You might also like

- 041924353041-Review Chapter 31Document6 pages041924353041-Review Chapter 31Aimé RandrianantenainaNo ratings yet

- Unit 7 - Class SlidesDocument57 pagesUnit 7 - Class Slidessabelo.j.nkosi.5No ratings yet

- Financial Market-Lecture 10Document28 pagesFinancial Market-Lecture 10Krish ShettyNo ratings yet

- Exchange Rates and the Foreign Exchange Market: An Asset ApproachDocument43 pagesExchange Rates and the Foreign Exchange Market: An Asset ApproachKhalil MohamedNo ratings yet

- Nternational Business FinanceDocument39 pagesNternational Business FinanceTacitus KilgoreNo ratings yet

- Exchange Rates Data 2006-2018Document68 pagesExchange Rates Data 2006-2018John UlziiNo ratings yet

- Foreign Exchange Markets GuideDocument28 pagesForeign Exchange Markets GuideAnshulGuptaNo ratings yet

- Multinational Financial Management: by Sharlaine Mae G. AndalDocument23 pagesMultinational Financial Management: by Sharlaine Mae G. AndalSharlaine AndalNo ratings yet

- SUp0ply Chain - Markov ModelDocument58 pagesSUp0ply Chain - Markov Modelspectrum_48No ratings yet

- Monetary Theories of Exchange RatesDocument22 pagesMonetary Theories of Exchange RatesSumit KumarNo ratings yet

- What Is A Multinational CorporationDocument13 pagesWhat Is A Multinational Corporationmagicalfantasy100% (2)

- International Financial ManagementDocument15 pagesInternational Financial ManagementraviNo ratings yet

- Arbitrage 2Document41 pagesArbitrage 2dawnheraldNo ratings yet

- Open Economy Lecture: BOP and Exchange Rate DeterminationDocument46 pagesOpen Economy Lecture: BOP and Exchange Rate DeterminationLakmal SilvaNo ratings yet

- The Spot Foreign Exchange MarketDocument49 pagesThe Spot Foreign Exchange MarketArun KumarNo ratings yet

- CH 13Document12 pagesCH 13Simona NicolaeNo ratings yet

- Exchange Rate Determination Chap 15Document32 pagesExchange Rate Determination Chap 15Munazza Jabeen50% (4)

- BFC5926 Seminar 8 - FX MarketsDocument43 pagesBFC5926 Seminar 8 - FX MarketsMengdi ZhangNo ratings yet

- Foreign Exchange Market: Market Where The Various National Currencies Are Sold and Bought (Not A Physical Place)Document40 pagesForeign Exchange Market: Market Where The Various National Currencies Are Sold and Bought (Not A Physical Place)Velichka DimitrovaNo ratings yet

- Module 2Document41 pagesModule 2bhargaviNo ratings yet

- Multinational Financial ManagementDocument95 pagesMultinational Financial ManagementANo ratings yet

- The Foreign Exchange Markets: Case: 1. The Collapse of Thai BahtDocument21 pagesThe Foreign Exchange Markets: Case: 1. The Collapse of Thai BahtsoheltushNo ratings yet

- CHapter 3 PDFDocument34 pagesCHapter 3 PDFTania ParvinNo ratings yet

- Exchange Rates: FUQINTRD 683W: Global Markets and InstitutionsDocument57 pagesExchange Rates: FUQINTRD 683W: Global Markets and InstitutionsNaresh KumarNo ratings yet

- Foreign Exchange and Balance of PaymentsDocument94 pagesForeign Exchange and Balance of PaymentsAnkit SinghNo ratings yet

- Forex 2023Document55 pagesForex 2023Sammy MosesNo ratings yet

- International TradeDocument57 pagesInternational TradeSam Ebenezer .SNo ratings yet

- 1 International Financial Markets PDFDocument18 pages1 International Financial Markets PDFshakil zibranNo ratings yet

- Chapter 9 - Foreign Exchange RiskDocument26 pagesChapter 9 - Foreign Exchange RiskAhmed El KhateebNo ratings yet

- Rates of Exchange: Radhakishan V Karthik S Jaichander Yasser FarookDocument15 pagesRates of Exchange: Radhakishan V Karthik S Jaichander Yasser FarookKarthik SankarNo ratings yet

- Interest Rate Parity (IRP) ExplainedDocument30 pagesInterest Rate Parity (IRP) ExplainedRammohanreddy RajidiNo ratings yet

- Interest Rate Parity PresentationDocument31 pagesInterest Rate Parity Presentationviki12334No ratings yet

- Departure From PPPDocument27 pagesDeparture From PPPBhuvan AwasthiNo ratings yet

- Cecchetti 5e Ch10 Foreign ExchangeDocument54 pagesCecchetti 5e Ch10 Foreign ExchangeammendNo ratings yet

- ECON Chapter 7Document8 pagesECON Chapter 7Mushaisano MudauNo ratings yet

- SM 9 PDFDocument20 pagesSM 9 PDFROHIT GULATINo ratings yet

- Forex Quotations and ArbitrageDocument25 pagesForex Quotations and Arbitragerohitpatil699No ratings yet

- If PPTSDocument31 pagesIf PPTSPriti BidasariaNo ratings yet

- ECON216 International Economics: Dr. Florian Gerth Faculty of BusinessDocument27 pagesECON216 International Economics: Dr. Florian Gerth Faculty of BusinessReema HaseebNo ratings yet

- Part 2Document23 pagesPart 2Silvia SlavkovaNo ratings yet

- Multinational Financial Management Exchange RatesDocument21 pagesMultinational Financial Management Exchange RatesShahbaz QureshiNo ratings yet

- International Financial Management VillafloresDocument36 pagesInternational Financial Management VillafloresSebastian M.VNo ratings yet

- Foreign Exchange Basics TheoryDocument16 pagesForeign Exchange Basics TheoryKaran AggarwalNo ratings yet

- 70-398 International Finance SPRING 2023: Prof. Serkan AkgucDocument29 pages70-398 International Finance SPRING 2023: Prof. Serkan AkgucAmiko GogitidzeNo ratings yet

- Foreign Exchange Markets - Lecture SlidesDocument25 pagesForeign Exchange Markets - Lecture SlidesmaddNo ratings yet

- Treasury Fund Management GuideDocument64 pagesTreasury Fund Management GuidemankeraNo ratings yet

- CH 11 - International Finance - NurhaiyyuDocument62 pagesCH 11 - International Finance - NurhaiyyukkNo ratings yet

- Leture # 3Document17 pagesLeture # 3Muhammad Haris KhanNo ratings yet

- L10 Open EconomyDocument43 pagesL10 Open EconomyYaswanth Kumar MaddaliNo ratings yet

- L4 International Arbitrage and IRPDocument25 pagesL4 International Arbitrage and IRPKent ChinNo ratings yet

- Exchange Rates and The Foreign Exchange Market: An Asset ApproachDocument44 pagesExchange Rates and The Foreign Exchange Market: An Asset ApproachJohanne Rhielle OpridoNo ratings yet

- Exchange Rates, Business Cycles, and Macroeconomic Policy in The Open EconomyDocument25 pagesExchange Rates, Business Cycles, and Macroeconomic Policy in The Open EconomyYuresh NadishanNo ratings yet

- PPT-4 Parity Conditions and Currency ForecastingDocument42 pagesPPT-4 Parity Conditions and Currency ForecastingKamal KantNo ratings yet

- Introduction To Market RiskDocument140 pagesIntroduction To Market RiskSaurabhNo ratings yet

- Session 15Document23 pagesSession 15Sid Tushaar SiddharthNo ratings yet

- Foreign Exchange Markets ExplainedDocument65 pagesForeign Exchange Markets ExplainedNimish PandeNo ratings yet

- Session 14-15-16Document39 pagesSession 14-15-16Digvijay SinghNo ratings yet

- What is International Financial ManagementDocument94 pagesWhat is International Financial ManagementHarendra Singh BhadauriaNo ratings yet

- Unit SDocument42 pagesUnit Ssprayzza tvNo ratings yet

- Raising CapitalDocument64 pagesRaising CapitalgagafikNo ratings yet

- Return, Risk, and The Security Market LineDocument37 pagesReturn, Risk, and The Security Market LinegagafikNo ratings yet

- Cash and Liquidity ManagementDocument27 pagesCash and Liquidity ManagementgagafikNo ratings yet

- Credit and Inventory ManagementDocument32 pagesCredit and Inventory ManagementgagafikNo ratings yet

- Options and Corporate FinanceDocument26 pagesOptions and Corporate FinancegagafikNo ratings yet

- CH09Document26 pagesCH09devinaNo ratings yet

- Long-Term Financial Planning and Growth: Mcgraw-Hill/IrwinDocument36 pagesLong-Term Financial Planning and Growth: Mcgraw-Hill/IrwindevinaNo ratings yet

- Introduction To Valuation: The Time Value of MoneyDocument34 pagesIntroduction To Valuation: The Time Value of MoneyAlfina AfiiNo ratings yet

- Cost of CapitalDocument35 pagesCost of CapitalgagafikNo ratings yet

- Capital Budgeting 1Document42 pagesCapital Budgeting 1Rych Bucks100% (1)

- Financial Statements, Taxes, and Cash FlowDocument46 pagesFinancial Statements, Taxes, and Cash FlowgagafikNo ratings yet

- CH11Document32 pagesCH11devinaNo ratings yet

- Dutch Flower Cluster v2Document9 pagesDutch Flower Cluster v2gagafikNo ratings yet

- Working With Financial StatementsDocument32 pagesWorking With Financial StatementsgagafikNo ratings yet

- Indonesia Case ECON OF COMPTDocument2 pagesIndonesia Case ECON OF COMPTgagafikNo ratings yet

- Competitividad Internacional AD-6010: CaseDocument3 pagesCompetitividad Internacional AD-6010: CasegagafikNo ratings yet

- Analyzing The Economic Situation in Cot D'ivoire, It Is Developing Country With IncreasingDocument1 pageAnalyzing The Economic Situation in Cot D'ivoire, It Is Developing Country With IncreasinggagafikNo ratings yet

- De Beers and NestleDocument4 pagesDe Beers and NestlegagafikNo ratings yet

- Dutch Flower and IcelandDocument5 pagesDutch Flower and IcelandgagafikNo ratings yet

- Basque and NYDocument3 pagesBasque and NYgagafikNo ratings yet

- Questions AnswersDocument13 pagesQuestions Answersgagafik100% (1)

- Tsis Analysis of Namibia EconomicsDocument7 pagesTsis Analysis of Namibia EconomicsgagafikNo ratings yet

- The Dutch Flower Cluster ReportDocument18 pagesThe Dutch Flower Cluster ReportgagafikNo ratings yet

- Tsis Analysis of Cot D'ivoire Economics: Department of Economics and Management Principle of EconomicsDocument3 pagesTsis Analysis of Cot D'ivoire Economics: Department of Economics and Management Principle of EconomicsgagafikNo ratings yet

- Econometrics Final PreparationDocument9 pagesEconometrics Final PreparationgagafikNo ratings yet

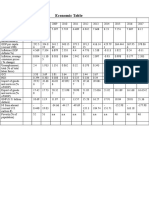

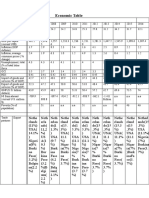

- Economic Table NigerDocument1 pageEconomic Table NigergagafikNo ratings yet

- CADocument2 pagesCAgagafikNo ratings yet

- EconDocument2 pagesEcongagafikNo ratings yet

- Abhishek Laddha ViewsDocument13 pagesAbhishek Laddha ViewsabhishekNo ratings yet

- CG Extra SumsDocument19 pagesCG Extra SumsPruthil Monpariya0% (1)

- Manila University corporate finance midterm exam ratiosDocument3 pagesManila University corporate finance midterm exam ratiosUnivMan LawNo ratings yet

- Azerbaijan Oil Company 2017 IFRS ReportsDocument96 pagesAzerbaijan Oil Company 2017 IFRS ReportsMehemmed MemmedliNo ratings yet

- Chapter 5 Consolidated Financial Statements of Group Companies PDFDocument103 pagesChapter 5 Consolidated Financial Statements of Group Companies PDFSamson SeiduNo ratings yet

- Accounting Textbook Solutions - 66Document19 pagesAccounting Textbook Solutions - 66acc-expertNo ratings yet

- ENV Envestnet Investor Presentation Draft 2018-01-09Document25 pagesENV Envestnet Investor Presentation Draft 2018-01-09Ala BasterNo ratings yet

- Goldman Sachs Acts as Bookrunner for $681M Hepsiburada IPODocument1 pageGoldman Sachs Acts as Bookrunner for $681M Hepsiburada IPOFERRONo ratings yet

- International Financial Management 1Document7 pagesInternational Financial Management 1Kundan KarnNo ratings yet

- Financial Statements and RatiosDocument27 pagesFinancial Statements and RatiosIoana MariucaNo ratings yet

- FSA Chapter 7Document3 pagesFSA Chapter 7Nadia ZahraNo ratings yet

- Capital Market Review and Outlook: AnnualDocument20 pagesCapital Market Review and Outlook: AnnualbigaNo ratings yet

- Ethiopia's Banking Sector Performance and OutlookDocument41 pagesEthiopia's Banking Sector Performance and OutlookAsniNo ratings yet

- AFFLE - Investor Presentation - 14-May-23 - TickertapeDocument30 pagesAFFLE - Investor Presentation - 14-May-23 - Tickertapeayush tandonNo ratings yet

- Part 1Document5 pagesPart 1Lanurias, Gabriel Dylan S.No ratings yet

- Buisness 12th Part-2Document142 pagesBuisness 12th Part-2online onlineNo ratings yet

- Ezz Steel, Al Ezz Steel Com..Document2 pagesEzz Steel, Al Ezz Steel Com..شادى احمدNo ratings yet

- Dividend PolicyDocument16 pagesDividend PolicyDương Thuỳ TrangNo ratings yet

- 2018 ZB PaperDocument9 pages2018 ZB Papermandy YiuNo ratings yet

- Investment Analysis - ICICIDocument17 pagesInvestment Analysis - ICICISudeep ChinnabathiniNo ratings yet

- P1.T3. Financial Markets & Products Chapter 1 - Banks Bionic Turtle FRM Study NotesDocument22 pagesP1.T3. Financial Markets & Products Chapter 1 - Banks Bionic Turtle FRM Study NotesChristian Rey MagtibayNo ratings yet

- SkyWorld - Redacted Prospectus (Full) - 20221202 PDFDocument579 pagesSkyWorld - Redacted Prospectus (Full) - 20221202 PDFOliver OscarNo ratings yet

- Bullish EngulfingDocument2 pagesBullish EngulfingHammad SaeediNo ratings yet

- Assignment 01 FMDocument8 pagesAssignment 01 FMChinky JaiswalNo ratings yet

- Merger of Centurion Bank of Punjab & HDFCDocument23 pagesMerger of Centurion Bank of Punjab & HDFCAshish Kotian100% (2)

- Entrep W6Document1 pageEntrep W6claudineNo ratings yet

- Chapter 3. Derivatives NewDocument9 pagesChapter 3. Derivatives NewTrúc Vũ Thụy ThanhNo ratings yet

- Thomas Rowe Price Investment PhilosophyDocument4 pagesThomas Rowe Price Investment PhilosophyKaran Uppal100% (1)

- Closprice Date - 21-03-2023Document1 pageClosprice Date - 21-03-2023sanjay sharmaNo ratings yet

- A Study On Changing Investment Pattern Among Youth: G.H.Patel Post Graduate Institute of Business ManagementDocument50 pagesA Study On Changing Investment Pattern Among Youth: G.H.Patel Post Graduate Institute of Business ManagementNaveen SahaNo ratings yet