You might also like

- Summary of Votes Required For Corporate ActDocument1 pageSummary of Votes Required For Corporate ActAnj100% (1)

- Summary of William H. Pike & Patrick C. Gregory's Why Stocks Go Up and DownFrom EverandSummary of William H. Pike & Patrick C. Gregory's Why Stocks Go Up and DownNo ratings yet

- OGI Who'SWho 2011Document76 pagesOGI Who'SWho 2011spinsta11100% (1)

- Petro-Canada CaseDocument17 pagesPetro-Canada CaseIgor SemenenkoNo ratings yet

- Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeDocument38 pagesPrepared by Coby Harmon University of California, Santa Barbara Westmont Collegee s tNo ratings yet

- Equity: Learning ObjectivesDocument68 pagesEquity: Learning ObjectivesFatima Azzahra SaragihNo ratings yet

- Equity: Learning ObjectivesDocument32 pagesEquity: Learning ObjectivesAASNo ratings yet

- Ekuitas Penerbitan SahamDocument32 pagesEkuitas Penerbitan SahamYoga TriatamaNo ratings yet

- Ch15 UpdatedDocument94 pagesCh15 Updatedkokmunwai717No ratings yet

- Ch15 UpdatedDocument90 pagesCh15 Updatedkokmunwai717No ratings yet

- Advanced FA I - Chapter 03, EquityDocument43 pagesAdvanced FA I - Chapter 03, EquityUtban AshabNo ratings yet

- Equity: Learning ObjectivesDocument62 pagesEquity: Learning ObjectivesElaine Lingx100% (1)

- Chp15 InstructorDocument65 pagesChp15 InstructorElaine LingxNo ratings yet

- Updated Ch15 - Shareholder's & Owner's EquityDocument47 pagesUpdated Ch15 - Shareholder's & Owner's EquitySaja AlbarjesNo ratings yet

- Act 330 Chapter 15Document71 pagesAct 330 Chapter 15Taaz TaassinNo ratings yet

- Stockholders' Equity: Intermediate AccountingDocument61 pagesStockholders' Equity: Intermediate AccountingHaris WibisonoNo ratings yet

- IFA 2 CH 6 EquityDocument53 pagesIFA 2 CH 6 Equitynatnaelsleshi3No ratings yet

- Kieso Inter Ch15 IFRS (Equity)Document55 pagesKieso Inter Ch15 IFRS (Equity)Peter Arya PrimaNo ratings yet

- Stockholders' Equity: Learning ObjectivesDocument66 pagesStockholders' Equity: Learning ObjectivesSunny SunnyNo ratings yet

- Accounting and Reporting of Stockholders' EquityDocument49 pagesAccounting and Reporting of Stockholders' EquitysueernNo ratings yet

- CH 15Document54 pagesCH 15papzdelongeNo ratings yet

- Intermediate AccountingDocument89 pagesIntermediate Accountingabood kahteeb68No ratings yet

- Chapter 14 EquityDocument60 pagesChapter 14 EquityGrace DeboraNo ratings yet

- CH 15Document79 pagesCH 15zetNo ratings yet

- ch15 EquityDocument80 pagesch15 EquityAnggrainiNo ratings yet

- Ch15 Kieso Ifrs4Document82 pagesCh15 Kieso Ifrs4Selena SevvinNo ratings yet

- Stockholders' Equity: Intermediate AccountingDocument61 pagesStockholders' Equity: Intermediate AccountingStefani Ayu ChristiartiNo ratings yet

- Stockholders' Equity: Intermediate AccountingDocument61 pagesStockholders' Equity: Intermediate AccountingStefani Ayu ChristiartiNo ratings yet

- CH 15Document85 pagesCH 15Carlene JanettaNo ratings yet

- CH 15Document77 pagesCH 15임재영No ratings yet

- L6 PDFDocument62 pagesL6 PDFTiến NguyễnNo ratings yet

- Shareholders EquityDocument51 pagesShareholders EquityHannah CorpuzNo ratings yet

- 3 CH Equity Kieso 2nd EdDocument74 pages3 CH Equity Kieso 2nd EdAkuntansi UntirtaNo ratings yet

- Intermediate Power PointDocument54 pagesIntermediate Power Pointlow profileNo ratings yet

- Corporations: Organization and Capital Stock Transactions: Accounting Principles, Ninth EditionDocument33 pagesCorporations: Organization and Capital Stock Transactions: Accounting Principles, Ninth EditionAhmed El KhateebNo ratings yet

- Stockholders' Equity Stockholders' EquityDocument72 pagesStockholders' Equity Stockholders' EquityMohammed Akhtab Ul HudaNo ratings yet

- Intermediat e AccountingDocument84 pagesIntermediat e AccountingAdriano FahleviNo ratings yet

- Ch15 EquityDocument7 pagesCh15 EquitykonyatanNo ratings yet

- CH 15 Stockholders' EquityDocument67 pagesCH 15 Stockholders' EquitySamiHadadNo ratings yet

- Lecture 11 - Stockholders EquityDocument62 pagesLecture 11 - Stockholders EquityIsyraf Hatim Mohd TamizamNo ratings yet

- Equity: Learning ObjectivesDocument32 pagesEquity: Learning ObjectivesAASNo ratings yet

- Chapter 13 SolutionsDocument45 pagesChapter 13 Solutionsaboodyuae2000No ratings yet

- Stockholders' Equity: Contributed Capital Lecture OutlineDocument6 pagesStockholders' Equity: Contributed Capital Lecture OutlineZean RazonNo ratings yet

- CFAB Accounting Chapter 11. Company Financial StatementsDocument43 pagesCFAB Accounting Chapter 11. Company Financial StatementsHuy NguyenNo ratings yet

- Lecture 12 - EquityDocument11 pagesLecture 12 - EquityThảo HảiNo ratings yet

- Accounting Capital+Stock+TransactionsDocument17 pagesAccounting Capital+Stock+TransactionsOckouri BarnesNo ratings yet

- Equity: Intermediate Accounting IFRS Edition Kieso, Weygandt, and WarfieldDocument70 pagesEquity: Intermediate Accounting IFRS Edition Kieso, Weygandt, and WarfieldagustadivNo ratings yet

- Introduction To Accounting 2 Organization and Capital Stock TransactionsDocument17 pagesIntroduction To Accounting 2 Organization and Capital Stock Transactionsalice horanNo ratings yet

- Jeter CHP 3Document54 pagesJeter CHP 3Kim StevNo ratings yet

- Advanced I Ch-IIIDocument65 pagesAdvanced I Ch-IIIWondeNo ratings yet

- Learning Objectives (Lo) : Minggu Ke 5 EquityDocument11 pagesLearning Objectives (Lo) : Minggu Ke 5 Equitycalsey azzahraNo ratings yet

- Chapter 17 1Document26 pagesChapter 17 1Diệu Linh NguyễnNo ratings yet

- Pertemuan 11 - EkuitasDocument34 pagesPertemuan 11 - EkuitasCristian Kumara PutraNo ratings yet

- Accounting For Corporate Form of Business Organizations Chapter OutlinesDocument11 pagesAccounting For Corporate Form of Business Organizations Chapter Outlinesdejen mengstieNo ratings yet

- Dividends - and - Share - Repurchases - Basics - SlidesDocument19 pagesDividends - and - Share - Repurchases - Basics - Slideszaheer9287No ratings yet

- CH 10 Acc2010 NotesDocument10 pagesCH 10 Acc2010 Notesapi-248751950No ratings yet

- Chapter 13Document13 pagesChapter 13Mondy MondyNo ratings yet

- CFA® Level I - Corporate Finance: Dividends and Share Repurchases: BasicsDocument18 pagesCFA® Level I - Corporate Finance: Dividends and Share Repurchases: BasicsAbhishek GuptaNo ratings yet

- PPT3-Consolidated Financial Statement - Date of AcquisitionDocument54 pagesPPT3-Consolidated Financial Statement - Date of AcquisitionRifdah Saphira100% (1)

- AcFn2012 Ch05 CorporationDocument62 pagesAcFn2012 Ch05 CorporationFahmi ShifferawNo ratings yet

- ch15 - Harestya - SentDocument42 pagesch15 - Harestya - SentBenedict MihoyoNo ratings yet

- Advanced Accounting: Consolidated Financial Statements-Date of AcquisitionDocument52 pagesAdvanced Accounting: Consolidated Financial Statements-Date of AcquisitiongoerginamarquezNo ratings yet

- Preview of Chapter 1: Financial AccountingDocument109 pagesPreview of Chapter 1: Financial AccountingHiếu Nguyễn Minh HoàngNo ratings yet

- Top 25 MSO's, Top 100 Cable SystemsDocument4 pagesTop 25 MSO's, Top 100 Cable SystemsVinoth KannanNo ratings yet

- Allotment of SharesDocument17 pagesAllotment of SharesHimanshu Premani100% (1)

- Tacao Vs CADocument1 pageTacao Vs CAGeorge AlmedaNo ratings yet

- Corporation Law ReviewerDocument4 pagesCorporation Law ReviewerKeziah HuelarNo ratings yet

- IGCSE Business Ch4 QuestionsDocument4 pagesIGCSE Business Ch4 Questionsferry sNo ratings yet

- Global by CompanyDocument14 pagesGlobal by CompanyJamil KhanNo ratings yet

- TK Audit ReportDocument13 pagesTK Audit ReportskyscrapperNo ratings yet

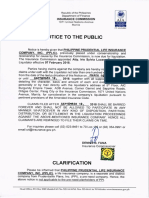

- Notice To The Public PPLIC Placed Under Liquidation Effective 07 Feb 2018Document1 pageNotice To The Public PPLIC Placed Under Liquidation Effective 07 Feb 2018Jerry MisterinoNo ratings yet

- Tutorial 2 - A202 QuestionDocument6 pagesTutorial 2 - A202 QuestionFuchoin ReikoNo ratings yet

- 120702ogj International SurveyDocument7 pages120702ogj International SurveyvinblayNo ratings yet

- Accounting: NO Judul PengarangDocument14 pagesAccounting: NO Judul Pengarangkartini11No ratings yet

- Post Money Safe User GuideDocument31 pagesPost Money Safe User GuideabermejoNo ratings yet

- BATA Annual Report 2018Document113 pagesBATA Annual Report 2018Rika AnggriaNo ratings yet

- Company ActDocument27 pagesCompany Actaryan28614No ratings yet

- Valeant Presentation PershingDocument47 pagesValeant Presentation PershingNick SposaNo ratings yet

- A Study of Corporate Governance Practices in IndiaDocument3 pagesA Study of Corporate Governance Practices in Indiaabhi malikNo ratings yet

- Group 10 AB Nuvo Grasim ABFSDocument8 pagesGroup 10 AB Nuvo Grasim ABFSPOOJA GUPTANo ratings yet

- DM 45 Old EsteiraDocument4 pagesDM 45 Old EsteiraWalissonNo ratings yet

- SponsorDocument2 pagesSponsorMeca NizaNo ratings yet

- IFR Awards 2022 RoHDocument3 pagesIFR Awards 2022 RoHRonnie KurtzbardNo ratings yet

- Crilw Part I Book PDFDocument432 pagesCrilw Part I Book PDFPavlov Kumar HandiqueNo ratings yet

- Partnership Accounting PDFDocument4 pagesPartnership Accounting PDFPamela BugarsoNo ratings yet

- 01 Website Jadual Tren 32 ETS 15 Jan 2022 - UpdateDocument2 pages01 Website Jadual Tren 32 ETS 15 Jan 2022 - UpdateWan Yoke NengNo ratings yet

- Cell Country CodesDocument29 pagesCell Country CodesYusha PatelNo ratings yet

- Endurance Technologies LimitedDocument249 pagesEndurance Technologies LimitedÂj AjithNo ratings yet

- Commercial Law Power PointDocument333 pagesCommercial Law Power PointPJ HongNo ratings yet

- Reit PPT Reitworld 2019 Annual Conference PresentationDocument34 pagesReit PPT Reitworld 2019 Annual Conference PresentationDaniel GoytrNo ratings yet