You might also like

- Chapter 9 - DepreciationDocument47 pagesChapter 9 - DepreciationsajalNo ratings yet

- Aman MathurDocument31 pagesAman MathursajalNo ratings yet

- Chapter 14 Association RulesDocument23 pagesChapter 14 Association RulessajalNo ratings yet

- Case Study ON Eastern Condiments Pvt. LTDDocument9 pagesCase Study ON Eastern Condiments Pvt. LTDsajalNo ratings yet

- Talent Management PracticesDocument15 pagesTalent Management PracticessajalNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5796)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Black Book GDocument90 pagesBlack Book GYashNo ratings yet

- Manufactures Near byDocument28 pagesManufactures Near bykomal LPS0% (1)

- MSB ATM GuidanceDocument3 pagesMSB ATM GuidanceJay CaplanNo ratings yet

- When Is The Best Time To Buy A StockDocument11 pagesWhen Is The Best Time To Buy A StockAnonymous w6TIxI0G8lNo ratings yet

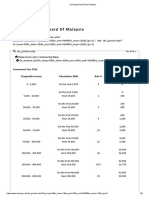

- Inland Revenue Board of Malaysia: Eng MalDocument6 pagesInland Revenue Board of Malaysia: Eng Malathirah jamaludinNo ratings yet

- The Financial Instability HypothesisDocument10 pagesThe Financial Instability HypothesisAculina DariiNo ratings yet

- Heros Convent HR - Sec.School First Term Examination Class - 4 Maths M.M.80Document3 pagesHeros Convent HR - Sec.School First Term Examination Class - 4 Maths M.M.80sunny singhNo ratings yet

- Balance of Payments: Presented by Shamroze SajidDocument18 pagesBalance of Payments: Presented by Shamroze SajidAejaz MohamedNo ratings yet

- Lesson 2 - Advanced Financial Statement Analysis and ValuationDocument66 pagesLesson 2 - Advanced Financial Statement Analysis and ValuationNoel Salazar JrNo ratings yet

- MINI CASE - Chapter 1Document3 pagesMINI CASE - Chapter 1JOBIN VARGHESENo ratings yet

- SFA Framing Guide 07 PDFDocument12 pagesSFA Framing Guide 07 PDFalattar98No ratings yet

- Study of Investments in Bonds PDFDocument67 pagesStudy of Investments in Bonds PDFMkingNo ratings yet

- Cash Count SheetDocument1 pageCash Count SheetPrincessa LeeNo ratings yet

- 0469 MihamaDocument1 page0469 Mihamasaurav royNo ratings yet

- Penawaran BerthaDocument2 pagesPenawaran BerthaTito AdiNo ratings yet

- Hope and WishDocument4 pagesHope and WishsupriyantoNo ratings yet

- Economics Money Banking & International Trade-1Document18 pagesEconomics Money Banking & International Trade-1Nandan Gowda100% (1)

- Beacon Pharma Ltd. - UpdateDocument12 pagesBeacon Pharma Ltd. - UpdateMd. Mustak AhmedNo ratings yet

- Chain Whitepaper PDFDocument32 pagesChain Whitepaper PDFdazeeeNo ratings yet

- 10 K 12 31 19 9Document85 pages10 K 12 31 19 9Conny CastroNo ratings yet

- BSNL March 2023 BillDocument3 pagesBSNL March 2023 BillLahu AadeNo ratings yet

- Practise - Chap 7& 8 (Stu)Document7 pagesPractise - Chap 7& 8 (Stu)Nguyen Ngoc Thanh (K17 HCM)No ratings yet

- Cpec A Threat or A Game Changer For PakistanDocument3 pagesCpec A Threat or A Game Changer For PakistanAyesha FakharNo ratings yet

- MOP (Method of Procedure) : TFM (Technical Facilities Management)Document7 pagesMOP (Method of Procedure) : TFM (Technical Facilities Management)MEER MUSTAFA ALINo ratings yet

- Request For Quotation Number (Doh-Gb50-2021)Document5 pagesRequest For Quotation Number (Doh-Gb50-2021)Belinda Williams100% (1)

- National Income and Price DeterminationDocument3 pagesNational Income and Price Determinationbustiman20No ratings yet

- As We All Are AwareDocument17 pagesAs We All Are AwaremgrfanNo ratings yet

- 0 Transmitting 132Kv Substation 1 Project Master Schedule: Construction DrawingsDocument39 pages0 Transmitting 132Kv Substation 1 Project Master Schedule: Construction Drawingsshahidbolar0% (1)

- Maybank Annual Report 2020 - Financial Statements (English)Document269 pagesMaybank Annual Report 2020 - Financial Statements (English)YikHau NgNo ratings yet