You might also like

- CALCULATE: Impact of Credit Score On LoansDocument2 pagesCALCULATE: Impact of Credit Score On LoansElise Smoll (Elise)100% (1)

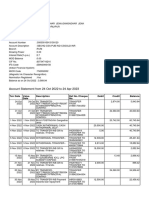

- Citi Bank Statement PDFDocument6 pagesCiti Bank Statement PDFblack bird100% (1)

- Account Summary Payment Information: New Balance - $78.87Document6 pagesAccount Summary Payment Information: New Balance - $78.87AriadnaUrsachi100% (1)

- PDF DocumentDocument5 pagesPDF DocumentNicolauNo ratings yet

- Investment Banking, 3E: Valuation, Lbos, M&A, and IposDocument11 pagesInvestment Banking, 3E: Valuation, Lbos, M&A, and IposBook Sittiwat100% (1)

- Chapter 17 - Selected Quantitative Problems & SolutionsDocument2 pagesChapter 17 - Selected Quantitative Problems & Solutions分享区No ratings yet

- Exclusive Listing: Baker Real Estate Incorporated, Brokerage. Brokers ProtectedDocument10 pagesExclusive Listing: Baker Real Estate Incorporated, Brokerage. Brokers ProtectedAnonymous BwovhJVhNo ratings yet

- Capital OneDocument6 pagesCapital Oneapi-285064294No ratings yet

- Evaluating Consumer Loans: William Chittenden Edited and Updated The Powerpoint Slides For This EditionDocument61 pagesEvaluating Consumer Loans: William Chittenden Edited and Updated The Powerpoint Slides For This Edition分享区No ratings yet

- Simple LBO ModelDocument14 pagesSimple LBO ModelProfessorAsim Kumar MishraNo ratings yet

- EMI Calculator For Home Loan, Car Loan & Personal Loan in IndiaDocument7 pagesEMI Calculator For Home Loan, Car Loan & Personal Loan in Indiadrvichram94No ratings yet

- Your Reverse Mortgage Summary: You Could GetDocument11 pagesYour Reverse Mortgage Summary: You Could GetPete Santilli100% (1)

- Streamline CompareDocument1 pageStreamline Comparejoe@josephhummel.comNo ratings yet

- Weighted Average Cost of Capital Calculator: Company Variables: Synthetic Debt RatingsDocument9 pagesWeighted Average Cost of Capital Calculator: Company Variables: Synthetic Debt RatingsinoocentkillerNo ratings yet

- Report To The Congress On The Profitability of Credit Card Operations of Depository Institutions July 2019Document18 pagesReport To The Congress On The Profitability of Credit Card Operations of Depository Institutions July 2019RAJAMANICKAMNo ratings yet

- Featured Calculators & Articles: Home Loan Personal Loan Car LoanDocument2 pagesFeatured Calculators & Articles: Home Loan Personal Loan Car LoanSk RajNo ratings yet

- EMI Calculator For Home Loan, Car Loan & Personal Loan in IndiaDocument2 pagesEMI Calculator For Home Loan, Car Loan & Personal Loan in Indiakingarvind7777No ratings yet

- Chase Investor Preso 11.4.09Document31 pagesChase Investor Preso 11.4.09ychartsNo ratings yet

- Bond CalculatorDocument14 pagesBond CalculatorWaseem ButtNo ratings yet

- EMI For Personal Loan in IndiaDocument2 pagesEMI For Personal Loan in IndiaAbhishek VishwakarmaNo ratings yet

- Home Affordability Calculator: IncomeDocument5 pagesHome Affordability Calculator: IncomeRomi RobertoNo ratings yet

- EMI Calculator For Home Loan, Car Loan & Personal Loan in IndiaDocument7 pagesEMI Calculator For Home Loan, Car Loan & Personal Loan in IndiaCA JANAMDEEP SINGHNo ratings yet

- Chap VDocument12 pagesChap VDonna Lee Bug-atanNo ratings yet

- Original: Your Credit Score and The Price You Pay For CreditDocument26 pagesOriginal: Your Credit Score and The Price You Pay For CreditMaritza CardonaNo ratings yet

- Customer Profitability Analysis and Loan PricingDocument36 pagesCustomer Profitability Analysis and Loan PricingFahim RahmanNo ratings yet

- Loan AmortizationDocument17 pagesLoan Amortizationayushabhishek64No ratings yet

- Loan AgreementMITC - 1705588392880Document24 pagesLoan AgreementMITC - 1705588392880844501abhayNo ratings yet

- Pre-Application WorksheetDocument2 pagesPre-Application WorksheetBrettKingNo ratings yet

- SCI Investor Day 2022Document104 pagesSCI Investor Day 2022Victor CamposNo ratings yet

- 16 SOBC Booklet Excluding FED ENG 081221 2Document61 pages16 SOBC Booklet Excluding FED ENG 081221 2Faizan WahidNo ratings yet

- Personal Loans: Things To Know and Deals To Go ForDocument7 pagesPersonal Loans: Things To Know and Deals To Go FordineshmarginalNo ratings yet

- Relationship Summary:: Page 1 of 7Document7 pagesRelationship Summary:: Page 1 of 7my nameNo ratings yet

- Practical Problems: Lustration 1 After 8Document4 pagesPractical Problems: Lustration 1 After 8Kiran Kumar KBNo ratings yet

- EMI Calculator For Personal LoanDocument4 pagesEMI Calculator For Personal LoanStarNo ratings yet

- ESRB Risk DashboardDocument43 pagesESRB Risk DashboardGasimovskyNo ratings yet

- Chap 008Document5 pagesChap 008hasnat sakibNo ratings yet

- Solutions of Portfolio TheoryDocument40 pagesSolutions of Portfolio TheoryApeksha netlizNo ratings yet

- Amex Credit Cards Fees ChargesDocument4 pagesAmex Credit Cards Fees ChargesriyadhphyNo ratings yet

- Fecredit Valuation AnalysisDocument8 pagesFecredit Valuation AnalysisHong Son PhanNo ratings yet

- Loans Receivable and Receivable Financing EdDocument6 pagesLoans Receivable and Receivable Financing EdCrisangel de LeonNo ratings yet

- When Making Credit Card Payments, Please Be Reminded of The FollowingDocument1 pageWhen Making Credit Card Payments, Please Be Reminded of The FollowingJohn Paolo DionisioNo ratings yet

- Maria Ialongo 84-23 Manton Street Apt 3E Briarwood Ny 11435-1813Document4 pagesMaria Ialongo 84-23 Manton Street Apt 3E Briarwood Ny 11435-1813Keiver jimenezNo ratings yet

- Dec 23Document4 pagesDec 23trishamhall1979No ratings yet

- Motorcycle LoanDocument10 pagesMotorcycle Loanrowilson reyNo ratings yet

- Gettingoutofdebt Spreadsheet Edit1Document6 pagesGettingoutofdebt Spreadsheet Edit1brianfromboiseNo ratings yet

- Customer Statement: Ally Bank P.O. Box 70377 Philadelphia, PA 19176-0377Document4 pagesCustomer Statement: Ally Bank P.O. Box 70377 Philadelphia, PA 19176-0377garrettloehrNo ratings yet

- Term Valued CFDocument14 pagesTerm Valued CFEl MemmetNo ratings yet

- Lending by Dr. Charles DansoDocument11 pagesLending by Dr. Charles Dansomohamed MostafaNo ratings yet

- Chapter 2-Sources of Fund-Part 1 - To StudentDocument9 pagesChapter 2-Sources of Fund-Part 1 - To StudentPháp NguyễnNo ratings yet

- Farmington Bank 1 Company Overview: 1.1 DescriptionDocument3 pagesFarmington Bank 1 Company Overview: 1.1 DescriptionAaron GenotaNo ratings yet

- Determinants of Loan Performance in P2P LendingDocument4 pagesDeterminants of Loan Performance in P2P Lendingberhanu geleboNo ratings yet

- Bank NII and NIM Scenarios Case StudyDocument8 pagesBank NII and NIM Scenarios Case Studynedhul50No ratings yet

- 8 Get Your Finances & Credit in OrderDocument15 pages8 Get Your Finances & Credit in OrdercropdownunderNo ratings yet

- Credit and CollectionDocument17 pagesCredit and CollectionDia Cessianne VillarolaNo ratings yet

- Lender Lender: What Is A 'Lender' What Is A 'Lender'Document6 pagesLender Lender: What Is A 'Lender' What Is A 'Lender'moNo ratings yet

- Key Corp 3Q07 PresentationDocument26 pagesKey Corp 3Q07 Presentationmdv31500No ratings yet

- BurtonsDocument6 pagesBurtonsKritika GoelNo ratings yet

- Personal Loan EmiDocument7 pagesPersonal Loan EmiMILAN BEHERANo ratings yet

- Montage Et Ingénierie Financière 290922Document185 pagesMontage Et Ingénierie Financière 290922Abir YassineNo ratings yet

- Corporate Finance: Credit CardsDocument24 pagesCorporate Finance: Credit Cardsusmanahmadqadri100% (2)

- BDO Network Bank 2022 Annual Report Financial SupplementsDocument115 pagesBDO Network Bank 2022 Annual Report Financial Supplementsbenjamin.holhNo ratings yet

- WSP Basic LBO - VF 2Document12 pagesWSP Basic LBO - VF 2jason.sevin02No ratings yet

- EMI CalculatorDocument2 pagesEMI CalculatorSushmita SwainNo ratings yet

- Wells FargoDocument11 pagesWells FargoRafa BorgesNo ratings yet

- Credit Derivatives and Structured Credit: A Guide for InvestorsFrom EverandCredit Derivatives and Structured Credit: A Guide for InvestorsNo ratings yet

- Money and Banking Chapter 12Document8 pagesMoney and Banking Chapter 12分享区No ratings yet

- Money and Banking Chapter 13Document4 pagesMoney and Banking Chapter 13分享区No ratings yet

- Evaluating Consumer Loans: William Chittenden Edited and Updated The Powerpoint Slides For This EditionDocument61 pagesEvaluating Consumer Loans: William Chittenden Edited and Updated The Powerpoint Slides For This Edition分享区No ratings yet

- If Foreign Risk ExposureDocument40 pagesIf Foreign Risk Exposure分享区No ratings yet

- Chapter 16 - Selected Quantitative Problems & SolutionsDocument2 pagesChapter 16 - Selected Quantitative Problems & Solutions分享区No ratings yet

- Chapter 9: Cooperative Strategy: OverviewDocument20 pagesChapter 9: Cooperative Strategy: Overview分享区No ratings yet

- Strategic Management: Concepts and CasesDocument39 pagesStrategic Management: Concepts and Cases分享区No ratings yet

- Motion For Clerk To Reassign Case To Another JudgeDocument71 pagesMotion For Clerk To Reassign Case To Another JudgeNeil GillespieNo ratings yet

- Tutorial 5Document5 pagesTutorial 5Jian Zhi TehNo ratings yet

- The Abington Journal 02-20-2013Document24 pagesThe Abington Journal 02-20-2013The Times LeaderNo ratings yet

- The Abington Journal 08-31-2011Document28 pagesThe Abington Journal 08-31-2011The Times LeaderNo ratings yet

- Present and Future Value Project Math 1090Document11 pagesPresent and Future Value Project Math 1090api-260807594No ratings yet

- A Case Study of Rural Finance Self-Help Groups in Uganda and TheiDocument49 pagesA Case Study of Rural Finance Self-Help Groups in Uganda and TheiNabossa EronNo ratings yet

- Borrower's Ledger (For Compilation)Document157 pagesBorrower's Ledger (For Compilation)Dennis Lumancas LadresNo ratings yet

- Internship Report On BALDocument96 pagesInternship Report On BALM I HASSANNo ratings yet

- Orchard Bank 288451024 - AgreementNPI2701ADocument15 pagesOrchard Bank 288451024 - AgreementNPI2701AKestrel1940No ratings yet

- Account StatementDocument12 pagesAccount Statementharish rajNo ratings yet

- Combining FactorsDocument13 pagesCombining FactorsIsachar BernaldezNo ratings yet

- Destiny 200Document11 pagesDestiny 200Jeanine WallaceNo ratings yet

- The Abington Journal 07-27-2011Document28 pagesThe Abington Journal 07-27-2011The Times LeaderNo ratings yet

- CH 14Document31 pagesCH 14Bui Thi Thu Hang (K13HN)No ratings yet

- Real Estate Finance Lecture - 3 - 2021Document14 pagesReal Estate Finance Lecture - 3 - 2021Zigma NetworkNo ratings yet

- Mohamad Nazri Bin HusainDocument2 pagesMohamad Nazri Bin HusainMohamad NazriNo ratings yet

- Accounts r1201Document276 pagesAccounts r1201林和鋟No ratings yet

- Amortization Calculator - Wikipedia, The Free EncyclopediaDocument3 pagesAmortization Calculator - Wikipedia, The Free Encyclopediaapi-3712367No ratings yet

- 2018 HW2 SolutionDocument5 pages2018 HW2 SolutionAhmad Bhatti100% (1)

- Milestone® Gold Mastercard® The Bank of Missouri: Interest Rates and Interest ChargesDocument4 pagesMilestone® Gold Mastercard® The Bank of Missouri: Interest Rates and Interest ChargesDelois RoseboroNo ratings yet

- Disney Vacation ClubDocument2 pagesDisney Vacation ClubStage DoorNo ratings yet

- Materi 11 Manajemen Keuangan & Pembiayaan Usaha: 1 Kewirausahaan Dan Perencanaan BisnisDocument26 pagesMateri 11 Manajemen Keuangan & Pembiayaan Usaha: 1 Kewirausahaan Dan Perencanaan BisnisnurendahNo ratings yet

- Economics House of CR CardHouse of Cards Credit Card ProjectsDocument32 pagesEconomics House of CR CardHouse of Cards Credit Card Projectsforum502No ratings yet

- March 19, 2014Document12 pagesMarch 19, 2014The Delphos HeraldNo ratings yet

- Information Systems To Support - Door-Step Banking - Enabling ScalDocument23 pagesInformation Systems To Support - Door-Step Banking - Enabling ScalPratik PatilNo ratings yet

- I LRD 3 L HF 78 W9 NBDWDocument3 pagesI LRD 3 L HF 78 W9 NBDWBIKRAM KUMAR BEHERANo ratings yet