You might also like

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- HO# (7) Chap018 Consumer Loans-, Credit Cards-And Real Estate LendingDocument40 pagesHO# (7) Chap018 Consumer Loans-, Credit Cards-And Real Estate LendingEissa SamNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- HO# (4) Chapter Twelve: Managing and Pricing Deposit ServicesDocument32 pagesHO# (4) Chapter Twelve: Managing and Pricing Deposit ServicesEissa SamNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Grade 5 Online Assignment U 5 L 2Document1 pageGrade 5 Online Assignment U 5 L 2Eissa SamNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- HO# (5) Chapter Sixteen: Lending Policies and Procedures: Managing Credit RiskDocument25 pagesHO# (5) Chapter Sixteen: Lending Policies and Procedures: Managing Credit RiskEissa SamNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Property or Unit Registration Form: Bit - Ly/2WaknuqDocument2 pagesProperty or Unit Registration Form: Bit - Ly/2WaknuqEissa SamNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Compensation HRM 401 Course Syllabus Spring 2020Document10 pagesCompensation HRM 401 Course Syllabus Spring 2020Eissa SamNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Grade 5 Online Assignment U 5 L 2Document1 pageGrade 5 Online Assignment U 5 L 2Eissa SamNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Assignment: Questions 1 2 3 Total Point 3 3 4 10 Student MarkDocument2 pagesAssignment: Questions 1 2 3 Total Point 3 3 4 10 Student MarkEissa SamNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Project (Course-Specific) : CLO#1: Identify and Explain The Issues Involved in Establishing Compensation SystemsDocument2 pagesProject (Course-Specific) : CLO#1: Identify and Explain The Issues Involved in Establishing Compensation SystemsEissa SamNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Property or Unit Registration Form: Bit - Ly/2WaknuqDocument2 pagesProperty or Unit Registration Form: Bit - Ly/2WaknuqEissa SamNo ratings yet

- Compensation HRM 401Document11 pagesCompensation HRM 401Eissa SamNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Research Project BAF421 Spring 2019-2020Document4 pagesResearch Project BAF421 Spring 2019-2020Eissa SamNo ratings yet

- Moodys June2018 PDFDocument9 pagesMoodys June2018 PDFEissa SamNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Course Syllabus: Program Human Resource Management Course Name Recruitment and Selection Course Code HRM 301Document11 pagesCourse Syllabus: Program Human Resource Management Course Name Recruitment and Selection Course Code HRM 301Eissa SamNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Course Syllabus: Program Human Resource Management Course Name Recruitment and Selection Course Code HRM 301Document11 pagesCourse Syllabus: Program Human Resource Management Course Name Recruitment and Selection Course Code HRM 301Eissa SamNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Course Syllabus: Program Human Resource Management Course Name Recruitment and Selection Course Code HRM 301Document11 pagesCourse Syllabus: Program Human Resource Management Course Name Recruitment and Selection Course Code HRM 301Eissa SamNo ratings yet

- HRM 301 Assignment 1Document3 pagesHRM 301 Assignment 1Eissa SamNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- BIM 402 AssignmentDocument3 pagesBIM 402 AssignmentEissa SamNo ratings yet

- Moodys June2018 PDFDocument9 pagesMoodys June2018 PDFEissa SamNo ratings yet

- Course Syllabus: Program Human Resource Management Course Name Recruitment and Selection Course Code HRM 301Document11 pagesCourse Syllabus: Program Human Resource Management Course Name Recruitment and Selection Course Code HRM 301Eissa SamNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Course Syllabus: Program Human Resource Management Course Name Recruitment and Selection Course Code HRM 301Document11 pagesCourse Syllabus: Program Human Resource Management Course Name Recruitment and Selection Course Code HRM 301Eissa SamNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Summary Presentation of The Regulatory Framework - Final 29.02.24 enDocument7 pagesSummary Presentation of The Regulatory Framework - Final 29.02.24 enBOULENOUAR TarikNo ratings yet

- Project Report of Derivatives PDFDocument77 pagesProject Report of Derivatives PDFHilal Ahmed78% (9)

- Shareholder Vs Stakeholder Approach - RSM South Africa Shareholders Vs Stakeholders - Legal Insights - RSM South AfricaDocument3 pagesShareholder Vs Stakeholder Approach - RSM South Africa Shareholders Vs Stakeholders - Legal Insights - RSM South AfricaCasper MaungaNo ratings yet

- Basic Accounting Chapter 1-5 QuizzesDocument6 pagesBasic Accounting Chapter 1-5 QuizzesLuna Shi100% (1)

- Assignment 12 July - NDocument3 pagesAssignment 12 July - NABHINANDAN GHOSH 1927401No ratings yet

- Ratio 4Document13 pagesRatio 4Edgar LayNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Lancaster Engineering IncDocument2 pagesLancaster Engineering IncMamunoor RashidNo ratings yet

- CB1Document6 pagesCB1sankar KNo ratings yet

- Ias 20 - Gov't GrantDocument19 pagesIas 20 - Gov't GrantGail Bermudez100% (1)

- Spto LK TW Iii 2019 PDFDocument90 pagesSpto LK TW Iii 2019 PDFfaulaNo ratings yet

- Financial Statement Analysis of Philex Mining Corp. and Abra Mining & Industrial Corp.Document12 pagesFinancial Statement Analysis of Philex Mining Corp. and Abra Mining & Industrial Corp.nesjynNo ratings yet

- Ent530 - Business Plan - Guidelines & TemplateDocument16 pagesEnt530 - Business Plan - Guidelines & Templateafiqah100% (1)

- Sop and Additional Documents For Vae - 1632115852Document3 pagesSop and Additional Documents For Vae - 1632115852Sales Multi MineralsNo ratings yet

- AFFLE - Investor Presentation - FY21Document19 pagesAFFLE - Investor Presentation - FY21Abhishek MurarkaNo ratings yet

- Net 57,000 Date (5.II.e)Document11 pagesNet 57,000 Date (5.II.e)Kyree VladeNo ratings yet

- Uniparts India LTD.: Jatin MahajanDocument2 pagesUniparts India LTD.: Jatin Mahajanpradeep kumar pradeep kumarNo ratings yet

- Istilah Akuntansi Dalam Bahasa InggrisDocument16 pagesIstilah Akuntansi Dalam Bahasa InggrisDhuny OctavianNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Dollar Amounts in Thousands: Balance SheetDocument1 pageDollar Amounts in Thousands: Balance SheetJai Bhushan BharmouriaNo ratings yet

- Bus - 122 Group ProjectDocument3 pagesBus - 122 Group ProjectKshitiz SherchanNo ratings yet

- Kewangan Korporat LatihanDocument4 pagesKewangan Korporat LatihanfahmiyyahNo ratings yet

- Buscom Quiz: Book Value Fair ValueDocument2 pagesBuscom Quiz: Book Value Fair ValueNairah M. TambieNo ratings yet

- A-Levels Accounting 2003 AnswersDocument21 pagesA-Levels Accounting 2003 Answersbetty makushaNo ratings yet

- HW6 BDocument2 pagesHW6 BBenicel Lane M. D. V.No ratings yet

- Capital Budgeting Techniques 01Document10 pagesCapital Budgeting Techniques 01Evangelystha Lumban TobingNo ratings yet

- FAR - Week 13 & 14 FinalDocument24 pagesFAR - Week 13 & 14 FinalAnthony John BrionesNo ratings yet

- CHAPTER-14: C I R P U I & B C, 2016: Orporate Nsolvency Esolution Rocess Nder Nsolvency Ankruptcy ODEDocument27 pagesCHAPTER-14: C I R P U I & B C, 2016: Orporate Nsolvency Esolution Rocess Nder Nsolvency Ankruptcy ODESrishti NigamNo ratings yet

- Dhanuka Agritech LTDDocument57 pagesDhanuka Agritech LTDSubscriptionNo ratings yet

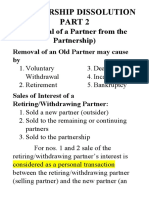

- Chapter 5 - Partnership Dissolution Part 2Document7 pagesChapter 5 - Partnership Dissolution Part 2Xyzra AlfonsoNo ratings yet

- Standard Bank BEE Financing StructuresDocument15 pagesStandard Bank BEE Financing StructuresKhanyile NcubeNo ratings yet

- Pe Investment ThesisDocument8 pagesPe Investment Thesissarahdavisjackson100% (2)