You might also like

- Practice Problems, CH 12Document6 pagesPractice Problems, CH 12scridNo ratings yet

- F0013 Exercise 12 Problems/Exercises in Financial RatiosDocument3 pagesF0013 Exercise 12 Problems/Exercises in Financial RatiosDuaaaaNo ratings yet

- Colgate-Palmolive Company (CL)Document4 pagesColgate-Palmolive Company (CL)Nicolás Campero AcedoNo ratings yet

- Balance Sheet: Pyramid Analysis Exercise Year 1 Year 2 Year 3 Year 4Document9 pagesBalance Sheet: Pyramid Analysis Exercise Year 1 Year 2 Year 3 Year 4PylypNo ratings yet

- Course Folder Fall 2022Document26 pagesCourse Folder Fall 2022Areeba QureshiNo ratings yet

- Accounting Assignment QuestionDocument14 pagesAccounting Assignment QuestionsureshdassNo ratings yet

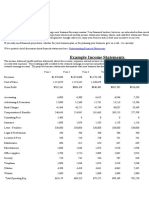

- Example For Financial Statement AnalysisDocument2 pagesExample For Financial Statement AnalysisMobile Legends0% (1)

- SCALP Handout 040Document2 pagesSCALP Handout 040Cher NaNo ratings yet

- SCALP Handout 040Document2 pagesSCALP Handout 040Cher NaNo ratings yet

- SCALP Handout 040Document2 pagesSCALP Handout 040Eren CuestaNo ratings yet

- Acc 291 Acc 291 Acc 291 Acc 291 Acc 291 Acc 291Document201 pagesAcc 291 Acc 291 Acc 291 Acc 291 Acc 291 Acc 291290acc100% (2)

- 8 Session 20 Pillar 02 Finance Management Part 1Document13 pages8 Session 20 Pillar 02 Finance Management Part 1Azfah AliNo ratings yet

- Cash Flow From Assets - Solution PDFDocument3 pagesCash Flow From Assets - Solution PDFSeptian Sugestyo PutroNo ratings yet

- Chapter 4. Financial Ratio Analyses and Their Implications To Management Learning ObjectivesDocument29 pagesChapter 4. Financial Ratio Analyses and Their Implications To Management Learning ObjectivesChieMae Benson QuintoNo ratings yet

- Balance Sheet of Maple Leaf: AssetsDocument12 pagesBalance Sheet of Maple Leaf: Assets01290101002675No ratings yet

- Bdo BalancesheetDocument6 pagesBdo BalancesheetroilesatheaNo ratings yet

- Grumpy Cat Company Comparative Statements of Financial Position December 31, 2020 and 2019 2020 2019 AssetsDocument2 pagesGrumpy Cat Company Comparative Statements of Financial Position December 31, 2020 and 2019 2020 2019 AssetsKatherine GablinesNo ratings yet

- Holoease: Jacob Sheridan 4/13/2020 To Perform A Financial Analysis For The Startup Tech Company, HoloeaseDocument11 pagesHoloease: Jacob Sheridan 4/13/2020 To Perform A Financial Analysis For The Startup Tech Company, HoloeaseJacob SheridanNo ratings yet

- Fin - AnalysisDocument2 pagesFin - Analysisajignacio.05No ratings yet

- The Balance Sheet and Income StatementDocument3 pagesThe Balance Sheet and Income Statementdhanya1995No ratings yet

- Chap 010Document19 pagesChap 010AshutoshNo ratings yet

- Leverage Ratio Exercise-1546993Document5 pagesLeverage Ratio Exercise-1546993k.aycansenNo ratings yet

- 3 - CokeDocument30 pages3 - CokePranali SanasNo ratings yet

- Balbala TongDocument4 pagesBalbala TongRizalene AgustinNo ratings yet

- MOD Technical Proposal 1.0Document23 pagesMOD Technical Proposal 1.0Scott TigerNo ratings yet

- HE 4 Questions - Updated-1Document13 pagesHE 4 Questions - Updated-1halelz69No ratings yet

- XYZ CompanyDocument4 pagesXYZ CompanycarinolokmoNo ratings yet

- Case Study #3Document5 pagesCase Study #3Jenny OjoylanNo ratings yet

- BERISO, Ella's Financial Status Analysis 2022Document8 pagesBERISO, Ella's Financial Status Analysis 2022kasandra dawn BerisoNo ratings yet

- Example Income Statements: Business Plan Financial ProjectionsDocument3 pagesExample Income Statements: Business Plan Financial ProjectionsSUMANTO SHARANNo ratings yet

- Target Final AnalysisDocument5 pagesTarget Final AnalysisSatyam1771No ratings yet

- IN Financial Management 1: Leyte CollegesDocument20 pagesIN Financial Management 1: Leyte CollegesJeric LepasanaNo ratings yet

- Balance Sheet: 2016 2017 2018 Assets Non-Current AssetsDocument6 pagesBalance Sheet: 2016 2017 2018 Assets Non-Current AssetsAhsan KamranNo ratings yet

- Finance For Non-Finance: Ratios AppleDocument12 pagesFinance For Non-Finance: Ratios AppleAvinash GanesanNo ratings yet

- ACFrOgCQb6wa8qC80YIgWx nX6TZBAv20t36Y6v4IINI tRrVqMKoatALM-RVzRoSlFJ3q DBWgUS7WKpaLaGx4C85SucFsMtbhmcAs-y6GE5Sgvzh4F49OEvpet2gphKgF6qFglhWYwVwKMmoJDocument3 pagesACFrOgCQb6wa8qC80YIgWx nX6TZBAv20t36Y6v4IINI tRrVqMKoatALM-RVzRoSlFJ3q DBWgUS7WKpaLaGx4C85SucFsMtbhmcAs-y6GE5Sgvzh4F49OEvpet2gphKgF6qFglhWYwVwKMmoJDarlene Bacatan AmancioNo ratings yet

- Quiz RatiosDocument4 pagesQuiz RatiosAmmar AsifNo ratings yet

- Yates Case Study - LT 11Document23 pagesYates Case Study - LT 11JerryJoshuaDiazNo ratings yet

- Cash Flow Statement-ShortDocument27 pagesCash Flow Statement-ShortLaurene Delos ReyesNo ratings yet

- Ezz Steel Ratio Analysis - Fall21Document10 pagesEzz Steel Ratio Analysis - Fall21farahNo ratings yet

- Excel File For Financial Ratio Activities UpdatedDocument4 pagesExcel File For Financial Ratio Activities Updated0a0lvbht4No ratings yet

- IMT CeresDocument10 pagesIMT Cerescabmeuk07No ratings yet

- Research Problem Michael Franco AccountingDocument5 pagesResearch Problem Michael Franco AccountingMichael FrancoNo ratings yet

- BSNL Balance SheetDocument15 pagesBSNL Balance SheetAbhishek AgarwalNo ratings yet

- ABS-CBN Corporation and Subsidiaries Consolidated Statements of Financial Position (Amounts in Thousands)Document10 pagesABS-CBN Corporation and Subsidiaries Consolidated Statements of Financial Position (Amounts in Thousands)Mark Angelo BustosNo ratings yet

- Finance Quiz 3Document43 pagesFinance Quiz 3Peak ChindapolNo ratings yet

- Tutorial Questions - Trimester - 2210.Document26 pagesTutorial Questions - Trimester - 2210.premsuwaatiiNo ratings yet

- IMT - Ceres Gardening CompanyDocument5 pagesIMT - Ceres Gardening Companysshenoy05No ratings yet

- Reports SampleDocument20 pagesReports SampleChristian Jade Lumasag NavaNo ratings yet

- Reliance CommunicationsDocument117 pagesReliance Communicationsrahul m dNo ratings yet

- Research For OBUDocument14 pagesResearch For OBUM Burhan SafiNo ratings yet

- Latihan Tugas ALK - Prospective AnalysisDocument3 pagesLatihan Tugas ALK - Prospective AnalysisSelvy MonibollyNo ratings yet

- HOndaDocument8 pagesHOndaRizwan Sikandar 6149-FMS/BBA/F20No ratings yet

- Requirement 1: BALANCE SHEETDocument3 pagesRequirement 1: BALANCE SHEETAnnabeth BrionNo ratings yet

- Five Below 2018 Financial StatementsDocument4 pagesFive Below 2018 Financial StatementsElie GergesNo ratings yet

- Numbers Tables BallsDocument5 pagesNumbers Tables BallsKia Khyte FloresNo ratings yet

- Financial Plan For A Start UpDocument12 pagesFinancial Plan For A Start UpNayab ArshadNo ratings yet

- WA2Document3 pagesWA2Ahmed HassaanNo ratings yet

- Financial Statement Analysis: Jeddah International College Answer PaperDocument4 pagesFinancial Statement Analysis: Jeddah International College Answer PaperBushraYousafNo ratings yet

- Practice Set 2 Pfizer HM SolvedDocument17 pagesPractice Set 2 Pfizer HM SolvedNISHA BANSALNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Week 2-Basic Cost ManagementDocument21 pagesWeek 2-Basic Cost ManagementRichard Oliver CortezNo ratings yet

- A Comparative Analysis of Hero and Bajaj Auto Ltd.Document18 pagesA Comparative Analysis of Hero and Bajaj Auto Ltd.shvmkushwah55No ratings yet

- Po Pt. Wahana Solusi Prima Ik Amboja (Kitchen Equipment New)Document2 pagesPo Pt. Wahana Solusi Prima Ik Amboja (Kitchen Equipment New)ismailNo ratings yet

- Vidhyoday - BCK Revision ChartsDocument21 pagesVidhyoday - BCK Revision Chartsmishrakumkum526No ratings yet

- Absorption and Marginal CostingDocument34 pagesAbsorption and Marginal CostingOsama Khan100% (1)

- Bukit Darah PLCDocument28 pagesBukit Darah PLCDuminiNo ratings yet

- Installment SalesDocument5 pagesInstallment SalesMarianne LanuzaNo ratings yet

- Financial Statement 2014Document355 pagesFinancial Statement 2014Akmal Idrus100% (1)

- Supply Chain of ArrowDocument26 pagesSupply Chain of ArrowNamanJainNo ratings yet

- Financial Statement AnalysisDocument9 pagesFinancial Statement AnalysisSitio BayabasanNo ratings yet

- Cost 531 2021 AssignmentDocument10 pagesCost 531 2021 AssignmentWaylee CheroNo ratings yet

- Economics and Society NotesDocument46 pagesEconomics and Society NotesArkar Myo KyawNo ratings yet

- R23 Financial Reporting StandardsDocument30 pagesR23 Financial Reporting StandardsDiegoNo ratings yet

- PENgarap-FS RedjDocument43 pagesPENgarap-FS RedjAndrea AtonducanNo ratings yet

- Social Media MarketingDocument59 pagesSocial Media MarketingMinhaz Zainul50% (2)

- aSelf-Made Secrets The Regular Girl Guide To Building A Profitable Online Empire by Marina de GiovanniDocument65 pagesaSelf-Made Secrets The Regular Girl Guide To Building A Profitable Online Empire by Marina de GiovanniLaurithaletiixd3100% (1)

- Ariel Marketing MixDocument9 pagesAriel Marketing MixIann AcutinaNo ratings yet

- Marketing Channel Strategy 8Th Edition Palmatier Test Bank Full Chapter PDFDocument37 pagesMarketing Channel Strategy 8Th Edition Palmatier Test Bank Full Chapter PDFTeresaMoorefaksg100% (10)

- 03 x03 Activity Costs WPDocument25 pages03 x03 Activity Costs WPRobert CastilloNo ratings yet

- Taj FinalDocument94 pagesTaj Finaldivya0007100% (4)

- DeVry ACCT 212 Final Exam 100% Correct AnswerDocument4 pagesDeVry ACCT 212 Final Exam 100% Correct AnswerJulia Richardson100% (1)

- PERLINDUNGAN HUKUM TERHADAP PEMILIK SAHAM PERUSAHAAN YANG PAILIT-Abraham Gilbert SimatupangDocument15 pagesPERLINDUNGAN HUKUM TERHADAP PEMILIK SAHAM PERUSAHAAN YANG PAILIT-Abraham Gilbert SimatupangIMBHB UHNNo ratings yet

- Dissertation On Debt Securities Market in IndiaDocument103 pagesDissertation On Debt Securities Market in Indiaumesh kumar sahu0% (2)

- Final - Continental AirlinesDocument13 pagesFinal - Continental AirlinesTaskin HafizNo ratings yet

- LOG713 Models For Production Management Exercises Week 37: Problem 1Document3 pagesLOG713 Models For Production Management Exercises Week 37: Problem 1Константин СтефановичNo ratings yet

- Topic: Statement of Financial Position (SFP) : Individual Performance Task/ Activity (Week 1 in The Module)Document11 pagesTopic: Statement of Financial Position (SFP) : Individual Performance Task/ Activity (Week 1 in The Module)Joana Jean SuymanNo ratings yet

- Answers Microeconomics: 3 Consumer ChoiceDocument3 pagesAnswers Microeconomics: 3 Consumer Choiceyogesh gunawatNo ratings yet

- Sample: Business Plan Business NameDocument10 pagesSample: Business Plan Business NameDan688No ratings yet

- Audit First Take 2Document23 pagesAudit First Take 2Pau CaisipNo ratings yet

- Business Plan ProjectDocument4 pagesBusiness Plan Projectapi-463825837No ratings yet