You might also like

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Golden ArchesDocument2 pagesGolden ArchesAngelina VellaNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- BF235Document33 pagesBF235Angelina VellaNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Mass Media Ethics - ReportDocument9 pagesMass Media Ethics - ReportAngelina VellaNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- 7616 Gianna Sanina Alba Azzolini Final Presentation 506637 1379272871Document13 pages7616 Gianna Sanina Alba Azzolini Final Presentation 506637 1379272871Angelina VellaNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Media PlanningDocument8 pagesMedia PlanningAngelina VellaNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Golden ArchesDocument2 pagesGolden ArchesAngelina VellaNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- 7616 Gianna Sanina Alba Azzolini Mid Term Presentation 520787 1065098158Document13 pages7616 Gianna Sanina Alba Azzolini Mid Term Presentation 520787 1065098158Angelina VellaNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

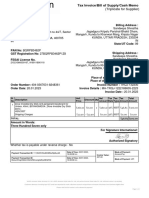

- Invoice DocumentDocument1 pageInvoice DocumentrameshNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Inflation, Deflation and StagflationDocument13 pagesInflation, Deflation and StagflationSteeeeeeeeph100% (1)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Understanding Margins PDFDocument23 pagesUnderstanding Margins PDFDiego BittencourtNo ratings yet

- Materi Dan Soal Soal Pendalaman Ipa Fisika Kls 7 Semester 1 Dan 2Document8 pagesMateri Dan Soal Soal Pendalaman Ipa Fisika Kls 7 Semester 1 Dan 2cui takeNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- 50 Questions To Ask A FranchisorDocument3 pages50 Questions To Ask A FranchisorRegie Sacil EspiñaNo ratings yet

- Cost Behaviour & Decision Making - HodDocument65 pagesCost Behaviour & Decision Making - Hodsrimant100% (2)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Accounting Rate of ReturnDocument7 pagesAccounting Rate of ReturnMahesh RaoNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Assignment 2, PEVCDocument4 pagesAssignment 2, PEVCMohit MehndirattaNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Hindalco-Novelis: Case StudyDocument27 pagesHindalco-Novelis: Case StudyRaj KauravNo ratings yet

- David WintersDocument8 pagesDavid WintersRui BárbaraNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Chapter 5: Strategic Capacity Planning For Products and ServicesDocument17 pagesChapter 5: Strategic Capacity Planning For Products and ServicesAliah RomeroNo ratings yet

- Amira Berdikari - Jurnal Khusus - Hanifah Hilyah SyahDocument9 pagesAmira Berdikari - Jurnal Khusus - Hanifah Hilyah Syahreza hariansyah100% (1)

- Capital Mortgage Insurance - Position PaperDocument4 pagesCapital Mortgage Insurance - Position Papersouthern2011100% (1)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- TP Vii PDFDocument17 pagesTP Vii PDFshekarj100% (3)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Bounding BermudansDocument6 pagesBounding Bermudans楊約翰No ratings yet

- ReviewerDocument34 pagesReviewerBABY JOY SEGUINo ratings yet

- GGP Ackman Presentation Ira Sohn Conf 5-26-10Document89 pagesGGP Ackman Presentation Ira Sohn Conf 5-26-10fstreet100% (2)

- Claim ApplicationDocument2 pagesClaim ApplicationAwkiNo ratings yet

- 2 - AccentForex Competitive Analysis No ScreenshotsDocument1 page2 - AccentForex Competitive Analysis No ScreenshotsTanveer HussainNo ratings yet

- Topic 7 - Presentation of FS (IAS 1) - SVDocument51 pagesTopic 7 - Presentation of FS (IAS 1) - SVHONG NGUYEN THI KIMNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Employee Benefits: Accounting Standard (AS) 15Document67 pagesEmployee Benefits: Accounting Standard (AS) 15hanumanthaiahgowdaNo ratings yet

- Fee Receipt - Lucknow UniversityDocument3 pagesFee Receipt - Lucknow UniversityNirbhay NirajNo ratings yet

- ACCT 10001: Accounting Reports & Analysis Lecture 2 Illustration: ARA Galleries Pty LTDDocument5 pagesACCT 10001: Accounting Reports & Analysis Lecture 2 Illustration: ARA Galleries Pty LTDBáchHợpNo ratings yet

- E) Growth and Survival of FirmsDocument6 pagesE) Growth and Survival of FirmsRACSO elimuNo ratings yet

- Eun 9e International Financial Management PPT CH06 AccessibleDocument31 pagesEun 9e International Financial Management PPT CH06 AccessibleDao Dang Khoa FUG CTNo ratings yet

- DragonpayDocument3 pagesDragonpayJamel YusophNo ratings yet

- ICICI Bank Ltd. Versus Official Liquidator of APS StarDocument17 pagesICICI Bank Ltd. Versus Official Liquidator of APS StarAman Kumar YadavNo ratings yet

- Sweat - ProfileDocument11 pagesSweat - ProfileNathaniel AnumbaNo ratings yet

- Module 34 Share-Based Compensation ProblemDocument1 pageModule 34 Share-Based Compensation ProblemThalia UyNo ratings yet

- SIB 675 - Assignment 2upDocument6 pagesSIB 675 - Assignment 2upMelissa TothNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)