You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5819)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Tutorial 2e Residence StatusDocument2 pagesTutorial 2e Residence StatusnatlyhNo ratings yet

- Jardine Davies Insurance Brokers vs. AliposaDocument2 pagesJardine Davies Insurance Brokers vs. AliposaCarlota Nicolas Villaroman100% (1)

- FijiTimes - June 29 2012 PDFDocument48 pagesFijiTimes - June 29 2012 PDFfijitimescanadaNo ratings yet

- Assessment 1 Reflective JournalDocument12 pagesAssessment 1 Reflective Journalhoney arguellesNo ratings yet

- Unitname Chaptername SectionnameDocument14 pagesUnitname Chaptername SectionnameDev GulatiNo ratings yet

- Mona Mohamed, Menna Selem, Mariam, ManalDocument8 pagesMona Mohamed, Menna Selem, Mariam, ManalMenna HamoudaNo ratings yet

- 1990 Watts and ZimmermanDocument27 pages1990 Watts and ZimmermanSaiful Iksan PratamaNo ratings yet

- GEC 105 Final ExamdsDocument3 pagesGEC 105 Final ExamdskunohoshiNo ratings yet

- City of Iloilo vs. Smart CommunicationsDocument2 pagesCity of Iloilo vs. Smart CommunicationsKim SimagalaNo ratings yet

- Acct 410 - Government and Not-for-ProfitDocument7 pagesAcct 410 - Government and Not-for-Profitllutz7No ratings yet

- Class - Problems On The Assessment of NonresidentDocument2 pagesClass - Problems On The Assessment of Nonresidentsakibctg416No ratings yet

- CIR vs. BurmeisterDocument13 pagesCIR vs. BurmeisterMaan MabbunNo ratings yet

- Quantitative Demand AnalysisDocument55 pagesQuantitative Demand AnalysisJessica Adharana KurniaNo ratings yet

- ECB Speeches and Interviews January 2022Document28 pagesECB Speeches and Interviews January 2022Bruce JefferyNo ratings yet

- Fabm MidtermDocument7 pagesFabm MidtermFritzie Mae Ruzhel GuimbuayanNo ratings yet

- Chapter 19 BKM Investments 9e SolutionsDocument11 pagesChapter 19 BKM Investments 9e Solutionsnpiper29100% (1)

- Alternative Minimum TaxDocument2 pagesAlternative Minimum TaxJeremy A. MillerNo ratings yet

- CV JunaidDocument2 pagesCV JunaidM JunaidNo ratings yet

- MSE604 Ch. 7 - Decpreciation & Income TaxesDocument30 pagesMSE604 Ch. 7 - Decpreciation & Income TaxesYoussef MedhatNo ratings yet

- Trust AccountingDocument13 pagesTrust AccountingPriyalaxmi Uma100% (5)

- Rabijit Contract Evabot SignedDocument8 pagesRabijit Contract Evabot SignedrabijitNo ratings yet

- Peshawar Electric Supply Company: Say No To CorruptionDocument2 pagesPeshawar Electric Supply Company: Say No To CorruptionRiaz Ul HaqNo ratings yet

- Sfas 131Document48 pagesSfas 131zimnycold100% (1)

- Handouts Vat On ImportationDocument2 pagesHandouts Vat On ImportationAldrin Giray MagpayoNo ratings yet

- Pacquiao v. MilabaoDocument26 pagesPacquiao v. Milabaoaudreydql5No ratings yet

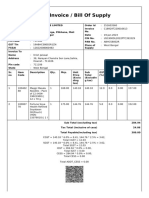

- Tax Invoice / Bill of SupplyDocument2 pagesTax Invoice / Bill of SupplyKrish JaiswalNo ratings yet

- Tax Exempt Corporationunder Tha NircDocument13 pagesTax Exempt Corporationunder Tha NircaletheialogheiaNo ratings yet

- Accounting Textbook Solutions - 43Document19 pagesAccounting Textbook Solutions - 43acc-expertNo ratings yet

- Archirodon Inv January 2024 (RTTS)Document11 pagesArchirodon Inv January 2024 (RTTS)SyedAsrarNo ratings yet

- Taxatio MCQDocument10 pagesTaxatio MCQAtif KhanNo ratings yet