You might also like

- Fianacial MarketsDocument53 pagesFianacial MarketsMostafa ElgendyNo ratings yet

- Choosing the Right Investment Advisor: An Essential Step on the Road to Financial FreedomFrom EverandChoosing the Right Investment Advisor: An Essential Step on the Road to Financial FreedomNo ratings yet

- Chapter 7Document45 pagesChapter 7tientran.31211021669No ratings yet

- Cognitive Investing: The Key to Making Better Investment DecisionsFrom EverandCognitive Investing: The Key to Making Better Investment DecisionsNo ratings yet

- Investment Analysis & Portfolio ManagementDocument22 pagesInvestment Analysis & Portfolio ManagementJyoti YadavNo ratings yet

- Dividend Investing for Beginners: How to Build Your Investment Strategy, Find The Best Dividend Stocks to Buy, and Generate Passive Income: Investing for Beginners, #1From EverandDividend Investing for Beginners: How to Build Your Investment Strategy, Find The Best Dividend Stocks to Buy, and Generate Passive Income: Investing for Beginners, #1No ratings yet

- PARTE2 FinancialMarketDocument31 pagesPARTE2 FinancialMarketBeltrán ZamoranoNo ratings yet

- Take On the Street (Review and Analysis of Levitt's Book)From EverandTake On the Street (Review and Analysis of Levitt's Book)No ratings yet

- Robert E. Wright Vincenzo QuadriniDocument38 pagesRobert E. Wright Vincenzo Quadriniwaqas illyasNo ratings yet

- Theories of Venture CapitalDocument32 pagesTheories of Venture CapitalДр. ЦчатерйееNo ratings yet

- Credit ManagementDocument4 pagesCredit ManagementYuuna HoshinoNo ratings yet

- Financial SystemDocument31 pagesFinancial SystemAdriana Del rosarioNo ratings yet

- Unit 1 Role of Financial Institutions and MarketsDocument11 pagesUnit 1 Role of Financial Institutions and MarketsGalijang ShampangNo ratings yet

- Stocks and BondsDocument20 pagesStocks and BondsChristian CorchilNo ratings yet

- The Financial System: Opportunities and Dangers: Chapter 20 of Edition, by N. Gregory Mankiw ECO62Document97 pagesThe Financial System: Opportunities and Dangers: Chapter 20 of Edition, by N. Gregory Mankiw ECO62Usman FaruqueNo ratings yet

- Personal Finance 6th Edition Madura Solutions Manual 1Document36 pagesPersonal Finance 6th Edition Madura Solutions Manual 1karenhalesondbatxme100% (17)

- Unit 2Document31 pagesUnit 2Vanshita MalviyaNo ratings yet

- Bank Management and Operations Why Banks Are SpecialDocument88 pagesBank Management and Operations Why Banks Are SpecialJayson BungimNo ratings yet

- Finance Is The Study of Funds Management, or The Allocation ofDocument8 pagesFinance Is The Study of Funds Management, or The Allocation ofPushpa BaruaNo ratings yet

- Wealth Management: WLMT-Term 6Document41 pagesWealth Management: WLMT-Term 6Tony JosephNo ratings yet

- Financial Intermediation and Financial IntermediariesDocument25 pagesFinancial Intermediation and Financial Intermediariesglee_No ratings yet

- Module Compilation 1 3 Midterm ReviewerDocument57 pagesModule Compilation 1 3 Midterm ReviewerJared PaulateNo ratings yet

- Lending Payment and Risk TakingDocument16 pagesLending Payment and Risk TakingasifanisNo ratings yet

- An Overview of FinanceDocument34 pagesAn Overview of FinanceAhsan SaeedNo ratings yet

- Module 1 3 - BofiDocument75 pagesModule 1 3 - BofiJohn Ray AmadorNo ratings yet

- Types of InvestmentDocument41 pagesTypes of InvestmentJanina Kirsten DevezaNo ratings yet

- Chapter 5 Financial RegulationsDocument39 pagesChapter 5 Financial RegulationsYonas BamlakuNo ratings yet

- Personal Finance 5th Edition Jeff Madura Solutions Manual 1Document8 pagesPersonal Finance 5th Edition Jeff Madura Solutions Manual 1kurt100% (45)

- Personal Finance 5th Edition Jeff Madura Solutions Manual 1Document36 pagesPersonal Finance 5th Edition Jeff Madura Solutions Manual 1karenhalesondbatxme100% (26)

- Part 1 The Philipine Financial SystemDocument17 pagesPart 1 The Philipine Financial SystemRona MaglahusNo ratings yet

- Service Organizations: Presented by Renji K PhilipDocument20 pagesService Organizations: Presented by Renji K PhiliprenjikphilipNo ratings yet

- B.AEco (Hon) - Macro - 4th Sem - Lesson 9Document15 pagesB.AEco (Hon) - Macro - 4th Sem - Lesson 9Sharad RanjanNo ratings yet

- Sec Questions Investors Should AskDocument20 pagesSec Questions Investors Should Askhaha2012No ratings yet

- Introduction To Financial SystemDocument28 pagesIntroduction To Financial SystemAarambh waghNo ratings yet

- Money and Banking Chapter 8Document3 pagesMoney and Banking Chapter 8Gene'sNo ratings yet

- Raising CapitalDocument12 pagesRaising CapitalFinnNo ratings yet

- Chapter Six: Risk Management in Financial InstitutionsDocument22 pagesChapter Six: Risk Management in Financial InstitutionsMikias DegwaleNo ratings yet

- Investor Behavior and Asset Allocation ProcessDocument19 pagesInvestor Behavior and Asset Allocation ProcessAnjali Ajz77No ratings yet

- Behavioural Finance With Private ClientsDocument14 pagesBehavioural Finance With Private ClientsRohan GhallaNo ratings yet

- 111Document5 pages111Adonis GaoiranNo ratings yet

- HimdasunDocument15 pagesHimdasunLameuneNo ratings yet

- Chapter 4: Financial IntermediationDocument15 pagesChapter 4: Financial IntermediationJhermaine SantiagoNo ratings yet

- Digital Assignment - 2: Submitted To: Submitted byDocument12 pagesDigital Assignment - 2: Submitted To: Submitted byMonashreeNo ratings yet

- Report in Fm1 PDFDocument36 pagesReport in Fm1 PDFQuennie Guy-abNo ratings yet

- Overview of Financial EnggDocument44 pagesOverview of Financial Engghandore_sachinNo ratings yet

- Week 4Document42 pagesWeek 4Maqsood AhmadNo ratings yet

- Chapter 1 05Document29 pagesChapter 1 05Mebrat WubanteNo ratings yet

- Fim - Activity 2Document3 pagesFim - Activity 2Sittie Rajma SapalNo ratings yet

- CH - 1 Indian Financial SystemDocument29 pagesCH - 1 Indian Financial Systemtrupti_viradiyaNo ratings yet

- Prelims Finance MergedDocument149 pagesPrelims Finance MergedBlueBladeNo ratings yet

- PFM FinalDocument56 pagesPFM FinalMadhuri SinghNo ratings yet

- Finalcil Market - Bba Unit One &twoDocument79 pagesFinalcil Market - Bba Unit One &twoBhagawat PaudelNo ratings yet

- SampleDocument7 pagesSampleCheng Chin HwaNo ratings yet

- Financial Literacy 1Document40 pagesFinancial Literacy 1leonwaypNo ratings yet

- Chapter+3 +financial+institutionsDocument85 pagesChapter+3 +financial+institutionsThảo Nhi LêNo ratings yet

- Investment Banking & The Financial Economics of Banking: Kevin Chiang, UVMDocument34 pagesInvestment Banking & The Financial Economics of Banking: Kevin Chiang, UVMHelenNo ratings yet

- Session 3 - Financial Intermediation NDocument33 pagesSession 3 - Financial Intermediation NVaibhav AggarwalNo ratings yet

- A5 - Risk ManagementDocument30 pagesA5 - Risk ManagementNoel GatbontonNo ratings yet

- Module 1.1 Financial MarketsDocument60 pagesModule 1.1 Financial MarketssateeshjorliNo ratings yet

- Audit Test & Audit SamplingDocument18 pagesAudit Test & Audit SamplingMd. Shadman Sakib 1610973630No ratings yet

- Acnabin Chartered AccountsDocument8 pagesAcnabin Chartered AccountsMd. Shadman Sakib 1610973630No ratings yet

- Audit Test & Audit SamplingDocument18 pagesAudit Test & Audit SamplingMd. Shadman Sakib 1610973630No ratings yet

- Internal Control.1pptxDocument19 pagesInternal Control.1pptxMd. Shadman Sakib 1610973630No ratings yet

- Chapter-17-LBO MergerDocument69 pagesChapter-17-LBO MergerSami Jatt0% (1)

- Money and BankingDocument531 pagesMoney and BankingKofi Appiah-DanquahNo ratings yet

- Bitcoin Finale Full 2Document15 pagesBitcoin Finale Full 2Md. Shadman Sakib 1610973630No ratings yet

- Time Value of MoneyDocument47 pagesTime Value of MoneyMd. Shadman Sakib 1610973630No ratings yet

- Pillsburry CaseDocument10 pagesPillsburry CaseMd. Shadman Sakib 1610973630No ratings yet

- Negotiable InstrumentDocument11 pagesNegotiable InstrumentMd. Shadman Sakib 1610973630No ratings yet

- Capacity of PartiesDocument19 pagesCapacity of PartiesMd. Shadman Sakib 1610973630No ratings yet

- Cost of CapitalDocument19 pagesCost of CapitalMd. Shadman Sakib 1610973630No ratings yet

- Capital BudgetingDocument33 pagesCapital BudgetingMd. Shadman Sakib 1610973630No ratings yet

- Risk and ReturnDocument37 pagesRisk and ReturnMd. Shadman Sakib 1610973630No ratings yet

- Capacity of PartiesDocument19 pagesCapacity of PartiesMd. Shadman Sakib 1610973630No ratings yet

- Chapter-7: Free ConsentDocument60 pagesChapter-7: Free ConsentMd. Shadman Sakib 1610973630No ratings yet

- Legality of Object and ConsiderationDocument4 pagesLegality of Object and ConsiderationMd. Shadman Sakib 1610973630No ratings yet

- Negotiable InstrumentDocument11 pagesNegotiable InstrumentMd. Shadman Sakib 1610973630No ratings yet

- Chapter-5: Void & Voidable AgreementsDocument11 pagesChapter-5: Void & Voidable AgreementsMd. Shadman Sakib 1610973630No ratings yet

- Chapter-4: ConsiderationDocument18 pagesChapter-4: ConsiderationMd. Shadman Sakib 1610973630No ratings yet

- ReceiptDocument4 pagesReceiptAnas MohamedNo ratings yet

- Chapter 8: Money Markets and Capital Markets: Group 2Document51 pagesChapter 8: Money Markets and Capital Markets: Group 2Queen TwoNo ratings yet

- Theory of Financial Intermediation. 1.0 History of Financail IntermediariesDocument23 pagesTheory of Financial Intermediation. 1.0 History of Financail IntermediariesAmeh AnyebeNo ratings yet

- The Negotiable Instrument Act 1881Document32 pagesThe Negotiable Instrument Act 1881Johanna FrancisNo ratings yet

- Lecture On Amortization and Amortization ScheduleDocument3 pagesLecture On Amortization and Amortization ScheduleAeiaNo ratings yet

- A Study On Customer Relationship Management at Bandhan Bank LimitedDocument55 pagesA Study On Customer Relationship Management at Bandhan Bank LimitedNitinAgnihotriNo ratings yet

- Complete List of BanksDocument2 pagesComplete List of BanksBadawi ManuelleNo ratings yet

- Impact of Covid 19 On Bankig SectorDocument3 pagesImpact of Covid 19 On Bankig SectorShaloo MinzNo ratings yet

- Sample Board ResoDocument1 pageSample Board ResoJuhnna Mae CezarNo ratings yet

- Online Consultation Instructions: Anna Christina V. Cusi, MD, DPPS, DPSDBPDocument1 pageOnline Consultation Instructions: Anna Christina V. Cusi, MD, DPPS, DPSDBPPrince JacintoNo ratings yet

- 11th Accountancy DraftDocument8 pages11th Accountancy Draftmohit pandeyNo ratings yet

- TSYS Bank Request Change Document-101Document1 pageTSYS Bank Request Change Document-101Keller Brown JnrNo ratings yet

- Notification: General Assam ShtllongDocument5 pagesNotification: General Assam ShtllongAbhimanyu KshirsagarNo ratings yet

- Answer Key Summative Exam 1 & 2 Business FinanceDocument5 pagesAnswer Key Summative Exam 1 & 2 Business Financejelay agresorNo ratings yet

- PPTDocument27 pagesPPTafeeraNo ratings yet

- CRE52 - Standardized ApproachDocument44 pagesCRE52 - Standardized ApproachCuong NguyenNo ratings yet

- Digital Transformation in Financial Services - (2017)Document242 pagesDigital Transformation in Financial Services - (2017)AbelBabelNo ratings yet

- UCG7p2g3rF SBICAPsDocument31 pagesUCG7p2g3rF SBICAPsHarapriyaPandaNo ratings yet

- Acc Financial MarketsDocument153 pagesAcc Financial Marketssharielles /No ratings yet

- Department of Education: Barangay G.S. Rosario, Carranglan, Nueva EcijaDocument4 pagesDepartment of Education: Barangay G.S. Rosario, Carranglan, Nueva EcijaDiaRamosAysonNo ratings yet

- Difference Between Traditional Banking and E-Banking 2Document13 pagesDifference Between Traditional Banking and E-Banking 2Neha ShajiNo ratings yet

- Importance of CRMDocument5 pagesImportance of CRMRamya MuraliNo ratings yet

- Savings ChargesDocument1 pageSavings ChargesGanesh ChaudharyNo ratings yet

- MIS 301 Group Assignment Quesion 3Document3 pagesMIS 301 Group Assignment Quesion 3Mohammad HammadNo ratings yet

- AC-HS101-S4-2022-5 Money, Financial and Banking SystemsDocument39 pagesAC-HS101-S4-2022-5 Money, Financial and Banking SystemsVedang BaleNo ratings yet

- Chapter 1. L1.4 Nature of Securities and Risks InvolvedDocument3 pagesChapter 1. L1.4 Nature of Securities and Risks InvolvedvibhuNo ratings yet

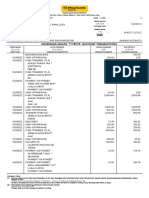

- MBBsavings - 164017 212412 - 2022 08 31 PDFDocument4 pagesMBBsavings - 164017 212412 - 2022 08 31 PDFAdeela fazlinNo ratings yet

- Macroeconomics Class 12 Money and BankingDocument11 pagesMacroeconomics Class 12 Money and BankingstudentNo ratings yet

- Shane Koyczans PlacesDocument3 pagesShane Koyczans Placesapi-501779888No ratings yet

- Remittance Application Form MAR2022 E - Form PDFDocument2 pagesRemittance Application Form MAR2022 E - Form PDFAlldyNo ratings yet