You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Financial Literacy PowerpointDocument17 pagesFinancial Literacy Powerpointapi-40190669833% (3)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Nov PDFDocument1 pageNov PDFSuresh PatelNo ratings yet

- Estatement Chase AprilDocument6 pagesEstatement Chase AprilAtta ur RehmanNo ratings yet

- Notice Under s138 of Ni ActDocument3 pagesNotice Under s138 of Ni Actshivam5singh-25No ratings yet

- Pakistan PII - Harvard Kennedy School PAEDocument35 pagesPakistan PII - Harvard Kennedy School PAEAsim JahangirNo ratings yet

- HJR.192 5th - June.1933 PDFDocument4 pagesHJR.192 5th - June.1933 PDFStar GazonNo ratings yet

- FYCE BM1804 - Income Taxation HandoutDocument17 pagesFYCE BM1804 - Income Taxation HandoutLisanna DragneelNo ratings yet

- Neo-Classical Theory of FirmsDocument14 pagesNeo-Classical Theory of FirmsAnuNo ratings yet

- MRF Extra DetailsDocument6 pagesMRF Extra DetailsAnuNo ratings yet

- MonopolyDocument68 pagesMonopolyAnuNo ratings yet

- MKT DemandDocument59 pagesMKT DemandAnuNo ratings yet

- Monopolistic Competition and OligopolyDocument47 pagesMonopolistic Competition and OligopolyAnuNo ratings yet

- Micro and Macro EconomicsDocument8 pagesMicro and Macro EconomicsAnuNo ratings yet

- MarketstructureDocument40 pagesMarketstructureAnuNo ratings yet

- Basics 2Document23 pagesBasics 2AnuNo ratings yet

- Market FailureDocument15 pagesMarket FailureAnuNo ratings yet

- Micro Economics & Business Environment Course MaterialDocument30 pagesMicro Economics & Business Environment Course MaterialAnuNo ratings yet

- Basics of Business EconomicsDocument67 pagesBasics of Business EconomicsAnuNo ratings yet

- Basic ProblemsDocument17 pagesBasic ProblemsAnuNo ratings yet

- Agenda: Raveena Rajan Mba I Sem Batch ADocument16 pagesAgenda: Raveena Rajan Mba I Sem Batch AAnuNo ratings yet

- Balancesheet - MRF LTDDocument4 pagesBalancesheet - MRF LTDAnuNo ratings yet

- Applications of Spread SheetsDocument8 pagesApplications of Spread SheetsAnuNo ratings yet

- Date Issued: 05.19.2006 Number: 0530 Circular No. 530 Series of 2006Document1 pageDate Issued: 05.19.2006 Number: 0530 Circular No. 530 Series of 2006Jesse Myl MarciaNo ratings yet

- Francisco Partners CaseDocument32 pagesFrancisco Partners CaseJose M Terrés-NícoliNo ratings yet

- Consolidated Fund of India: The Accounts of Government Are Kept in Three PartsDocument1 pageConsolidated Fund of India: The Accounts of Government Are Kept in Three PartsAshok KumarNo ratings yet

- iMPORTANCE OF RATIO ANALYSISDocument2 pagesiMPORTANCE OF RATIO ANALYSISPremiNo ratings yet

- Program btc2bDocument2 pagesProgram btc2bbtc2b2No ratings yet

- Principles of AccountingDocument8 pagesPrinciples of AccountingDanish MuradNo ratings yet

- International Banking & Foreign Exchange ManagementDocument12 pagesInternational Banking & Foreign Exchange ManagementrumiNo ratings yet

- Transaction AcknowledgmentDocument9 pagesTransaction Acknowledgmentgirish geethuNo ratings yet

- LucidChart MarzoDocument2 pagesLucidChart MarzoHenry M Gutièrrez SNo ratings yet

- Ca Inter (Income Tax) Ca Vijender AggarwalDocument2 pagesCa Inter (Income Tax) Ca Vijender AggarwalMehul GuptaNo ratings yet

- ECON252 Midterm1 ExamDocument8 pagesECON252 Midterm1 ExamTu ShirotaNo ratings yet

- Política Monetaria en Un Entorno de Dos Monedas: Banco Central de Reserva Del PerúDocument39 pagesPolítica Monetaria en Un Entorno de Dos Monedas: Banco Central de Reserva Del PerúCristian Fernando Sanabria BautistaNo ratings yet

- Effect of Electronic Banking On The Economic Growth of Nigeria (2009-2018)Document24 pagesEffect of Electronic Banking On The Economic Growth of Nigeria (2009-2018)The IjbmtNo ratings yet

- International FinanceDocument181 pagesInternational FinanceadhishsirNo ratings yet

- Financial Analysis For Boa CoffeeDocument2 pagesFinancial Analysis For Boa CoffeeRunaway ShujiNo ratings yet

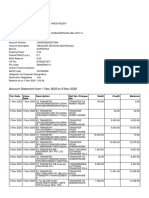

- Account Statement From 1 Nov 2020 To 9 Nov 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument2 pagesAccount Statement From 1 Nov 2020 To 9 Nov 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balancevinod reddyNo ratings yet

- The National Budget of Bangladesh: A Comparative StudyDocument48 pagesThe National Budget of Bangladesh: A Comparative StudyQuazi Aritra Reyan80% (25)

- 20220912-TEM-Tong's PortfolioDocument8 pages20220912-TEM-Tong's PortfolioMohd FadzilNo ratings yet

- Swabhimaan - Transforming Rural India Through Financial InclusionDocument2 pagesSwabhimaan - Transforming Rural India Through Financial Inclusionjohnyy2kNo ratings yet

- FIM Exercise AnsDocument6 pagesFIM Exercise AnsSam MNo ratings yet

- DRDOTendernotice 2 PDFDocument220 pagesDRDOTendernotice 2 PDFASRAR AHMED KHANNo ratings yet

- Midland Energy CaseDocument3 pagesMidland Energy CaseanilprasanthNo ratings yet

- Inside JobDocument3 pagesInside JobFrancheska Betancourt RiosNo ratings yet