You might also like

- The Basel Ii "Use Test" - a Retail Credit Approach: Developing and Implementing Effective Retail Credit Risk Strategies Using Basel IiFrom EverandThe Basel Ii "Use Test" - a Retail Credit Approach: Developing and Implementing Effective Retail Credit Risk Strategies Using Basel IiNo ratings yet

- The New Project Management: Tools for an Age of Rapid Change, Complexity, and Other Business RealitiesFrom EverandThe New Project Management: Tools for an Age of Rapid Change, Complexity, and Other Business RealitiesNo ratings yet

- Basel NormsDocument42 pagesBasel NormsBluehacksNo ratings yet

- Basel II Compliance Solution FrameworkDocument12 pagesBasel II Compliance Solution Frameworkamol2982No ratings yet

- Basel II Compliance Solution Framework OverviewDocument12 pagesBasel II Compliance Solution Framework OverviewgirrajmeenaNo ratings yet

- Credit RatingDocument3 pagesCredit Ratingsanjay parmar100% (4)

- Special Issues in Indian Banking Sector ReportDocument78 pagesSpecial Issues in Indian Banking Sector ReportAli AttarwalaNo ratings yet

- Basel II Capital Accord SlidesDocument25 pagesBasel II Capital Accord SlidesAamir RazaNo ratings yet

- Revised CF Webcast Slides April 2018Document16 pagesRevised CF Webcast Slides April 2018drew aranasNo ratings yet

- Audit of BanksDocument6 pagesAudit of BanksLyka M. ManalotoNo ratings yet

- Lecture Notes 1 - Corporate Finance Corporate GovernanceDocument32 pagesLecture Notes 1 - Corporate Finance Corporate GovernanceLucas VignaudNo ratings yet

- Receivables Management: "Any Fool Can Lend Money, ButDocument14 pagesReceivables Management: "Any Fool Can Lend Money, ButmanpreetklerNo ratings yet

- BaselDocument38 pagesBaselsourabhs90No ratings yet

- Finman PrelimDocument16 pagesFinman PrelimAngelyn AmadorNo ratings yet

- Digital Banking An Regulatry ComplianceDocument23 pagesDigital Banking An Regulatry Compliancesathyanandaprabhu2786No ratings yet

- Reimagined Policy - PL and BILDocument39 pagesReimagined Policy - PL and BILarshidahmadNo ratings yet

- Chap 20Document7 pagesChap 20v lNo ratings yet

- Risk Based Internal Audit - Need, Implementation & Key ElementsDocument28 pagesRisk Based Internal Audit - Need, Implementation & Key ElementsnitinNo ratings yet

- Borrelli Walsh - 20191111 - Due Diligence For Emerging Markets What WorksDocument3 pagesBorrelli Walsh - 20191111 - Due Diligence For Emerging Markets What WorksImroni PisesaNo ratings yet

- Presented By: Arpita Gupta Disha Sogani Priyamvada Romi SharmaDocument17 pagesPresented By: Arpita Gupta Disha Sogani Priyamvada Romi SharmaPriyamvada ShekhawatNo ratings yet

- Presentation By: Yogieta S. Mehra: in Light ofDocument37 pagesPresentation By: Yogieta S. Mehra: in Light ofyogietaNo ratings yet

- Lecture 1 Banking, Financial Services Industry and RegulationsDocument29 pagesLecture 1 Banking, Financial Services Industry and Regulationseugene etwireNo ratings yet

- Institute - Usb Department - BbaDocument20 pagesInstitute - Usb Department - BbaAmanNo ratings yet

- Macrib Group 9&10Document7 pagesMacrib Group 9&10Anurag PatelNo ratings yet

- Leading With Finance SyllabusDocument2 pagesLeading With Finance SyllabusJyxiongJuevaxaikiNo ratings yet

- Updated Slides introducing the conceptual framework (1)Document24 pagesUpdated Slides introducing the conceptual framework (1)Hunal Kumar MautadinNo ratings yet

- Credit Rating: Dr. Kanhaiya SinghDocument30 pagesCredit Rating: Dr. Kanhaiya SinghVidisha SinghalNo ratings yet

- Corporate Banking Lending Processes and RegulationsDocument58 pagesCorporate Banking Lending Processes and RegulationsSuraj KumarNo ratings yet

- 1424 Receivables ManagementDocument13 pages1424 Receivables ManagementBhavika_Patel_8085No ratings yet

- Receivables ManagementDocument37 pagesReceivables Managementchanky_kool8782% (11)

- Chapter 1Document49 pagesChapter 1Sami JattNo ratings yet

- DELOITTE-ch-fa-managing-business-continuity-finance-covid-19 SUMMARYDocument7 pagesDELOITTE-ch-fa-managing-business-continuity-finance-covid-19 SUMMARYReza HaryoNo ratings yet

- Receivables Management TechniquesDocument37 pagesReceivables Management Techniquesjai262418No ratings yet

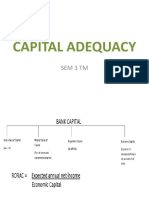

- Capital Adequacy: Prof. B.B.BhattacharyyaDocument115 pagesCapital Adequacy: Prof. B.B.BhattacharyyaSheetal IyerNo ratings yet

- Chapter 2: The Conceptual Framework: Fundamentals of Intermediate Accounting Weygandt, Kieso, and WarfieldDocument36 pagesChapter 2: The Conceptual Framework: Fundamentals of Intermediate Accounting Weygandt, Kieso, and WarfieldMohammed Akhtab Ul HudaNo ratings yet

- Corporate Governance: Stakeholders, Management, and PurposeDocument18 pagesCorporate Governance: Stakeholders, Management, and PurposeUnnamed homosapienNo ratings yet

- Capital Adequacy: Sem 3 TMDocument45 pagesCapital Adequacy: Sem 3 TMahsan habibNo ratings yet

- Credit Analysis and Distress PredictionDocument57 pagesCredit Analysis and Distress Predictionrizki nurNo ratings yet

- NpaDocument19 pagesNpasayantanpatra100% (1)

- CARE's Issuer Rating: 1. ScopeDocument7 pagesCARE's Issuer Rating: 1. ScopeSuryaNo ratings yet

- Implement risk management, obtain banking license, develop new productsDocument1 pageImplement risk management, obtain banking license, develop new productsVenkatesh Krishna KumarNo ratings yet

- Syllabus Leading With Finance PDFDocument1 pageSyllabus Leading With Finance PDFTanmoy GhoraiNo ratings yet

- Harvard Business School PDFDocument1 pageHarvard Business School PDFNIKUNJ JAINNo ratings yet

- Credit MonitoringDocument166 pagesCredit Monitoringjananidhanasekaran26No ratings yet

- Receivables ManagementDocument13 pagesReceivables ManagementjayantbhatnagarNo ratings yet

- Conceptual FrameworkDocument13 pagesConceptual FrameworkKate Louie RamasNo ratings yet

- Basel II PresentationDocument21 pagesBasel II PresentationMuhammad SaqibNo ratings yet

- Credit Risk Part I RMBKDocument52 pagesCredit Risk Part I RMBKGourav BaidNo ratings yet

- Risk Based Internal Audit TrainingDocument4 pagesRisk Based Internal Audit TrainingaNo ratings yet

- Strategic Finance Management ppt1Document17 pagesStrategic Finance Management ppt1Ram P100% (1)

- Topic 5-Financial SupervisionDocument43 pagesTopic 5-Financial Supervisionmerlinda ratuNo ratings yet

- L4-Organizational Structure of BanksDocument26 pagesL4-Organizational Structure of BanksShameel IrshadNo ratings yet

- Basel II - Understanding the International FrameworkDocument57 pagesBasel II - Understanding the International FrameworkskartyknNo ratings yet

- Risk Management in BanksDocument32 pagesRisk Management in Banksanon_595315274100% (1)

- Forex & Treasury Management: Regulatory RiskDocument15 pagesForex & Treasury Management: Regulatory RiskGaurav BhandariNo ratings yet

- Chapter 2: The Conceptual FrameworkDocument36 pagesChapter 2: The Conceptual FrameworkNida Mohammad Khan AchakzaiNo ratings yet

- CSI Black Belt in Credit Risk Management - Financial Analysis Master Class (Singapore), Featuring Mr. TOMMY SEAHDocument4 pagesCSI Black Belt in Credit Risk Management - Financial Analysis Master Class (Singapore), Featuring Mr. TOMMY SEAHCFE International Consultancy GroupNo ratings yet

- Impact and Recommendations For Credit Risk ManagementDocument13 pagesImpact and Recommendations For Credit Risk ManagementRoberto TuestaNo ratings yet

- India's Growing E-Waste ProblemDocument12 pagesIndia's Growing E-Waste ProblemLavesh_Bhandar_4987No ratings yet

- Chhattisgarh 04092012Document55 pagesChhattisgarh 04092012Sneha BhorawatNo ratings yet

- 7 Tool of TQMDocument69 pages7 Tool of TQMMuhammad Ali AkbarNo ratings yet

- Retailvertical 1232693541890021 3Document24 pagesRetailvertical 1232693541890021 3Sneha BhorawatNo ratings yet

- Cadbury LiteDocument28 pagesCadbury LiteSneha BhorawatNo ratings yet

- Hindalco Through The Lens of Michael PorterDocument8 pagesHindalco Through The Lens of Michael PorterSneha BhorawatNo ratings yet

- 7 Tool of TQMDocument69 pages7 Tool of TQMMuhammad Ali AkbarNo ratings yet

- America's Health Insurance Plans PAC (AHIP) - 8227 - VSRDocument2 pagesAmerica's Health Insurance Plans PAC (AHIP) - 8227 - VSRZach EdwardsNo ratings yet

- Building Code PDFDocument11 pagesBuilding Code PDFUmrotus SyadiyahNo ratings yet

- FCRA Renewal CertificateDocument2 pagesFCRA Renewal CertificateBrukshya o Jeevar Bandhu ParisadNo ratings yet

- Balibago Faith Baptist Church V Faith in Christ Jesus Baptist ChurchDocument13 pagesBalibago Faith Baptist Church V Faith in Christ Jesus Baptist ChurchRelmie TaasanNo ratings yet

- Bank Officer's Handbook of Commercial Banking Law 5thDocument363 pagesBank Officer's Handbook of Commercial Banking Law 5thCody Morgan100% (5)

- Honeywell Acumist Micronized Additives Wood Coatings Overview PDFDocument2 pagesHoneywell Acumist Micronized Additives Wood Coatings Overview PDFBbaPbaNo ratings yet

- Factoring FSDocument13 pagesFactoring FSAvinaw KumarNo ratings yet

- Study of Non Performing Assets in Bank of Maharashtra.Document74 pagesStudy of Non Performing Assets in Bank of Maharashtra.Arun Savukar60% (10)

- Bioavailabilitas & BioekivalenDocument27 pagesBioavailabilitas & Bioekivalendonghaesayangela100% (1)

- Audit of ContractsDocument26 pagesAudit of ContractsSarvesh Khatnani100% (1)

- High Commission of India: Visa Application FormDocument2 pagesHigh Commission of India: Visa Application FormShuhan Mohammad Ariful HoqueNo ratings yet

- Tacas Vs Tobon (SC)Document7 pagesTacas Vs Tobon (SC)HenteLAWcoNo ratings yet

- Black Farmers in America, 1865-2000 The Pursuit of in Dependant Farming and The Role of CooperativesDocument28 pagesBlack Farmers in America, 1865-2000 The Pursuit of in Dependant Farming and The Role of CooperativesBrian Scott Williams100% (1)

- 2020 Dee - v. - Dee Reyes20210424 14 mjb83kDocument4 pages2020 Dee - v. - Dee Reyes20210424 14 mjb83kLynielle CrisologoNo ratings yet

- Online Tax Payment PortalDocument1 pageOnline Tax Payment Portalashish rathoreNo ratings yet

- Eltek FP2 IndoorDocument1 pageEltek FP2 IndoorDmiNo ratings yet

- Characteristics of SovereigntyDocument9 pagesCharacteristics of SovereigntyVera Mae RigorNo ratings yet

- Ato v. Ramos CDDocument2 pagesAto v. Ramos CDKaren AmpeloquioNo ratings yet

- Authum Infra - PPTDocument191 pagesAuthum Infra - PPTmisfitmedicoNo ratings yet

- Joanne Mae VDocument5 pagesJoanne Mae VAndrea Denise VillafuerteNo ratings yet

- Deed of Donation for Farm to Market Road ROWDocument2 pagesDeed of Donation for Farm to Market Road ROWAntonio Del Rosario100% (1)

- HHRG 118 IF00 Wstate ChewS 20230323Document10 pagesHHRG 118 IF00 Wstate ChewS 20230323Jillian SmithNo ratings yet

- Evidence Drop: Hawaii DOH Apparently Gave Obama Stig Waidelich's Birth Certificate Number - 3/27/2013Document62 pagesEvidence Drop: Hawaii DOH Apparently Gave Obama Stig Waidelich's Birth Certificate Number - 3/27/2013ObamaRelease YourRecords100% (3)

- Early Education of Rizal UsitaDocument13 pagesEarly Education of Rizal Usitajuriel velascoNo ratings yet

- Solomon Islands School Certificate 2007 New Testament Studies Question BookletDocument14 pagesSolomon Islands School Certificate 2007 New Testament Studies Question BookletAndrew ArahaNo ratings yet

- Akun-Akun Queen ToysDocument4 pagesAkun-Akun Queen ToysAnggita Kharisma MaharaniNo ratings yet

- Iem GM Form PDFDocument2 pagesIem GM Form PDFAbdul KarimNo ratings yet

- Thesis Property ManagementDocument7 pagesThesis Property Managementfjnsf5yf100% (2)

- Consti II Cases Section 1Document283 pagesConsti II Cases Section 1kybee1988No ratings yet

- StaRo Special Steel Items and Surplus StockDocument2 pagesStaRo Special Steel Items and Surplus StockmelainiNo ratings yet