You might also like

- Financial Ratio Analysis of Heartland IncDocument8 pagesFinancial Ratio Analysis of Heartland IncARCHIT KUMARNo ratings yet

- Topic 13 Financial Statement AnalysisDocument32 pagesTopic 13 Financial Statement AnalysisAbd AL Rahman Shah Bin Azlan ShahNo ratings yet

- Debt Service Coverage RatioDocument7 pagesDebt Service Coverage RatioAamir BilalNo ratings yet

- Analysis of Financial StatementsDocument19 pagesAnalysis of Financial StatementsGautam MNo ratings yet

- 3.financial Statement AnylasisDocument20 pages3.financial Statement AnylasisTadasha MishraNo ratings yet

- Financial Statement Ratio AnalysisDocument14 pagesFinancial Statement Ratio Analysissunil0507100% (1)

- Debt RatioDocument7 pagesDebt RatioAamir BilalNo ratings yet

- SL No Description A Liquidity RatiosDocument10 pagesSL No Description A Liquidity RatiosAshish SharmaNo ratings yet

- Classification of Ratios Type Standard Norm For Investors For Company Profitability RATIOS: (Expressed in %)Document12 pagesClassification of Ratios Type Standard Norm For Investors For Company Profitability RATIOS: (Expressed in %)parivesh16No ratings yet

- Ratio Analysis:: Liquidity Measurement RatiosDocument8 pagesRatio Analysis:: Liquidity Measurement RatiossammitNo ratings yet

- Financial Ratio Analysis BreakdownDocument13 pagesFinancial Ratio Analysis BreakdownA.Rahman SalahNo ratings yet

- Chapter 3Document61 pagesChapter 3Shrief MohiNo ratings yet

- Financial Analysis RatiosDocument34 pagesFinancial Analysis Ratioskrishna priyaNo ratings yet

- Chartered AccountantDocument24 pagesChartered AccountantanirudhanoliNo ratings yet

- Chapter 3 Financial Statment and AnalysisDocument7 pagesChapter 3 Financial Statment and AnalysisSusan ThapaNo ratings yet

- Analysis 1Document59 pagesAnalysis 1Gautam M100% (1)

- 1) Activity RatiosDocument28 pages1) Activity RatiosNyanNo ratings yet

- Bega Cheese FY19-20 Financial Analysis: 11% EBITDA Growth & 384% PAT RiseDocument8 pagesBega Cheese FY19-20 Financial Analysis: 11% EBITDA Growth & 384% PAT RiseHaroon KhanNo ratings yet

- FABM2-WPS OfficeDocument2 pagesFABM2-WPS OfficeAliza KhateNo ratings yet

- Financial RatiosDocument29 pagesFinancial RatiosYASHA BAIDNo ratings yet

- Ratio Analysis ParticipantsDocument17 pagesRatio Analysis ParticipantsDeepu MannatilNo ratings yet

- Financial Leverage Du Pont Analysis &growth RateDocument34 pagesFinancial Leverage Du Pont Analysis &growth Rateahmad jamalNo ratings yet

- Finance PDFDocument136 pagesFinance PDFjariyarasheedNo ratings yet

- Analyzing Financial Statements for Decision MakingDocument32 pagesAnalyzing Financial Statements for Decision MakingmarieieiemNo ratings yet

- Financial Analysis and Reporting 1Document4 pagesFinancial Analysis and Reporting 1Anonymous ryxSr2No ratings yet

- Financial Accounting Ratio Anaylsis FormulasDocument2 pagesFinancial Accounting Ratio Anaylsis Formulasbasit111100% (1)

- Part III - Developing The Entrepreneurial PlanDocument24 pagesPart III - Developing The Entrepreneurial Plannivedita choudhuryNo ratings yet

- Ratio Analysis 2020Document26 pagesRatio Analysis 2020sabelo.j.nkosi.5No ratings yet

- Day 5 Ratios and Examples 2024Document18 pagesDay 5 Ratios and Examples 2024Kit KatNo ratings yet

- Chapter 6 For CUP Financial AccountingDocument15 pagesChapter 6 For CUP Financial Accountingratanak_kong1-9No ratings yet

- Value Investor EncyclopediaDocument1,111 pagesValue Investor EncyclopediamanojdavangeNo ratings yet

- Final Exam Ibrahim Helmy, Advanced FinanceDocument30 pagesFinal Exam Ibrahim Helmy, Advanced FinanceIbrahim HelmyNo ratings yet

- Key Financial Ratios GuideDocument25 pagesKey Financial Ratios GuideGaurav HiraniNo ratings yet

- ACFINMA ReveiwerDocument14 pagesACFINMA ReveiwerKat LontokNo ratings yet

- Ratio AnalysisDocument34 pagesRatio AnalysisavdhutshirsatNo ratings yet

- Financial Statement Analysis Using RatiosDocument26 pagesFinancial Statement Analysis Using RatiosSophia NicoleNo ratings yet

- Presentation On Economics and Accountancy For Bankers: Presented byDocument19 pagesPresentation On Economics and Accountancy For Bankers: Presented byAnirbanGhoshNo ratings yet

- Fin202 - Chap 3,4,5,6Document20 pagesFin202 - Chap 3,4,5,6An Gia Khuong (K17 CT)No ratings yet

- HO 4 Analisis Laporan KeuanganDocument44 pagesHO 4 Analisis Laporan KeuanganChintiaNo ratings yet

- Business Plan Content: Elaborated By: - DateDocument20 pagesBusiness Plan Content: Elaborated By: - DateephNo ratings yet

- Chapter 3 Summary - Dion Bonaventura - 2006464940Document4 pagesChapter 3 Summary - Dion Bonaventura - 2006464940Dion Bonaventura ManaluNo ratings yet

- Unit 6-JO A F-1 PDFDocument36 pagesUnit 6-JO A F-1 PDFPavan ChitragarNo ratings yet

- PPT1-Financial Statements & AnalysisDocument42 pagesPPT1-Financial Statements & AnalysisKumudNo ratings yet

- Financial Ratios - Sheet1Document4 pagesFinancial Ratios - Sheet1Melanie SamsonaNo ratings yet

- Chapter 2 Financial AnalysisDocument26 pagesChapter 2 Financial AnalysisCarl JovianNo ratings yet

- Ratio Analysis FormulaeDocument3 pagesRatio Analysis FormulaeErica DsouzaNo ratings yet

- Ratio AnalysisDocument6 pagesRatio AnalysisMinha ShabbirNo ratings yet

- Ratio AnalysisDocument113 pagesRatio AnalysisNAMAN SRIVASTAV100% (1)

- Chapter 2 - Evaluating A Firm's Financial Performance: 2005, Pearson Prentice HallDocument47 pagesChapter 2 - Evaluating A Firm's Financial Performance: 2005, Pearson Prentice HallNur SyakirahNo ratings yet

- Financial Statement AnalysisDocument10 pagesFinancial Statement AnalysisBeth Diaz LaurenteNo ratings yet

- Fam - 1Document20 pagesFam - 1shahidNo ratings yet

- Ratio AnalysisDocument17 pagesRatio Analysisragz22100% (1)

- Financial Statement AnalysisDocument10 pagesFinancial Statement AnalysisAli Gokhan Kocan100% (1)

- Bank Financial Statements and Performance MetricsDocument107 pagesBank Financial Statements and Performance MetricsNur AlamNo ratings yet

- Financial Ratios FormulaDocument4 pagesFinancial Ratios FormulaKamlesh SinghNo ratings yet

- ProjectDocument7 pagesProjectAamer MansoorNo ratings yet

- Bank Ratio Analysis v.2Document30 pagesBank Ratio Analysis v.2moe.jee6173100% (1)

- BA 569 Financial RatiosDocument7 pagesBA 569 Financial RatiosMariaNo ratings yet

- Business Metrics and Tools; Reference for Professionals and StudentsFrom EverandBusiness Metrics and Tools; Reference for Professionals and StudentsNo ratings yet

- Midterm Exmiantion - BUP - Advance Reserch Methodology - FIN 5102 - MBA PDFDocument1 pageMidterm Exmiantion - BUP - Advance Reserch Methodology - FIN 5102 - MBA PDFNazia YousufNo ratings yet

- Semester Final SyllabusDocument2 pagesSemester Final SyllabusNazia YousufNo ratings yet

- Problems: Chapter 31: MergersDocument27 pagesProblems: Chapter 31: MergersNazia YousufNo ratings yet

- Problems: Chapter 31: MergersDocument27 pagesProblems: Chapter 31: MergersNazia YousufNo ratings yet

- Study Unit 1 FAC1601Document18 pagesStudy Unit 1 FAC1601andreqwNo ratings yet

- Solution Manual For Corporate Finance A Focused Approach 6th Edition by Ehrhard Brigham ISBN 1305637100 9781305637108Document36 pagesSolution Manual For Corporate Finance A Focused Approach 6th Edition by Ehrhard Brigham ISBN 1305637100 9781305637108stephanievargasogimkdbxwn100% (25)

- Statement For Ufone # 03327121166: Account DetailsDocument5 pagesStatement For Ufone # 03327121166: Account DetailsDaniRanaNo ratings yet

- ITD Publication Decade Sharing ExperiencesDocument217 pagesITD Publication Decade Sharing ExperiencesDiego P00No ratings yet

- Econ 1 - Problem Set 6 With SolutionsDocument13 pagesEcon 1 - Problem Set 6 With SolutionsChilly Wu100% (4)

- Role of Nbfcs and Hfcs in Driving Sustainable GDP Growth in IndiaDocument44 pagesRole of Nbfcs and Hfcs in Driving Sustainable GDP Growth in IndiaVivek BandebucheNo ratings yet

- Namibia - The New Port of Walvis Bay Container Terminal Project - Appraisal ReportDocument38 pagesNamibia - The New Port of Walvis Bay Container Terminal Project - Appraisal ReportMohamed ElfawalNo ratings yet

- Distributions To Shareholders: Dividends and Share RepurchasesDocument28 pagesDistributions To Shareholders: Dividends and Share RepurchasesShantal kate LimNo ratings yet

- Albatross Capital Budgeting ProglemDocument1 pageAlbatross Capital Budgeting Proglemنواف القحطانيNo ratings yet

- FromDocument4 pagesFromKeith BoltonNo ratings yet

- Statement of Cash Flows Final TermDocument20 pagesStatement of Cash Flows Final TermAG VenturesNo ratings yet

- Principles of Taxation: Introduction and Chapter 1 Types of Taxes and The Jurisdictions That Use ThemDocument17 pagesPrinciples of Taxation: Introduction and Chapter 1 Types of Taxes and The Jurisdictions That Use ThemprasadkulkarnigitNo ratings yet

- Real Estate Financial Analysis Workbook: Revised June 21, 2010Document31 pagesReal Estate Financial Analysis Workbook: Revised June 21, 2010Truong Pham33% (3)

- Enable TDSDocument3 pagesEnable TDSharshita kaushikNo ratings yet

- Revised Schedule VI Balance Sheet and Profit Loss StatementDocument4 pagesRevised Schedule VI Balance Sheet and Profit Loss StatementRavi BhattNo ratings yet

- OJT Company ProfileDocument9 pagesOJT Company ProfileEira ShaneNo ratings yet

- Honours 3rd Year EconomicsDocument11 pagesHonours 3rd Year Economicsrokeyaislam693No ratings yet

- 2013 HSR Update December ReportDocument18 pages2013 HSR Update December ReportDarren KrauseNo ratings yet

- Income Tax NotificationDocument5 pagesIncome Tax NotificationjaksandcoNo ratings yet

- Personal Finance Workbook 3eDocument130 pagesPersonal Finance Workbook 3eShashi Sharma67% (3)

- Index (2014)Document3,905 pagesIndex (2014)NocoJoeNo ratings yet

- PCL - Boiler O&M - 20may19 PDFDocument3 pagesPCL - Boiler O&M - 20may19 PDFgopala krishnanNo ratings yet

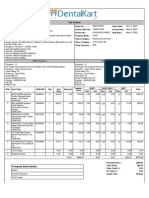

- Tax Invoice for Dental SuppliesDocument2 pagesTax Invoice for Dental SuppliesPriyanka GandhiNo ratings yet

- US Internal Revenue Service: Irb03-52Document41 pagesUS Internal Revenue Service: Irb03-52IRSNo ratings yet

- Solution Manual For International Accounting 5th Edition Timothy Doupnik Mark Finn Giorgio Gotti Hector PereraDocument36 pagesSolution Manual For International Accounting 5th Edition Timothy Doupnik Mark Finn Giorgio Gotti Hector Pereracranny.pentoseeu9227100% (48)

- G.R. No. 125948 - First Philippine Industrial Corp. v. Court of AppealsDocument4 pagesG.R. No. 125948 - First Philippine Industrial Corp. v. Court of AppealsMegan AglauaNo ratings yet

- Tax4861 2022 TL 103 0 BDocument99 pagesTax4861 2022 TL 103 0 BFlorence ApleniNo ratings yet

- DHL Express - USA Customs Duty InvoiceDocument1 pageDHL Express - USA Customs Duty InvoiceShahid SaleemNo ratings yet

- Calculate Payroll for Mohammed AgencyDocument8 pagesCalculate Payroll for Mohammed AgencyIsrael KifleNo ratings yet

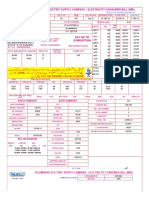

- Iesco Online Bill PDFDocument2 pagesIesco Online Bill PDFAdnan MunirNo ratings yet