You might also like

- Forecasting ProblemsDocument7 pagesForecasting ProblemsJoel Pangisban0% (3)

- Comparative Income Statements and Balance Sheets For Merck ($ Millions) FollowDocument6 pagesComparative Income Statements and Balance Sheets For Merck ($ Millions) FollowIman naufalNo ratings yet

- Mayes 8e CH05 SolutionsDocument36 pagesMayes 8e CH05 SolutionsRamez AhmedNo ratings yet

- BSBFIM601 Manage FinancesDocument34 pagesBSBFIM601 Manage Financesneha0% (1)

- 7 11 Capital ManagementDocument6 pages7 11 Capital ManagementRonaldo ConventoNo ratings yet

- I. Financial AssumptionsDocument14 pagesI. Financial AssumptionsJaera shopaholicNo ratings yet

- Budget Artikel ExcelDocument8 pagesBudget Artikel ExcelnugrahaNo ratings yet

- Budget PT Abcd Balance Sheet Projection of Year 2017Document8 pagesBudget PT Abcd Balance Sheet Projection of Year 2017Abdul SyukurNo ratings yet

- FINM 7044 Group Assignment 终Document4 pagesFINM 7044 Group Assignment 终jimmmmNo ratings yet

- Acc 291 Acc 291 Acc 291 Acc 291 Acc 291 Acc 291Document201 pagesAcc 291 Acc 291 Acc 291 Acc 291 Acc 291 Acc 291290acc100% (2)

- DU Pont AnalysisDocument9 pagesDU Pont Analysisshani2010No ratings yet

- Name-Ishwor Rijal LBU I'd - 77271300 Subject - Corporate FinanceDocument10 pagesName-Ishwor Rijal LBU I'd - 77271300 Subject - Corporate FinanceIshwor RijalNo ratings yet

- NIKL PR Aug 07 2020Document5 pagesNIKL PR Aug 07 2020Peter Paul RecaboNo ratings yet

- Current Assets: See Accompanying Notes To Financial StatementsDocument5 pagesCurrent Assets: See Accompanying Notes To Financial StatementsAlicia NhsNo ratings yet

- Assignment 2 - Strategic Financial Management - Abdulhakeem MustafaDocument7 pagesAssignment 2 - Strategic Financial Management - Abdulhakeem MustafaHakeem SnrNo ratings yet

- Chapter 6 PDFDocument23 pagesChapter 6 PDFreyNo ratings yet

- Comprehensive Income (2017-2018)Document12 pagesComprehensive Income (2017-2018)Lee SuarezNo ratings yet

- Gita AgricultureDocument20 pagesGita AgriculturemrigendrarimalNo ratings yet

- 2-Annex A Cpfi Afs ConsoDocument97 pages2-Annex A Cpfi Afs ConsoCynthia PenoliarNo ratings yet

- Aspin Kemp - Associates Holding Corp. Consolidated FS 2017 PDFDocument25 pagesAspin Kemp - Associates Holding Corp. Consolidated FS 2017 PDFAnonymous nVXCkl0ANo ratings yet

- PBCC ActivitiesDocument25 pagesPBCC ActivitiesykwaiNo ratings yet

- WAPO 2019 Final Draft XXXDocument229 pagesWAPO 2019 Final Draft XXXRenatus shijaNo ratings yet

- Practice Solution 2Document4 pagesPractice Solution 2Luigi NocitaNo ratings yet

- Seven Up Bottling Co PLC: For The Ended 31 March, 2014Document4 pagesSeven Up Bottling Co PLC: For The Ended 31 March, 2014Gina FelyaNo ratings yet

- Fm-Nov-Dec 2012Document14 pagesFm-Nov-Dec 2012banglauserNo ratings yet

- Directors' Report: For The Period Ended 31 March 2018Document24 pagesDirectors' Report: For The Period Ended 31 March 2018Asma RehmanNo ratings yet

- Sir Sarwar AFSDocument41 pagesSir Sarwar AFSawaischeemaNo ratings yet

- English Q3 2018 Financials For Galfar WebsiteDocument24 pagesEnglish Q3 2018 Financials For Galfar WebsiteMOORTHYNo ratings yet

- Discounted Cash FlowDocument9 pagesDiscounted Cash FlowAditya JandialNo ratings yet

- 4.1-Hortizontal/Trends Analysis: Chapter No # 4Document32 pages4.1-Hortizontal/Trends Analysis: Chapter No # 4Sadi ShahzadiNo ratings yet

- 5 6120493211875018431Document62 pages5 6120493211875018431Hafsah Amod DisomangcopNo ratings yet

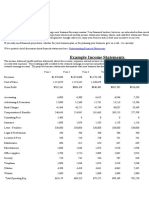

- Example Income Statements: Business Plan Financial ProjectionsDocument3 pagesExample Income Statements: Business Plan Financial ProjectionsSUMANTO SHARANNo ratings yet

- Submitted By: Syeda Fatima Usman (65236) HUNAIN IMRAN (65368) HANIYA BATOOL (65282) Huraibah Batool (65283)Document24 pagesSubmitted By: Syeda Fatima Usman (65236) HUNAIN IMRAN (65368) HANIYA BATOOL (65282) Huraibah Batool (65283)Syeda Fatima UsmanNo ratings yet

- Institute of Management Development and Research (Imdr) : Pune Post Graduation Diploma in Management (PGDM)Document9 pagesInstitute of Management Development and Research (Imdr) : Pune Post Graduation Diploma in Management (PGDM)hitesh rathodNo ratings yet

- Case 9Document11 pagesCase 9Nguyễn Thanh PhongNo ratings yet

- Donam Corporate FinanceDocument9 pagesDonam Corporate FinanceMAGOMU DAN DAVIDNo ratings yet

- Chapter-5 Analysis of Financial Statement: Statement of Profit & Loss Account For The Year Ended 31 MarchDocument5 pagesChapter-5 Analysis of Financial Statement: Statement of Profit & Loss Account For The Year Ended 31 MarchAcchu RNo ratings yet

- Cash Flow StatementDocument19 pagesCash Flow Statementasherjoe67% (3)

- Tugas Personal 1 FINC6193Document9 pagesTugas Personal 1 FINC6193alif syahputra11No ratings yet

- 2017 DoubleDragon Properties Corp and SubsidiariesDocument86 pages2017 DoubleDragon Properties Corp and Subsidiariesbackup cmbmpNo ratings yet

- Tesla Inc Unsolved Model 330PMDocument61 pagesTesla Inc Unsolved Model 330PMAYUSH SHARMANo ratings yet

- UploadDocument83 pagesUploadAli BMSNo ratings yet

- 025the Final Print NaaaDocument63 pages025the Final Print NaaaRhealyn Cabel CapalaranNo ratings yet

- Project Report: RIDA SHEIKH (61573) WAQAR MASNOOR (62790) ALI ABDULLAH (61112) MUHAMMAD ALI (61251)Document15 pagesProject Report: RIDA SHEIKH (61573) WAQAR MASNOOR (62790) ALI ABDULLAH (61112) MUHAMMAD ALI (61251)rida sheikhNo ratings yet

- Cash Flow From Assets - Solution PDFDocument3 pagesCash Flow From Assets - Solution PDFSeptian Sugestyo PutroNo ratings yet

- FMIBDocument10 pagesFMIBVu Ngoc QuyNo ratings yet

- 1) Basic of Cost ControlDocument38 pages1) Basic of Cost ControlYuda Setiawan100% (1)

- What A ProblemDocument4 pagesWhat A ProblemEleazar SalazarNo ratings yet

- Topic 10-12 Alk (Hitungannya)Document6 pagesTopic 10-12 Alk (Hitungannya)Daffa Permana PutraNo ratings yet

- National Foods Balance Sheet: 2013 2014 Assets Non-Current AssetsDocument8 pagesNational Foods Balance Sheet: 2013 2014 Assets Non-Current Assetsbakhoo12No ratings yet

- Nuru Ethiopia Final Audit Report 2019Document22 pagesNuru Ethiopia Final Audit Report 2019Elias Abubeker AhmedNo ratings yet

- Investments Profitability AnalysisDocument53 pagesInvestments Profitability AnalysisAidan MacasaNo ratings yet

- ABS CBN CorporationDocument16 pagesABS CBN CorporationAlyssa BeatriceNo ratings yet

- FM Unit 2 Tutorial - Finanacial Statement Analysis Revised 2019Document4 pagesFM Unit 2 Tutorial - Finanacial Statement Analysis Revised 2019Tanice WhyteNo ratings yet

- Data Case 8Document31 pagesData Case 8milagrosNo ratings yet

- Case 14 ExcelDocument8 pagesCase 14 ExcelRabeya AktarNo ratings yet

- Financial Statements Analysis: Arsalan FarooqueDocument31 pagesFinancial Statements Analysis: Arsalan FarooqueMuhib NoharioNo ratings yet

- 2016 Management AccountsDocument6 pages2016 Management AccountsJcaldas AponteNo ratings yet

- Week 4Document9 pagesWeek 4kishorbombe.unofficialNo ratings yet

- Principles of Cash Flow Valuation: An Integrated Market-Based ApproachFrom EverandPrinciples of Cash Flow Valuation: An Integrated Market-Based ApproachRating: 3 out of 5 stars3/5 (3)

- A Primer On The AhtnDocument4 pagesA Primer On The AhtnRonie SugarolNo ratings yet

- Introduction To Globalization: Presented By: CB Ronie E. Sugarol, MPBMDocument10 pagesIntroduction To Globalization: Presented By: CB Ronie E. Sugarol, MPBMRonie SugarolNo ratings yet

- Writing Letters Writing Memos and Writing Short and Long ReportsDocument17 pagesWriting Letters Writing Memos and Writing Short and Long ReportsRonie SugarolNo ratings yet

- 4 RsDocument22 pages4 RsRonie SugarolNo ratings yet

- HOD Assignment 1Document19 pagesHOD Assignment 1KUMARAGURU PONRAJNo ratings yet

- Creating FSG ReportsDocument36 pagesCreating FSG Reportsashimamal100% (1)

- Statement of Cash Flows-International Accounting Standard (IAS) 7Document18 pagesStatement of Cash Flows-International Accounting Standard (IAS) 7Adenrele Salako100% (1)

- Adh Newipo IpoDocument759 pagesAdh Newipo IpoSathishKumarNo ratings yet

- Analysis of Financial StatementsDocument37 pagesAnalysis of Financial StatementsApollo Institute of Hospital Administration100% (5)

- Module 4 - Financial Instruments (Assets)Document9 pagesModule 4 - Financial Instruments (Assets)Luisito CorreaNo ratings yet

- MIDTERM EXAM - Mahardika Ayunda C1I019034 AKMDocument12 pagesMIDTERM EXAM - Mahardika Ayunda C1I019034 AKMMahardika AyundaNo ratings yet

- Ch1 4e - Acc in Action 2021Document50 pagesCh1 4e - Acc in Action 2021K59 Vu Thi Thu HienNo ratings yet

- Buscom ExcelDocument18 pagesBuscom ExceldmangiginNo ratings yet

- Group 4 YemochiDocument22 pagesGroup 4 YemochiJane GawadNo ratings yet

- Business: Pearson Edexcel International GCSEDocument15 pagesBusiness: Pearson Edexcel International GCSEHan Thi Win KoNo ratings yet

- Project On Sun PharmaDocument77 pagesProject On Sun PharmaNivedha MNo ratings yet

- Importance of Final AccountsDocument5 pagesImportance of Final AccountsShradha KapseNo ratings yet

- Final Accounts ProblemDocument21 pagesFinal Accounts Problemkramit1680% (10)

- QS12 - Midterm 2 Review SolutionDocument7 pagesQS12 - Midterm 2 Review Solutionlyk0tex0% (1)

- Controlling: Source: Management - A Global Perspective by Weihrich and Koontz 11 EditionDocument26 pagesControlling: Source: Management - A Global Perspective by Weihrich and Koontz 11 EditionMaritoni MercadoNo ratings yet

- Financial AccountingDocument4 pagesFinancial Accountingdracula nagrajNo ratings yet

- Investment Property: Investment Property Is Defined As Property (Land or Building or Part of A Building or Both) HeldDocument7 pagesInvestment Property: Investment Property Is Defined As Property (Land or Building or Part of A Building or Both) HeldMark Anthony SivaNo ratings yet

- Microsoft Word - Chapter 1Document4 pagesMicrosoft Word - Chapter 1SoblessedNo ratings yet

- Week 1 - Lesson 1 Overview of AccountingDocument10 pagesWeek 1 - Lesson 1 Overview of AccountingRose RaboNo ratings yet

- Chapter 13 - Multiple Choices Problem and Theries KeyDocument15 pagesChapter 13 - Multiple Choices Problem and Theries KeyKryscel ManansalaNo ratings yet

- Mads Rialubin Travel Agency WORKSHEET FS TRIAL BALANCEDocument3 pagesMads Rialubin Travel Agency WORKSHEET FS TRIAL BALANCEJowe Ringor Casignia100% (1)

- Quiz 2 - 4B UpdatesDocument3 pagesQuiz 2 - 4B UpdatesAngelo HilomaNo ratings yet

- Baker ElectronicsDocument1 pageBaker ElectronicsleicatapangNo ratings yet

- Break Even Analysis TR TCDocument10 pagesBreak Even Analysis TR TCSudhir KashyapNo ratings yet

- Financial Analysis and Planning: Cash Flow and Fund Flow Statement Are Not There in SyllabusDocument29 pagesFinancial Analysis and Planning: Cash Flow and Fund Flow Statement Are Not There in SyllabusHanabusa Kawaii IdouNo ratings yet

- Chapter 5Document44 pagesChapter 5chanreaksmeytepNo ratings yet

- Chapter 23 - Gripping IFRS ICAP 2008 (Solution of Graded Questions)Document29 pagesChapter 23 - Gripping IFRS ICAP 2008 (Solution of Graded Questions)Falah Ud Din SheryarNo ratings yet

- Online Lecutre 1Document21 pagesOnline Lecutre 1Dinar HassanNo ratings yet

- FA 2 Chapter 11 Manufacturing AccountsDocument20 pagesFA 2 Chapter 11 Manufacturing AccountsMhd AminNo ratings yet