUtopia Corporation Law Reviewer 2008Christian John Rojo100% (3)

- BDO Annual Report Volume 2Document150 pagesBDO Annual Report Volume 2Deb AlejandroNo ratings yet

- Manonmaniam Sundaranar University: M.B.A. - I YearDocument118 pagesManonmaniam Sundaranar University: M.B.A. - I YearRAJANo ratings yet

- Ch01 TB LoftusDocument8 pagesCh01 TB LoftusTata Nguyen100% (1)

- Hariharan PDFDocument10 pagesHariharan PDFHariharan ShekarNo ratings yet

- Partnership For Recit by Group Part 1Document2 pagesPartnership For Recit by Group Part 1Camie YoungNo ratings yet

- Glo 20is 2017 PDFDocument317 pagesGlo 20is 2017 PDFKristine LlamasNo ratings yet

- 002.LEVINE A: ASIC Personal Name ExtractDocument42 pages002.LEVINE A: ASIC Personal Name ExtractFlinders TrusteesNo ratings yet

- Slides Week 2 PDFDocument91 pagesSlides Week 2 PDFYash ModiNo ratings yet

- United States Court of Appeals: PublishedDocument13 pagesUnited States Court of Appeals: PublishedScribd Government DocsNo ratings yet

- Corporation LawDocument9 pagesCorporation LawDEBRA L. BADIOLA-BRACIANo ratings yet

- Prime White Cement Corp. v. IAC, 220 SCRA 103 (1993)Document11 pagesPrime White Cement Corp. v. IAC, 220 SCRA 103 (1993)bentley CobyNo ratings yet

- Corporate Law-IDocument76 pagesCorporate Law-ITzar YS MuskovyNo ratings yet

- The Corporation Code of The Philippines or The Batas Pambansa Bilang 68Document6 pagesThe Corporation Code of The Philippines or The Batas Pambansa Bilang 68cris allea catacutanNo ratings yet

- P-2 TheoryDocument72 pagesP-2 TheoryUdayan KachchhyNo ratings yet

- Indian CG Scorecard PDFDocument91 pagesIndian CG Scorecard PDFJill MehtaNo ratings yet