You might also like

- Maximizing Profits in Perfectly Competitive MarketsDocument4 pagesMaximizing Profits in Perfectly Competitive MarketsRodney Meg Fitz Balagtas100% (1)

- Producer and Actor Mutual AgreementDocument3 pagesProducer and Actor Mutual AgreementKrishNo ratings yet

- ACC5116 - HOBA - Additional ProblemsDocument6 pagesACC5116 - HOBA - Additional ProblemsCarl Dhaniel Garcia Salen100% (1)

- Telstra BillDocument1 pageTelstra Billl lNo ratings yet

- Agreement-Loan CollateralDocument1 pageAgreement-Loan CollateralHannah Mica Velasco-OandasanNo ratings yet

- Perfect CompetitionDocument27 pagesPerfect CompetitionFlorie May SaynoNo ratings yet

- 2.1. Perfect CompetitionDocument73 pages2.1. Perfect Competitionapi-3696178100% (5)

- Perfect Competition, Cost & Output DeterminationDocument70 pagesPerfect Competition, Cost & Output DeterminationVũ TrangNo ratings yet

- 5perfect CompetitionDocument19 pages5perfect CompetitionSHERIF GABERNo ratings yet

- Lec 15,16,17perfect CompetitionDocument19 pagesLec 15,16,17perfect CompetitionSabira RahmanNo ratings yet

- Pure CompetitionDocument9 pagesPure Competitioncindycanlas_07No ratings yet

- Assignment 2Document3 pagesAssignment 2Anum HussainNo ratings yet

- Perfect Competition ExplainedDocument6 pagesPerfect Competition ExplainedΜιχάλης ΘεοχαρόπουλοςNo ratings yet

- Firms in Perfectly Competitive Markets: Chapter Summary and Learning ObjectivesDocument33 pagesFirms in Perfectly Competitive Markets: Chapter Summary and Learning ObjectivesseriosulyawksomNo ratings yet

- Econ Microeconomics 4 4Th Edition Mceachern Solutions Manual Full Chapter PDFDocument35 pagesEcon Microeconomics 4 4Th Edition Mceachern Solutions Manual Full Chapter PDFeric.herrara805100% (11)

- ECON Microeconomics 4 4th Edition McEachern Solutions Manual 1Document14 pagesECON Microeconomics 4 4th Edition McEachern Solutions Manual 1debra100% (37)

- ECO101 Perfect Competitive MarketDocument14 pagesECO101 Perfect Competitive Marketxawad13No ratings yet

- Microeconomics: Output and CostsDocument16 pagesMicroeconomics: Output and CostsArmin RidžalovićNo ratings yet

- Question AnswerDocument6 pagesQuestion AnswerSoloymanNo ratings yet

- MarketDocument42 pagesMarketSnn News TubeNo ratings yet

- Micro Lecture 4Document16 pagesMicro Lecture 4Cate MasilunganNo ratings yet

- Unit 3Document20 pagesUnit 3SivaramkrishnanNo ratings yet

- Chapter 8 Profit Maximization &cmptitive SupplyDocument92 pagesChapter 8 Profit Maximization &cmptitive Supplysridhar7892No ratings yet

- Economic Analysis Ch.7.2023Document24 pagesEconomic Analysis Ch.7.2023Amgad ElshamyNo ratings yet

- Perfect Competition MC Practice With AnswersDocument8 pagesPerfect Competition MC Practice With AnswersMaría José AmezquitaNo ratings yet

- Business Economics V1Document9 pagesBusiness Economics V1Anees MerchantNo ratings yet

- Market Structure and Perfect CompetitionDocument3 pagesMarket Structure and Perfect Competitionafrocircus09No ratings yet

- Profit Maximization and Competitive Supply: Review QuestionsDocument14 pagesProfit Maximization and Competitive Supply: Review QuestionsTonoy Peter CorrayaNo ratings yet

- 2.2. MonopolyDocument52 pages2.2. Monopolyapi-3696178100% (2)

- Perfect Competition: 1.large Numbers of Sellers and BuyersDocument10 pagesPerfect Competition: 1.large Numbers of Sellers and Buyersatik jawadNo ratings yet

- Econ2011-Chapter 8: Competitive Markets (Perfect Competition)Document10 pagesEcon2011-Chapter 8: Competitive Markets (Perfect Competition)RosemaryTanNo ratings yet

- Managerial EconomicsDocument24 pagesManagerial EconomicsVatsal LadNo ratings yet

- Eco MCQDocument4 pagesEco MCQSenthil Kumar GanesanNo ratings yet

- Micro Economic Assighment Send MainDocument9 pagesMicro Economic Assighment Send MainMohd Arhaan KhanNo ratings yet

- Chapter 9 SUMMARY SECTION CDocument4 pagesChapter 9 SUMMARY SECTION ClalesyeuxNo ratings yet

- Pure Competition in The Short Run Four Market Models: Very Large Numbers of Independent Sellers EachDocument2 pagesPure Competition in The Short Run Four Market Models: Very Large Numbers of Independent Sellers EachAriane Jane CachoNo ratings yet

- Production Function Chapter Explaining Key Concepts Like Fixed Variable InputsDocument12 pagesProduction Function Chapter Explaining Key Concepts Like Fixed Variable InputsarthurNo ratings yet

- Module 5 - Chapter 7 Q&ADocument6 pagesModule 5 - Chapter 7 Q&ABusn DNo ratings yet

- Perfect Competition (Part 1)Document18 pagesPerfect Competition (Part 1)Wasif KhanNo ratings yet

- Chapter 8 Profit Maximization and Competitive Supply: Review QuestionsDocument9 pagesChapter 8 Profit Maximization and Competitive Supply: Review QuestionsAnisaNo ratings yet

- Chapter 14Document2 pagesChapter 14usama farooqNo ratings yet

- Managerial Economics: Unit 9Document18 pagesManagerial Economics: Unit 9Mary Grace V. PeñalbaNo ratings yet

- BE - TUTORIAL 5 - STU 2Document16 pagesBE - TUTORIAL 5 - STU 2Gia LinhNo ratings yet

- Understanding Short-Run Supply Curves for Perfectly Competitive FirmsDocument4 pagesUnderstanding Short-Run Supply Curves for Perfectly Competitive FirmsAwais KhanNo ratings yet

- 2nd Economics Week 10 CompleteDocument5 pages2nd Economics Week 10 CompleteHamza BukhariNo ratings yet

- Market Structures HandoutDocument10 pagesMarket Structures HandoutSuzanne HolmesNo ratings yet

- Parkin 13ge Econ IMDocument12 pagesParkin 13ge Econ IMDina SamirNo ratings yet

- Pure Competition in Short Run - NotesDocument6 pagesPure Competition in Short Run - Notessouhad.abouzakiNo ratings yet

- Monopolistic Competition and OligopolyDocument94 pagesMonopolistic Competition and OligopolyVardaanNo ratings yet

- Perfect CompetitionDocument12 pagesPerfect CompetitionMikail Lee BelloNo ratings yet

- Managerial Economics - Short Answer CHDocument4 pagesManagerial Economics - Short Answer CHAnkita T. MooreNo ratings yet

- Survey of Econ 3Rd Edition Sexton Solutions Manual Full Chapter PDFDocument33 pagesSurvey of Econ 3Rd Edition Sexton Solutions Manual Full Chapter PDFedward.goodwin761100% (12)

- ME. MonopolisticDocument141 pagesME. MonopolisticAndrewson BautistaNo ratings yet

- Business EconomicsDocument13 pagesBusiness EconomicsQuerida FernandesNo ratings yet

- CH 06Document12 pagesCH 06LinNo ratings yet

- Monopolistic CompetitionDocument21 pagesMonopolistic CompetitionBrigitta Devita ArdityasariNo ratings yet

- Monopoly Oligopoly Monopolistic Competition Perfect CompetitionDocument8 pagesMonopoly Oligopoly Monopolistic Competition Perfect CompetitionDerry Mipa SalamNo ratings yet

- Chapter Four: Price and Out Put Determination Under Perfect CompetitionDocument49 pagesChapter Four: Price and Out Put Determination Under Perfect Competitioneyob yohannesNo ratings yet

- Brue3e Chap07 FinalDocument14 pagesBrue3e Chap07 Finalnadiahnur07No ratings yet

- PomDocument63 pagesPomAllen Fourever50% (2)

- Perfect Competition in 8 ChaptersDocument16 pagesPerfect Competition in 8 ChaptersAbdulrahman Alotaibi100% (1)

- Market StructureDocument20 pagesMarket StructureJan Allyson BiagNo ratings yet

- Perfect Competition and Equilibrium of FirmsDocument7 pagesPerfect Competition and Equilibrium of FirmsGA ahuja Pujabi aaNo ratings yet

- Linking Words ExerciseDocument4 pagesLinking Words ExerciseAmiNo ratings yet

- Determiners ExerciseDocument6 pagesDeterminers ExerciseSumedha SunayaNo ratings yet

- Gerund vs. InfinitiveDocument5 pagesGerund vs. InfinitiveSumedha SunayaNo ratings yet

- Connecting Words ExerciseDocument6 pagesConnecting Words ExerciseSumedha SunayaNo ratings yet

- Subject-Verb Agreement ExerciseDocument4 pagesSubject-Verb Agreement ExerciseSumedha SunayaNo ratings yet

- Prepositions ExerciseDocument6 pagesPrepositions ExerciseJoão B. M. FilhoNo ratings yet

- Tenses Worksheet: 1. We .. Here For Two HoursDocument6 pagesTenses Worksheet: 1. We .. Here For Two HoursSumedha SunayaNo ratings yet

- Conjunctions ExerciseDocument6 pagesConjunctions ExerciseJoão B. M. FilhoNo ratings yet

- Gap Filling Vocabulary ExerciseDocument6 pagesGap Filling Vocabulary ExerciseSumedha SunayaNo ratings yet

- Gerund vs. InfinitiveDocument5 pagesGerund vs. InfinitiveJoão B. M. FilhoNo ratings yet

- Question Tags Exercise: 1. No One Knows The Answer, ?Document5 pagesQuestion Tags Exercise: 1. No One Knows The Answer, ?Sumedha SunayaNo ratings yet

- Question Words ExerciseDocument5 pagesQuestion Words ExerciseSumedha SunayaNo ratings yet

- Transitive vs. IntransitiveDocument5 pagesTransitive vs. IntransitiveSumedha SunayaNo ratings yet

- Subject-Verb Agreement: 1. The Performance of The Students .. ExcellentDocument5 pagesSubject-Verb Agreement: 1. The Performance of The Students .. ExcellentSumedha SunayaNo ratings yet

- Articles ExerciseDocument6 pagesArticles ExerciseSumedha SunayaNo ratings yet

- Adverbs Exercise: 1. He Narrated The Incident inDocument5 pagesAdverbs Exercise: 1. He Narrated The Incident inSumedha SunayaNo ratings yet

- Tenses Exercise: 1. I Will Follow You Wherever YouDocument6 pagesTenses Exercise: 1. I Will Follow You Wherever YouSumedha SunayaNo ratings yet

- Beginner Level Grammar ExerciseDocument5 pagesBeginner Level Grammar ExerciseSumedha SunayaNo ratings yet

- Active and Passive Voice ExerciseDocument6 pagesActive and Passive Voice ExerciseSumedha SunayaNo ratings yet

- Gap Filling Exercise (Tenses)Document6 pagesGap Filling Exercise (Tenses)Sumedha Sunaya100% (1)

- Passive Voice ExerciseDocument6 pagesPassive Voice ExerciseSumedha SunayaNo ratings yet

- 108 Names Ganga MaataDocument13 pages108 Names Ganga MaataSumedha SunayaNo ratings yet

- Gap Filling ExerciseDocument6 pagesGap Filling ExerciseSumedha SunayaNo ratings yet

- Idiomatic Expressions QuizDocument6 pagesIdiomatic Expressions QuizSumedha SunayaNo ratings yet

- 1359 - APS Macro Student - Money Market and Loanable Funds MarketDocument6 pages1359 - APS Macro Student - Money Market and Loanable Funds MarketSumedha SunayaNo ratings yet

- Elasticity of Demand, Economic Lowdown Podcast Series - STDocument4 pagesElasticity of Demand, Economic Lowdown Podcast Series - STSumedha SunayaNo ratings yet

- Confusing Words ExerciseDocument5 pagesConfusing Words ExerciseSumedha SunayaNo ratings yet

- 1359 - APS Macro Teacher - Money Market and Loanable Funds MarketDocument4 pages1359 - APS Macro Teacher - Money Market and Loanable Funds MarketSumedha SunayaNo ratings yet

- 1359 - APS Macro Solution - Money Market and Loanable Funds MarketDocument6 pages1359 - APS Macro Solution - Money Market and Loanable Funds MarketSumedha SunayaNo ratings yet

- Exploring-Strategies-and-Challenges-in-Weekly-Allowance-Budgeting-among-1st-year-and-2nd-year-College-Students-at-Caraga-State-University-Cabadbaran-Campus-focuses-on-understanding-the-strategies-emp-1Document17 pagesExploring-Strategies-and-Challenges-in-Weekly-Allowance-Budgeting-among-1st-year-and-2nd-year-College-Students-at-Caraga-State-University-Cabadbaran-Campus-focuses-on-understanding-the-strategies-emp-1Geralyn RefugioNo ratings yet

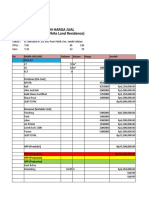

- Estimasi Perhitungan Harga Jual Perumahan WLR 2Document25 pagesEstimasi Perhitungan Harga Jual Perumahan WLR 2Next LevelManagementNo ratings yet

- Insights into Technical Visits from a Case Study of AVEX IncDocument8 pagesInsights into Technical Visits from a Case Study of AVEX IncJavier RamirezNo ratings yet

- Barriers To EntrepreneurshipDocument7 pagesBarriers To EntrepreneurshipAmanDeep SinghNo ratings yet

- Bcom Fa - 20230121013946Document9 pagesBcom Fa - 20230121013946Swayam AgarwalNo ratings yet

- Abm TermsDocument2 pagesAbm TermsAxeliaNo ratings yet

- Black BookDocument26 pagesBlack BookYash soshteNo ratings yet

- Department of Mechanical Engineering ME8094-Computer Integrated Manufacturing Systems Unit I - MCQ BankDocument10 pagesDepartment of Mechanical Engineering ME8094-Computer Integrated Manufacturing Systems Unit I - MCQ BankSanjayVaghelaNo ratings yet

- Financial Reporting and Audit Evidence: by Mwamba Ally Jingu: Fcpa PHDDocument20 pagesFinancial Reporting and Audit Evidence: by Mwamba Ally Jingu: Fcpa PHDAdil KhamisNo ratings yet

- Marketing ManagementDocument6 pagesMarketing ManagementMohammad Fajar SidikNo ratings yet

- T0 2022-2023 MS FA - WorkbookDocument18 pagesT0 2022-2023 MS FA - WorkbookZhuozhi WuNo ratings yet

- DPI Programme GoalsDocument11 pagesDPI Programme GoalsGodfrey KakalaNo ratings yet

- Mathematical Literacy p1 Sep 2022 Eastern CapeDocument15 pagesMathematical Literacy p1 Sep 2022 Eastern CapeRexNo ratings yet

- Maf 5101 Financial AccountingDocument2 pagesMaf 5101 Financial AccountingertaudNo ratings yet

- Allevia DeliverDocument1 pageAllevia DeliverSITI NURHASLINDA ZAKARIANo ratings yet

- Medalleo Low Rise - 01-Mar-2023 - 1Document2 pagesMedalleo Low Rise - 01-Mar-2023 - 1Karan PhoolwaniNo ratings yet

- Vietnam Logistics Industry RealityDocument10 pagesVietnam Logistics Industry RealityQuỳnh GiaoNo ratings yet

- Mercurial Lite Paper v1Document9 pagesMercurial Lite Paper v1ivan chenNo ratings yet

- Sydnor2010 - Overinsuring Modest RisksDocument24 pagesSydnor2010 - Overinsuring Modest RisksRoberto PaezNo ratings yet

- Presentation - HDFC Dividend Yield FundDocument27 pagesPresentation - HDFC Dividend Yield FundRitesh ChatterjeeNo ratings yet

- Seminar Presentation On: Small Scale IndustriesDocument7 pagesSeminar Presentation On: Small Scale IndustriesSAATHVIK SHEKARNo ratings yet

- Practice Questions - 1-2 PDFDocument29 pagesPractice Questions - 1-2 PDFHarish C NairNo ratings yet

- Monopoly: Imba Nccu Managerial Economics Jack WuDocument26 pagesMonopoly: Imba Nccu Managerial Economics Jack WuMelina KurniawanNo ratings yet

- Super Procure - Company IntroductionDocument14 pagesSuper Procure - Company IntroductionshadabhashimNo ratings yet

- Budgeting Guide for ExpensesDocument6 pagesBudgeting Guide for ExpensesJulieth CaviativaNo ratings yet

- World Trade: An: Eleventh EditionDocument33 pagesWorld Trade: An: Eleventh EditionYUJIA HUNo ratings yet