You might also like

- Banking Ombudsman Complaint ProcessDocument8 pagesBanking Ombudsman Complaint ProcessManini JaiswalNo ratings yet

- RegulationsDocument12 pagesRegulationsmruthunjay kadakolNo ratings yet

- Banking Ombudsman Scheme ExplainedDocument5 pagesBanking Ombudsman Scheme ExplainedAkashNo ratings yet

- Deficiency of Services in BanksDocument10 pagesDeficiency of Services in Banksshaqueeb nallamanduNo ratings yet

- Banking OmbudsmanDocument4 pagesBanking OmbudsmanAshok SutharNo ratings yet

- Deficiency of Service in Banks (India)Document10 pagesDeficiency of Service in Banks (India)Parveen Kumar0% (1)

- By: Group 4 - Jayalaxmi Desai - Kevin Ladani - Manish Jagwani - Piyush Singh - Samarth Khare - Sameer TiggaDocument72 pagesBy: Group 4 - Jayalaxmi Desai - Kevin Ladani - Manish Jagwani - Piyush Singh - Samarth Khare - Sameer TiggaShaifali ChauhanNo ratings yet

- Frequently Asked Questions: Banking Currency Foreign Exchange Government Securities Market Nbfcs Others Payment SystemsDocument3 pagesFrequently Asked Questions: Banking Currency Foreign Exchange Government Securities Market Nbfcs Others Payment SystemsAyushNo ratings yet

- OmbudsmanDocument21 pagesOmbudsmanRAYSPEARNo ratings yet

- Type of Complaints: IndiaDocument2 pagesType of Complaints: Indiaaditisalvi10No ratings yet

- Unit 5 BLDocument3 pagesUnit 5 BLzenith chhablaniNo ratings yet

- Banking OmbudsmanDocument2 pagesBanking OmbudsmanSantosh ViswaNo ratings yet

- Banking Ombudsman Scheme, 2006 (Jan 1, 2006) PDFDocument4 pagesBanking Ombudsman Scheme, 2006 (Jan 1, 2006) PDFAtanu PaulNo ratings yet

- Customer Compensation PolicyDocument20 pagesCustomer Compensation PolicyShivam SuryawanshiNo ratings yet

- 22 Ombudsman PresentationDocument29 pages22 Ombudsman PresentationHeaven DsougaNo ratings yet

- Neft TermsDocument11 pagesNeft TermsavisekmishraNo ratings yet

- What is a Banking OmbudsmanDocument9 pagesWhat is a Banking OmbudsmanAnimesh BawejaNo ratings yet

- Banking Ombudsman SchemeDocument128 pagesBanking Ombudsman SchemesbrNo ratings yet

- Personal Loans May 2021Document17 pagesPersonal Loans May 2021rdebnath004No ratings yet

- Banking Ombudsman: Meaning, Functions and WorkingDocument5 pagesBanking Ombudsman: Meaning, Functions and WorkingSapphire Sharma0% (1)

- Rtgs Neft RulesDocument11 pagesRtgs Neft RuleschennaimechNo ratings yet

- Loan PolicyDocument5 pagesLoan PolicySoumya BanerjeeNo ratings yet

- 2e9b1the Consumer Protection ActDocument9 pages2e9b1the Consumer Protection ActSidharth KapoorNo ratings yet

- Banking Ombudsman Scheme - Effective Redressal for Customer GrievancesDocument54 pagesBanking Ombudsman Scheme - Effective Redressal for Customer GrievancesMitheleshDevarajNo ratings yet

- Analysis of The Banking Ombudsman SchemeDocument44 pagesAnalysis of The Banking Ombudsman SchemeSundar Babu50% (2)

- RBI Revised Notification 6 July 2017 PDFDocument9 pagesRBI Revised Notification 6 July 2017 PDFMoneylife FoundationNo ratings yet

- Terms and Condition Personal LoanDocument1 pageTerms and Condition Personal LoanSasmita PanigrahyNo ratings yet

- What Is The Banking Ombudsman Scheme?Document10 pagesWhat Is The Banking Ombudsman Scheme?Poonam PathadeNo ratings yet

- Special Pre-Approved Personal Loan TermsDocument1 pageSpecial Pre-Approved Personal Loan TermsRam Kannan PNo ratings yet

- Banking Operations ManagementDocument30 pagesBanking Operations ManagementTariq SiddiquiNo ratings yet

- Policy For Lending To Micro and Small EnterprisesDocument8 pagesPolicy For Lending To Micro and Small Enterprisespatruni sureshkumarNo ratings yet

- Terms and Conditions Governing Immediate Payment Services (Imps) of The National Payment Corporation of India (Npci)Document6 pagesTerms and Conditions Governing Immediate Payment Services (Imps) of The National Payment Corporation of India (Npci)Sachin AgaleNo ratings yet

- Compensation Policy 28 03 2019Document10 pagesCompensation Policy 28 03 2019Arnab MitraNo ratings yet

- Customer Protection PolicyDocument7 pagesCustomer Protection PolicyRuchika RaiNo ratings yet

- Banking OmbudsmanDocument14 pagesBanking OmbudsmanAarti MaanNo ratings yet

- Annexure-A Guidelines For Conventional Banking CustomersDocument2 pagesAnnexure-A Guidelines For Conventional Banking Customersumerbashir743No ratings yet

- Banking Ombudsman: Indira Selvam.RDocument12 pagesBanking Ombudsman: Indira Selvam.RSriramNo ratings yet

- Jiyo Easy: HandbookDocument60 pagesJiyo Easy: HandbookkvchandrareddyNo ratings yet

- Union Bank of India - Terms and ConditionsDocument5 pagesUnion Bank of India - Terms and ConditionsUmesh KaneNo ratings yet

- Banking Ombudsman Scheme, 2006Document3 pagesBanking Ombudsman Scheme, 2006takshila amitNo ratings yet

- Sub: Compensation Cum Customer Relation Policy 2021 - 22: Operation & Services DeptDocument20 pagesSub: Compensation Cum Customer Relation Policy 2021 - 22: Operation & Services DeptAmitKumarNo ratings yet

- Increasing Inflationary ImpactDocument3 pagesIncreasing Inflationary ImpactAdi ButtNo ratings yet

- Guidelines On Mobile Financial ServicesDocument4 pagesGuidelines On Mobile Financial ServicesAhsan ZamanNo ratings yet

- Information Technology in Banking Term Paper ON Services Provided To Senior Citizens by Banks Submitted To, Mr. A.R.Joshi & Mrs Kalpagam UmashakarDocument15 pagesInformation Technology in Banking Term Paper ON Services Provided To Senior Citizens by Banks Submitted To, Mr. A.R.Joshi & Mrs Kalpagam UmashakarSanjay DurgaNo ratings yet

- SBI Compensation Policy 2018Document21 pagesSBI Compensation Policy 2018fictional worldNo ratings yet

- Loan Policy - ObjectivesDocument46 pagesLoan Policy - Objectivesnehamittal03No ratings yet

- Documents Needed for Insurance Claims and Ombudsman ComplaintsDocument5 pagesDocuments Needed for Insurance Claims and Ombudsman ComplaintsEkta singhNo ratings yet

- Banking OmbudsmanDocument46 pagesBanking OmbudsmanJaymaan SharmaNo ratings yet

- Merchant-to-Distributor (M2D) LOAN Terms and Conditions: Further T&CsDocument5 pagesMerchant-to-Distributor (M2D) LOAN Terms and Conditions: Further T&Csa3951804No ratings yet

- What Is Banking Ombudsman?Document5 pagesWhat Is Banking Ombudsman?Tushar SaxenaNo ratings yet

- DoorDocument4 pagesDoorapi-3807149No ratings yet

- BalanceTransfer TNCDocument3 pagesBalanceTransfer TNCRahul BaraiyaNo ratings yet

- Agent Banking in Bangladesh: AuthorityDocument2 pagesAgent Banking in Bangladesh: AuthorityAnik SarkarNo ratings yet

- Customer Compensation PolicyDocument15 pagesCustomer Compensation PolicyVaishnaviNo ratings yet

- BT ON EMI TNCDocument3 pagesBT ON EMI TNCRahul BaraiyaNo ratings yet

- RBI Master Circular, 2014Document34 pagesRBI Master Circular, 2014Devendra VermaNo ratings yet

- Access your bank accounts online with Mi-b@nkDocument81 pagesAccess your bank accounts online with Mi-b@nkkoolmaverickNo ratings yet

- Compensation Policy 2020 21Document14 pagesCompensation Policy 2020 21K. NikhilNo ratings yet

- KB220502AIMCU - Sanction Letter PDFDocument3 pagesKB220502AIMCU - Sanction Letter PDFRatnesh ShuklaNo ratings yet

- Relevancy-and-AdmissibilityDocument7 pagesRelevancy-and-Admissibilityamritam yadavNo ratings yet

- History of Insurance in IndiaDocument2 pagesHistory of Insurance in Indiaamritam yadavNo ratings yet

- The Duke Expresses Compassion Toward A Having An Enemy That Is As Empty As ShylockDocument1 pageThe Duke Expresses Compassion Toward A Having An Enemy That Is As Empty As Shylockshambhavi sinhaNo ratings yet

- Difference Between IRDA and SEBI On Their FunctionsDocument1 pageDifference Between IRDA and SEBI On Their Functionsamritam yadavNo ratings yet

- Role of IRDA in Indian Insurance SectorDocument4 pagesRole of IRDA in Indian Insurance Sectoramritam yadavNo ratings yet

- Roll No.R760218115 SAP ID 500071424: Online - Through Blackboard Learning Management SystemDocument7 pagesRoll No.R760218115 SAP ID 500071424: Online - Through Blackboard Learning Management Systemamritam yadavNo ratings yet

- IRDA & MilestonesDocument2 pagesIRDA & Milestonesamritam yadavNo ratings yet

- Passive Voice PresentationDocument14 pagesPassive Voice Presentationamritam yadavNo ratings yet

- Abstract Contracts ProjectDocument12 pagesAbstract Contracts Projectamritam yadavNo ratings yet

- R115Document7 pagesR115amritam yadavNo ratings yet

- Contract Project: A Project Report ON Case Law: Satyabrata Ghose V Mugneeram Bangur & Co. and 1954 AIR 44Document14 pagesContract Project: A Project Report ON Case Law: Satyabrata Ghose V Mugneeram Bangur & Co. and 1954 AIR 44shambhavi sinhaNo ratings yet

- Name - Amritam Shankar Topic-Management by Objectives ROLL-115 SAP ID - 500071424Document7 pagesName - Amritam Shankar Topic-Management by Objectives ROLL-115 SAP ID - 500071424amritam yadavNo ratings yet

- QP - Investement Law - Mid Term Sept 2021Document9 pagesQP - Investement Law - Mid Term Sept 2021amritam yadavNo ratings yet

- TensesDocument6 pagesTensesAmritam YaduvanshiNo ratings yet

- Company Law Assignment 115Document8 pagesCompany Law Assignment 115amritam yadavNo ratings yet

- COURSE PLAN - CPC II & The Limitation Act, 1963 CLCC3010 - BBA LLB (CORP LAW)Document14 pagesCOURSE PLAN - CPC II & The Limitation Act, 1963 CLCC3010 - BBA LLB (CORP LAW)amritam yadavNo ratings yet

- Code of Civil Procedure, 1908Document1 pageCode of Civil Procedure, 1908amritam yadavNo ratings yet

- Roll No. Sap Id: Online - Through Blackboard Learning Management SystemDocument1 pageRoll No. Sap Id: Online - Through Blackboard Learning Management Systemamritam yadavNo ratings yet

- Address For Correspondence: Career ObjectiveDocument4 pagesAddress For Correspondence: Career Objectiveamritam yadavNo ratings yet

- Yadav Labour LawDocument5 pagesYadav Labour Lawamritam yadavNo ratings yet

- An Affidavit To This Effect Is Enclosed Herewith The PetitionDocument5 pagesAn Affidavit To This Effect Is Enclosed Herewith The Petitionamritam yadavNo ratings yet

- Computer Project: Name - Amritam Shankar Yadav Project-Evolution of Computers Class Tittle - Digital DevicesDocument3 pagesComputer Project: Name - Amritam Shankar Yadav Project-Evolution of Computers Class Tittle - Digital Devicesamritam yadavNo ratings yet

- The Duke Expresses Compassion Toward A Having An Enemy That Is As Empty As ShylockDocument1 pageThe Duke Expresses Compassion Toward A Having An Enemy That Is As Empty As Shylockshambhavi sinhaNo ratings yet

- Contract Project: A Project Report ON Case Law: Satyabrata Ghose V Mugneeram Bangur & Co. and 1954 AIR 44Document14 pagesContract Project: A Project Report ON Case Law: Satyabrata Ghose V Mugneeram Bangur & Co. and 1954 AIR 44shambhavi sinhaNo ratings yet

- CLNL 1011 General English I Pre-requisites/Exposure Co-Requisites Course ObjectivesDocument5 pagesCLNL 1011 General English I Pre-requisites/Exposure Co-Requisites Course Objectivesshambhavi sinhaNo ratings yet

- CL 1Document3 pagesCL 1amritam yadavNo ratings yet

- Corporate Restructuring (Hons.) - BBALLB (Hons.) Corporate Law 2018Document6 pagesCorporate Restructuring (Hons.) - BBALLB (Hons.) Corporate Law 2018amritam yadavNo ratings yet

- Process management optimizes CPU usageDocument1 pageProcess management optimizes CPU usageamritam yadavNo ratings yet

- How to Write an Effective Legal OpinionDocument10 pagesHow to Write an Effective Legal OpinionAmritam YaduvanshiNo ratings yet

- TensesDocument6 pagesTensesAmritam YaduvanshiNo ratings yet

- INGGRISSMA2000 KDocument12 pagesINGGRISSMA2000 KGalang R Edy SantosoNo ratings yet

- Bank Reconciliation Statement PreparationDocument10 pagesBank Reconciliation Statement PreparationAngela PaduaNo ratings yet

- Assessment 2 - Lesson Plan PPDocument24 pagesAssessment 2 - Lesson Plan PPZaria TariqNo ratings yet

- BC SyllabusDocument12 pagesBC SyllabusSandesh IngaleNo ratings yet

- Road Occupancy Permit Application For The City of MississaugaDocument2 pagesRoad Occupancy Permit Application For The City of MississaugaSylvia StewartNo ratings yet

- Final Project On SEBLDocument26 pagesFinal Project On SEBLAtabur RahmanNo ratings yet

- Expansion of The Menu Option DescriptionDocument57 pagesExpansion of The Menu Option DescriptionGeraldine NkankumeNo ratings yet

- Fixed Deposit Accounts of Mahathirs Wife and 5 of His Child As Well As His CroniesDocument21 pagesFixed Deposit Accounts of Mahathirs Wife and 5 of His Child As Well As His CroniesPauline ChongNo ratings yet

- SK Financial ReportsDocument2 pagesSK Financial ReportsEugene GuillermoNo ratings yet

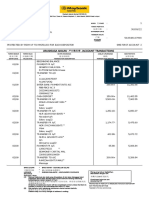

- Rs. 13.00 Rs. 1,318.22 Rs. 1,311.00: 11 Feb 2023 To 10 Mar 2023Document3 pagesRs. 13.00 Rs. 1,318.22 Rs. 1,311.00: 11 Feb 2023 To 10 Mar 2023Aayush KumarNo ratings yet

- Financial Institutions & Management Chapter 15Document35 pagesFinancial Institutions & Management Chapter 15Dominic NguyenNo ratings yet

- 6banking - Eto TalagaDocument23 pages6banking - Eto TalagaRachel LeachonNo ratings yet

- Indian Financial SystemDocument16 pagesIndian Financial Systemshankarinadar100% (1)

- Executive Summary: Internship Report On Muslim Commercial Bank, Gondal Branch AttockDocument54 pagesExecutive Summary: Internship Report On Muslim Commercial Bank, Gondal Branch Attockbilalqureshi123No ratings yet

- Unit 4: BankingDocument10 pagesUnit 4: BankingUrsu FeodosiiNo ratings yet

- Aldous I.M. S. Mirafuentes 1: 370 G. Bautista Street, San Jose Rodriguez Rizal Contact No. 09614487402 Email AddressDocument5 pagesAldous I.M. S. Mirafuentes 1: 370 G. Bautista Street, San Jose Rodriguez Rizal Contact No. 09614487402 Email AddressAngelica Nicole YongcoNo ratings yet

- Anti-Money Laundering ActDocument8 pagesAnti-Money Laundering ActKriztel CuñadoNo ratings yet

- ACCEPTANCE Nego 11.11.223Document10 pagesACCEPTANCE Nego 11.11.223Rebecca TatadNo ratings yet

- Leonardi vs. Chase Nat'l BankDocument4 pagesLeonardi vs. Chase Nat'l BankRoda May DiñoNo ratings yet

- Siddheshwar Agriculture Cooperative LTD.: Bhurakot, KanchanpurDocument6 pagesSiddheshwar Agriculture Cooperative LTD.: Bhurakot, Kanchanpurmadhu chaudharyNo ratings yet

- The Asset Market Money and Prices: Chapter 7 From Andrew B. Abel Ben BernankeDocument56 pagesThe Asset Market Money and Prices: Chapter 7 From Andrew B. Abel Ben BernankeTahir MaharNo ratings yet

- Project Report On The Functions of Commercial BanksDocument29 pagesProject Report On The Functions of Commercial BanksAnil Batra100% (2)

- Bank Mandiri Entry StrategyDocument20 pagesBank Mandiri Entry StrategyEka DarmadiNo ratings yet

- A394 E17 ChallanDocument1 pageA394 E17 ChallanSanjeev KumarNo ratings yet

- MBBcurrent 564548147990 2022-09-30 PDFDocument12 pagesMBBcurrent 564548147990 2022-09-30 PDFAdeela fazlinNo ratings yet

- Bank ReconciliationDocument5 pagesBank ReconciliationUwuuUNo ratings yet

- Arthakranti Marathi Book PDFDocument16 pagesArthakranti Marathi Book PDFGireesh VaiddyaNo ratings yet

- Bocpv0011d 2023Document4 pagesBocpv0011d 2023Vyshak Bisha ValsanNo ratings yet

- Credit Policy GuidelinesDocument4 pagesCredit Policy Guidelinesnazmul099No ratings yet

- Sample Financial ForecastingDocument16 pagesSample Financial ForecastingzubiyaNo ratings yet