You might also like

- Chapter 4 Branch AccountingDocument31 pagesChapter 4 Branch AccountingAkkamaNo ratings yet

- Adv CH Onefor 3rd YearDocument32 pagesAdv CH Onefor 3rd Yearalemayehu100% (2)

- Chapter Two Accounting For Sales Agency and Principal Head Office and Branch 2.1. Distinction Between Sales Agency and BranchDocument19 pagesChapter Two Accounting For Sales Agency and Principal Head Office and Branch 2.1. Distinction Between Sales Agency and Branchliyneh mebrahituNo ratings yet

- Advanced Fin. Acct - Chapter 1-6Document77 pagesAdvanced Fin. Acct - Chapter 1-6kaleb100% (2)

- Chap 5Document43 pagesChap 5Akm Engida67% (3)

- Chapter One Class of 2019Document24 pagesChapter One Class of 2019Kidu Yabe0% (1)

- Advanced Financial Accounting (Acfn3151)Document2 pagesAdvanced Financial Accounting (Acfn3151)alemayehu100% (4)

- Advance Chapter 2 4 - 6005941748281382493Document114 pagesAdvance Chapter 2 4 - 6005941748281382493NatnaelNo ratings yet

- Accounting and Reporting For Foreign Currencies and Translation of Foreign Currency Financial Statements PDFDocument33 pagesAccounting and Reporting For Foreign Currencies and Translation of Foreign Currency Financial Statements PDFMeselech GirmaNo ratings yet

- Chapter 3 Business Combination Edited 2Document24 pagesChapter 3 Business Combination Edited 2Qabsoo Finiinsaa100% (1)

- Accounting for G&SRF FundsDocument22 pagesAccounting for G&SRF Fundshabtamu tadesse100% (2)

- Advance I Ch-IDocument63 pagesAdvance I Ch-IUtban Ashab100% (1)

- Advanced Financial Accounting Worksheet Chapter One SolutionsDocument3 pagesAdvanced Financial Accounting Worksheet Chapter One SolutionsJichang Hik100% (3)

- Chapter Six Consolidation of Financial Statements Under Purchase AccountingDocument15 pagesChapter Six Consolidation of Financial Statements Under Purchase AccountingMelody Lisa100% (1)

- Chapter 4Document31 pagesChapter 4yebegashetNo ratings yet

- Green Company Is Considering Acquiring The Assets of Gold Company by Assuming Gold's Liabilities and byDocument5 pagesGreen Company Is Considering Acquiring The Assets of Gold Company by Assuming Gold's Liabilities and byሔርሞን ይድነቃቸው67% (3)

- Accounting For Public Sector and Civil Society-1Document147 pagesAccounting For Public Sector and Civil Society-1Zeki HDNo ratings yet

- Chapter One Joint ArrangementDocument28 pagesChapter One Joint Arrangementሔርሞን ይድነቃቸውNo ratings yet

- Fair Value Measurement: Prepared By: Michael Wells Date: June 13-17, 2016 Addis AbabaDocument60 pagesFair Value Measurement: Prepared By: Michael Wells Date: June 13-17, 2016 Addis AbabaGere Tassew100% (1)

- Advanced Financial Accounting TopicsDocument2 pagesAdvanced Financial Accounting Topicsbona birra100% (1)

- CVP AnalysisDocument30 pagesCVP AnalysisBinyam Ayele100% (1)

- Manage Accounting FundamentalsDocument100 pagesManage Accounting FundamentalsYonas100% (1)

- 03-Chapter Three-Installment and Consignment ContractsDocument22 pages03-Chapter Three-Installment and Consignment ContractsHaile100% (1)

- Government and Non-Profit Accounting WorksheetDocument6 pagesGovernment and Non-Profit Accounting WorksheetYonas100% (9)

- 3chapter Three FM ExtDocument19 pages3chapter Three FM ExtTIZITAW MASRESHANo ratings yet

- Chapter3 - Costing Methods The Costing of Resource OutputsDocument27 pagesChapter3 - Costing Methods The Costing of Resource OutputsNetsanet Belay100% (1)

- Chapter One Introduction To Taxation and Tax AccountingDocument69 pagesChapter One Introduction To Taxation and Tax AccountingMelat Gebretsion100% (2)

- Investment & Portfolio MGT AssignmentDocument2 pagesInvestment & Portfolio MGT AssignmentAgidew ShewalemiNo ratings yet

- Asfaw AberaDocument90 pagesAsfaw Aberaanteneh mekonen100% (1)

- Accounting For Income TaxDocument37 pagesAccounting For Income TaxAbdulhafiz100% (4)

- Govt ch3Document21 pagesGovt ch3Belay MekonenNo ratings yet

- Cost-Volume-Profit Analysis and Direct vs Absorption CostingDocument15 pagesCost-Volume-Profit Analysis and Direct vs Absorption CostingOROM VINE100% (4)

- Unit 3Document33 pagesUnit 3YonasNo ratings yet

- Instructions: Answer The Following Carefully. Highlight Your Answer With Color Yellow. AfterDocument9 pagesInstructions: Answer The Following Carefully. Highlight Your Answer With Color Yellow. AfterMIKASANo ratings yet

- Auditing Principles and Practices II Assignment AnswerDocument6 pagesAuditing Principles and Practices II Assignment Answerbona birra67% (3)

- Natnael Wolde Advanced Financial AccountingDocument7 pagesNatnael Wolde Advanced Financial Accountingሔርሞን ይድነቃቸው100% (1)

- Group Assignment TaxationDocument20 pagesGroup Assignment TaxationEnat Endawoke100% (1)

- Chapter 3: Business Combination: Based On IFRS 3Document38 pagesChapter 3: Business Combination: Based On IFRS 3ሔርሞን ይድነቃቸውNo ratings yet

- Accounting For Capital Project FundsDocument8 pagesAccounting For Capital Project FundsMekonnen MekuriaNo ratings yet

- Income TaxDocument36 pagesIncome Taxnati100% (1)

- Chapter One Overview of Governmental and Not For Profit Organizations 1.0. Learning ObjectivesDocument24 pagesChapter One Overview of Governmental and Not For Profit Organizations 1.0. Learning ObjectivesshimelisNo ratings yet

- General Fund Journal EntriesDocument4 pagesGeneral Fund Journal EntriesJichang HikNo ratings yet

- 4 5805514475188521062Document3 pages4 5805514475188521062eferem100% (5)

- IncomeTax IAS 12 Revised Edited GD 2020Document46 pagesIncomeTax IAS 12 Revised Edited GD 2020yonas alemuNo ratings yet

- Accounting for Inventories ChapterDocument58 pagesAccounting for Inventories Chapternarr0% (1)

- Chapter 5 Installment SalesDocument10 pagesChapter 5 Installment SalesAkkama100% (1)

- Ch.1 Questions & AnswersDocument4 pagesCh.1 Questions & Answersgdghf0% (2)

- Chapter 3 Current Liability PayrollDocument39 pagesChapter 3 Current Liability PayrollAbdi Mucee Tube100% (1)

- Unit 5: Accounting SystemsDocument22 pagesUnit 5: Accounting SystemsYonas100% (2)

- Advance Financial Accounting Group Assignment SolutionsTITLE Group 11-15 Accounting Solutions for Consignment, Branch Offices TITLE Gurmu Ephrem's Financial Accounting Assignments AnswersDocument5 pagesAdvance Financial Accounting Group Assignment SolutionsTITLE Group 11-15 Accounting Solutions for Consignment, Branch Offices TITLE Gurmu Ephrem's Financial Accounting Assignments Answerssosina eseyew100% (1)

- Assessment of Loan Repayment Performance: in Case of Awash Bank in Sikela BranchDocument9 pagesAssessment of Loan Repayment Performance: in Case of Awash Bank in Sikela Branchbundesa buzo100% (1)

- GASB Accounting and Reporting Standards for State and Local GovernmentsDocument7 pagesGASB Accounting and Reporting Standards for State and Local GovernmentsHabte Debele100% (1)

- Abaynesh Abate Advanced Financial AccountingDocument7 pagesAbaynesh Abate Advanced Financial Accountingሔርሞን ይድነቃቸውNo ratings yet

- AKDocument9 pagesAKAnonymous cJogAxQnNo ratings yet

- Public finance and taxation assignmentDocument3 pagesPublic finance and taxation assignmentEmebet TesemaNo ratings yet

- Home Office and Branch Accounting Agency 1Document20 pagesHome Office and Branch Accounting Agency 1John Stephen PendonNo ratings yet

- Ch04 Accounting Systems: Chapter Four Accounting Systems 5.1. Manual and Computerized Accounting SystetemsDocument4 pagesCh04 Accounting Systems: Chapter Four Accounting Systems 5.1. Manual and Computerized Accounting SystetemsKanbiro Orkaido100% (2)

- Adv ch-2Document16 pagesAdv ch-2Prof. Dr. Anbalagan ChinniahNo ratings yet

- 2 Branch AccountingDocument30 pages2 Branch AccountingSameer Hussain100% (3)

- Advanced FA I&II (1) (1)Document99 pagesAdvanced FA I&II (1) (1)tame kibruNo ratings yet

- Review of Major Events and Rail Infrastructure ReportsDocument218 pagesReview of Major Events and Rail Infrastructure ReportsalemayehuNo ratings yet

- Unit 2 Financial Statement AnalysisDocument17 pagesUnit 2 Financial Statement AnalysisalemayehuNo ratings yet

- St. Mary's Cost Accounting Chapter 2 SummaryDocument10 pagesSt. Mary's Cost Accounting Chapter 2 SummaryalemayehuNo ratings yet

- Job Costing: 1. Whether Actual or Estimated Costs Are UsedDocument16 pagesJob Costing: 1. Whether Actual or Estimated Costs Are UsedalemayehuNo ratings yet

- Cost Allocation: Joint-Products & Byproducts: Chapter SixDocument13 pagesCost Allocation: Joint-Products & Byproducts: Chapter SixalemayehuNo ratings yet

- Department of Labor: 22-06-001-13-001Document63 pagesDepartment of Labor: 22-06-001-13-001USA_DepartmentOfLaborNo ratings yet

- Illustration 2: InstructionDocument2 pagesIllustration 2: InstructionalemayehuNo ratings yet

- Example 1: SolutionDocument7 pagesExample 1: SolutionalemayehuNo ratings yet

- GAGE College Management Section 1 & 2 Extension Program AssignmentDocument2 pagesGAGE College Management Section 1 & 2 Extension Program AssignmentalemayehuNo ratings yet

- Accounting For Inventory ch2Document15 pagesAccounting For Inventory ch2alemayehu100% (1)

- Accounting For The Payroll System: Ethiopian Context PayrollDocument13 pagesAccounting For The Payroll System: Ethiopian Context Payrollalemayehu67% (3)

- Principles of Accounting ReceivablesDocument11 pagesPrinciples of Accounting ReceivablesalemayehuNo ratings yet

- Introduction To CompDocument47 pagesIntroduction To CompalemayehuNo ratings yet

- Accounting For The Payroll System in An Ethiopian ContextDocument11 pagesAccounting For The Payroll System in An Ethiopian ContextalemayehuNo ratings yet

- Chapter Five Microsoft WordDocument18 pagesChapter Five Microsoft WordalemayehuNo ratings yet

- Citizen and CitizenshipDocument11 pagesCitizen and CitizenshipalemayehuNo ratings yet

- Accounting For Cosignment and InstallementDocument26 pagesAccounting For Cosignment and InstallementalemayehuNo ratings yet

- Principles of Accounting ReceivablesDocument11 pagesPrinciples of Accounting ReceivablesalemayehuNo ratings yet

- Project Technical AnalysisDocument111 pagesProject Technical AnalysisalemayehuNo ratings yet

- Chapter-Four: The Law of SalesDocument7 pagesChapter-Four: The Law of SalesalemayehuNo ratings yet

- What Is ConstitutionDocument16 pagesWhat Is ConstitutionalemayehuNo ratings yet

- Financial Anaysis of ProjectDocument48 pagesFinancial Anaysis of ProjectalemayehuNo ratings yet

- History of The Project: Tions and Related Exposure DraftsDocument15 pagesHistory of The Project: Tions and Related Exposure DraftsalemayehuNo ratings yet

- Manual 3 Federal Accounting System Chapter 11. Monthly ReportsDocument38 pagesManual 3 Federal Accounting System Chapter 11. Monthly ReportsalemayehuNo ratings yet

- Business Law By: Seyoum Teka Chapter One: Introduction To LawDocument162 pagesBusiness Law By: Seyoum Teka Chapter One: Introduction To LawalemayehuNo ratings yet

- Develop A Research ProposalDocument44 pagesDevelop A Research ProposalalemayehuNo ratings yet

- 69 Ad2b22d5Document67 pages69 Ad2b22d5Terence Sze Zheng YangNo ratings yet

- Accounting Information Systems: An Overview: Addis Ababa University School of CommerceDocument20 pagesAccounting Information Systems: An Overview: Addis Ababa University School of Commercealemayehu100% (2)

- Business Combinations : Ifrs 3Document45 pagesBusiness Combinations : Ifrs 3alemayehu100% (1)

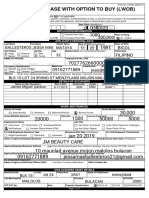

- Lwob - Application-Form Edited Edited EditedDocument2 pagesLwob - Application-Form Edited Edited Editedjessamaeballesteros21100% (1)

- SC rules on scope and limitations of taxation, tax vs regulatory feesDocument23 pagesSC rules on scope and limitations of taxation, tax vs regulatory feesArrianne ObiasNo ratings yet

- Population Dynamics in India and Implications For Economic GrowthDocument31 pagesPopulation Dynamics in India and Implications For Economic GrowthManasi D Cuty PieNo ratings yet

- Reliance Industries' Naphtha Swap DealDocument4 pagesReliance Industries' Naphtha Swap DealPrabha ArunNo ratings yet

- Notable Judgements 2v2Document120 pagesNotable Judgements 2v2Shital Darak MandhanaNo ratings yet

- Management of Financial Services PDFDocument76 pagesManagement of Financial Services PDFManisha Nagpal100% (1)

- AE211 Final ExamDocument10 pagesAE211 Final ExamMariette Alex AgbanlogNo ratings yet

- Fiib - Om - Process and Capacity AnalysisDocument9 pagesFiib - Om - Process and Capacity AnalysisCherin SamNo ratings yet

- Fe 25 CircularDocument10 pagesFe 25 CircularMaria ChaudhryNo ratings yet

- 04 Accounts Receivable - (PS)Document2 pages04 Accounts Receivable - (PS)kyle mandaresioNo ratings yet

- EsopDocument27 pagesEsopNakul GargNo ratings yet

- The Analysis of Indicators Aimed at The Sustainable Development of Alcohol Production Using The Python Programming Language (According To The Data of The Republic of Armenia)Document5 pagesThe Analysis of Indicators Aimed at The Sustainable Development of Alcohol Production Using The Python Programming Language (According To The Data of The Republic of Armenia)International Journal of Innovative Science and Research TechnologyNo ratings yet

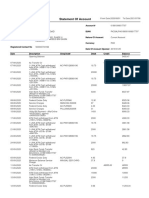

- 'Account StatementDocument11 pages'Account StatementSikander Qazi100% (2)

- Knowledge Managment BiaDocument18 pagesKnowledge Managment BiaAbhinav PandeyNo ratings yet

- 4 Capital Budgeting PDFDocument45 pages4 Capital Budgeting PDFmichael christianNo ratings yet

- Promotion BBLDocument13 pagesPromotion BBLChalista RafaNo ratings yet

- Grade A Steam Coal Soft Offer July 2010Document3 pagesGrade A Steam Coal Soft Offer July 2010dikluhNo ratings yet

- Maharashtra State Agricultural Marketing Board: Annual Report: Year 2017-2018Document41 pagesMaharashtra State Agricultural Marketing Board: Annual Report: Year 2017-2018Chittesh SachdevaNo ratings yet

- List of Analytics Consulting Companies in IndiaDocument3 pagesList of Analytics Consulting Companies in IndiaAmardeep KaushalNo ratings yet

- 10k - Manpower Inc 2011Document115 pages10k - Manpower Inc 2011dayalratikNo ratings yet

- Kingfisher Airlines Annual Report 2011 12Document85 pagesKingfisher Airlines Annual Report 2011 12Neha DhuriNo ratings yet

- 2023 Slides On Exempt IncomeDocument31 pages2023 Slides On Exempt IncomeSiphesihleNo ratings yet

- Demonetisation The Nielsen ViewDocument4 pagesDemonetisation The Nielsen ViewShriram SNo ratings yet

- Be It Enacted by The Senate and House of Representatives of The Philippine Congress AssembledDocument2 pagesBe It Enacted by The Senate and House of Representatives of The Philippine Congress AssembledMikka MonesNo ratings yet

- Inventory management key processes and termsDocument17 pagesInventory management key processes and termsVishnu Kumar SNo ratings yet

- Modified Tax Calculator With Form-16 - Version 8.2.2 (T) For 2013-14Document28 pagesModified Tax Calculator With Form-16 - Version 8.2.2 (T) For 2013-14Bijender Pal ChoudharyNo ratings yet

- HR Project ReportDocument5 pagesHR Project ReportSolo BgmNo ratings yet

- Income DistributionDocument5 pagesIncome DistributionRishiiieeeznNo ratings yet

- Coca-Cola Hellenic 2011 Annual Report (IFRS FinancialsDocument86 pagesCoca-Cola Hellenic 2011 Annual Report (IFRS FinancialskhankhanmNo ratings yet

- BankingDocument4 pagesBankingkumareshNo ratings yet