You might also like

- Summary of Anthony Crescenzi's The Strategic Bond Investor, Third EditionFrom EverandSummary of Anthony Crescenzi's The Strategic Bond Investor, Third EditionNo ratings yet

- Classical Macroecon and Keynesian AggregateDocument23 pagesClassical Macroecon and Keynesian Aggregatessregens820% (1)

- The Conduct of Monetary Policy: Strategy and TacticsDocument26 pagesThe Conduct of Monetary Policy: Strategy and TacticsLazaros KarapouNo ratings yet

- The Conduct of Monetary Policy: Strategy and TacticsDocument26 pagesThe Conduct of Monetary Policy: Strategy and TacticsBradley RayNo ratings yet

- InflationDocument19 pagesInflationLinh Đỗ ThùyNo ratings yet

- Why Study Money, Banking, and Financial Markets?Document30 pagesWhy Study Money, Banking, and Financial Markets?Zəfər CabbarovNo ratings yet

- CH 16Document49 pagesCH 16Asya MammadovaNo ratings yet

- Why Study Money, Banking, and Financial Markets?Document29 pagesWhy Study Money, Banking, and Financial Markets?Lazaros KarapouNo ratings yet

- The Conduct of Monetary Policy: Strategy and TacticsDocument34 pagesThe Conduct of Monetary Policy: Strategy and TacticsAlejandroArnoldoFritzRuenesNo ratings yet

- Why Study Money, Banking, and Financial Markets?Document28 pagesWhy Study Money, Banking, and Financial Markets?Joe PatrickNo ratings yet

- Chapter 1 NotesDocument28 pagesChapter 1 NotesMaathir Al ShukailiNo ratings yet

- Chapter 1 NotesDocument28 pagesChapter 1 NotesMaathir Al ShukailiNo ratings yet

- Mishkin Chap 1Document29 pagesMishkin Chap 1Tricia KiethNo ratings yet

- Why Study Money, Banking, and Financial Markets?Document25 pagesWhy Study Money, Banking, and Financial Markets?Hafiz akbarNo ratings yet

- Why Study Money, Banking, and Financial Markets?Document25 pagesWhy Study Money, Banking, and Financial Markets?Ali El MallahNo ratings yet

- Nltcnh - Chapter 1 - Tiếng AnhDocument25 pagesNltcnh - Chapter 1 - Tiếng Anhphamthikieuanh1111No ratings yet

- 01 - Mish - Embfm7c - PPT - ch01 EditDocument28 pages01 - Mish - Embfm7c - PPT - ch01 Editginny HeNo ratings yet

- 1 - Why Study Money, Banking, and Financial Markets?Document25 pages1 - Why Study Money, Banking, and Financial Markets?cihtanbioNo ratings yet

- Why Study Money, Banking, and Financial Markets?Document25 pagesWhy Study Money, Banking, and Financial Markets?Ahmad RahhalNo ratings yet

- Why Study Money N BankingDocument25 pagesWhy Study Money N BankingJimmy TengNo ratings yet

- CH 15Document51 pagesCH 15lobsterkarlobbNo ratings yet

- Why Study Money, Banking, and Financial Markets?Document17 pagesWhy Study Money, Banking, and Financial Markets?Trang VũNo ratings yet

- Mishkin Econ12eGE CH17Document46 pagesMishkin Econ12eGE CH17josemourinhoNo ratings yet

- ch24 Mish11ge EmbfmDocument41 pagesch24 Mish11ge EmbfmRakib HasanNo ratings yet

- Blanchard Macro7e PPT 21Document18 pagesBlanchard Macro7e PPT 21eva gonzalez diazNo ratings yet

- CH08 Mish11ge EMBFMDocument19 pagesCH08 Mish11ge EMBFMZeeruanNo ratings yet

- Foreign Exchange Rate DeterminationDocument37 pagesForeign Exchange Rate DeterminationSonia Laksita ErbianitaNo ratings yet

- Why Study Money, Banking, and Financial Markets?Document31 pagesWhy Study Money, Banking, and Financial Markets?frostriskNo ratings yet

- Lecture of Mishkin CH 01Document31 pagesLecture of Mishkin CH 01Phuoc DangNo ratings yet

- The Economics of Money, Banking, and Financial Markets: Sixth Canadian EditionDocument28 pagesThe Economics of Money, Banking, and Financial Markets: Sixth Canadian Editionchristian rodriguexNo ratings yet

- CH10 Mish11ge EMBFMDocument23 pagesCH10 Mish11ge EMBFMZeeruanNo ratings yet

- ABEL10e Accessible Fullppt 01Document29 pagesABEL10e Accessible Fullppt 01Holly KSRNo ratings yet

- ESOM - Chapter 1 Course OverviewDocument24 pagesESOM - Chapter 1 Course OverviewLy KhanhNo ratings yet

- Ch01 ME For BlackboardDocument17 pagesCh01 ME For BlackboardIlqar SəlimovNo ratings yet

- Chap 1 Economics of Money and BankingDocument25 pagesChap 1 Economics of Money and BankingJason YoungNo ratings yet

- CHAPTER 6 ECO531 Monetary Policy - StudentsDocument28 pagesCHAPTER 6 ECO531 Monetary Policy - StudentsNasuha MusaNo ratings yet

- Chapter 24 Monetary Policy TheoryDocument39 pagesChapter 24 Monetary Policy TheoryTRAM NGUYEN NHU QUYNHNo ratings yet

- LN25Mish769581 10 LN25Document20 pagesLN25Mish769581 10 LN25Ali El MallahNo ratings yet

- Section VidDocument25 pagesSection Vidsailendra123No ratings yet

- Ch1 Why Study Banking & Financial InstitutionsDocument25 pagesCh1 Why Study Banking & Financial InstitutionsSam CincoNo ratings yet

- Chapter 11 Monetary Policy Lecture PresentationDocument21 pagesChapter 11 Monetary Policy Lecture PresentationalsinanhananNo ratings yet

- Lec 1 - Chap1&3Document38 pagesLec 1 - Chap1&3TACN-1TC-19ACN Luong Khanh LinhNo ratings yet

- Monetary and Financial Economics: 2 Année de La Grande Ecole de L'institut de RabatDocument28 pagesMonetary and Financial Economics: 2 Année de La Grande Ecole de L'institut de RabatIsmaîl TemsamaniNo ratings yet

- Chapter 8 An Economic Alaysis of Financiaal StructureDocument14 pagesChapter 8 An Economic Alaysis of Financiaal StructureSamanthaHandNo ratings yet

- CFO Macro12 PPT 14Document31 pagesCFO Macro12 PPT 14Pedro ValdiviaNo ratings yet

- InflationDocument13 pagesInflationThiên CầmNo ratings yet

- Schapter 14 Monetary Policy (Student)Document38 pagesSchapter 14 Monetary Policy (Student)mieraadzilahNo ratings yet

- Why Study Money, Banking and Financial Market?Document18 pagesWhy Study Money, Banking and Financial Market?jahangir tanveerNo ratings yet

- CH 01 PPTaccessibleDocument35 pagesCH 01 PPTaccessibleDaner DlawarNo ratings yet

- Why Study Money, Banking, and Financial Markets?Document12 pagesWhy Study Money, Banking, and Financial Markets?وائل مصطفىNo ratings yet

- Mishkin Econ13e PPT 15Document31 pagesMishkin Econ13e PPT 15quynhle.31221021604No ratings yet

- Macroeconomics 2nd Edition Hubbard Solutions ManualDocument24 pagesMacroeconomics 2nd Edition Hubbard Solutions Manuallanhlucfx1100% (32)

- POE 20 MacroeconomicsDocument47 pagesPOE 20 MacroeconomicsFiitjee RecordNo ratings yet

- Mishkin CH 01Document23 pagesMishkin CH 01Ehtsham Ul HaqNo ratings yet

- Financial Crises in Advanced EconomiesDocument29 pagesFinancial Crises in Advanced EconomiesZeeruanNo ratings yet

- CH 29Document25 pagesCH 29aamitabh3No ratings yet

- Stabilization Policies: - Reliance On Demand Management Policies inDocument13 pagesStabilization Policies: - Reliance On Demand Management Policies inPrateek KhandelwalNo ratings yet

- Chapter 4Document23 pagesChapter 4Jinnath JumurNo ratings yet

- Global Marketing: Ninth EditionDocument44 pagesGlobal Marketing: Ninth EditionOmar SanadNo ratings yet

- 2019 Jan 7 Lecture 2 and 3 Business EnvironmentDocument50 pages2019 Jan 7 Lecture 2 and 3 Business EnvironmentLevy LubindaNo ratings yet

- Macroeconomics EF204: Lecture #1Document23 pagesMacroeconomics EF204: Lecture #1AymanNo ratings yet

- Mitigating Risks in the Fertilizer Industry CaseDocument2 pagesMitigating Risks in the Fertilizer Industry CaseViệt NữNo ratings yet

- Bảng Tính Excel - Dataset and Data TableDocument14 pagesBảng Tính Excel - Dataset and Data TableViệt NữNo ratings yet

- 2.1. Key Answer To Question 2.1.Document3 pages2.1. Key Answer To Question 2.1.Việt NữNo ratings yet

- 16Document1 page16Việt NữNo ratings yet

- Financial Futures Markets: Chapter ObjectivesDocument22 pagesFinancial Futures Markets: Chapter ObjectivesViệt NữNo ratings yet

- Cafe DataDocument76 pagesCafe DataViệt NữNo ratings yet

- Acct 202 Ch1Document24 pagesAcct 202 Ch1Hieu DamNo ratings yet

- 16Document1 page16Việt NữNo ratings yet

- 1Document2 pages1Việt NữNo ratings yet

- Stock ValuationDocument28 pagesStock ValuationViệt NữNo ratings yet

- Behavior of Interest RateDocument28 pagesBehavior of Interest RateViệt NữNo ratings yet

- 16Document1 page16Việt NữNo ratings yet

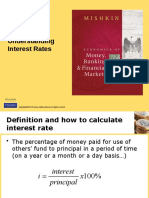

- Understanding Interest RateDocument42 pagesUnderstanding Interest RateViệt NữNo ratings yet

- Understanding Interest RateDocument42 pagesUnderstanding Interest RateViệt NữNo ratings yet

- Feeling Tea!: Presented by Group 1Document44 pagesFeeling Tea!: Presented by Group 1Việt NữNo ratings yet

- A2 Microeconomics Starter Pack 1Document36 pagesA2 Microeconomics Starter Pack 1cfranklin26.202No ratings yet

- Macroeconomics 15th Edition Mcconnell Solutions ManualDocument17 pagesMacroeconomics 15th Edition Mcconnell Solutions Manualdencuongpow5100% (24)

- The Grass Roots Process Housing. AlexanderDocument24 pagesThe Grass Roots Process Housing. AlexanderJosé Solís OpazoNo ratings yet

- Handouts and QuestionsDocument138 pagesHandouts and QuestionsJay Villegas ArmeroNo ratings yet

- BSP's Role in Promoting Price StabilityDocument14 pagesBSP's Role in Promoting Price StabilityJasmine LustadoNo ratings yet

- 2.3 Macroeconomic Objectives PDFDocument38 pages2.3 Macroeconomic Objectives PDFTita RachmawatiNo ratings yet

- ESSAY 10 MARKS (Eco120)Document5 pagesESSAY 10 MARKS (Eco120)husna azizanNo ratings yet

- ECON1102 Macroeconomics 1 CheatsheetDocument2 pagesECON1102 Macroeconomics 1 CheatsheetCarla MissionaNo ratings yet

- Whats Up Kwacha, by DR Aubrey Chibumba, CFADocument14 pagesWhats Up Kwacha, by DR Aubrey Chibumba, CFAsimusokwechristopherNo ratings yet

- UK Quarterly Marketbeat March 2016Document16 pagesUK Quarterly Marketbeat March 2016mannantawaNo ratings yet

- Lecture Notes On Macroeconomic Principles: Peter Ireland Department of Economics Boston CollegeDocument7 pagesLecture Notes On Macroeconomic Principles: Peter Ireland Department of Economics Boston CollegeQueny WongNo ratings yet

- How your kindergarten classroom impacts lifelong earningsDocument89 pagesHow your kindergarten classroom impacts lifelong earningsJoe OgleNo ratings yet

- GROUP 5 Ascension of Gasoline The Oil Price HikeDocument3 pagesGROUP 5 Ascension of Gasoline The Oil Price Hikeqy8rwv586mNo ratings yet

- Esd ModuleDocument131 pagesEsd ModuleNdumiso Moyo100% (1)

- Econometrics Assignment Regression AnalysisDocument15 pagesEconometrics Assignment Regression AnalysisHassan ChaudhryNo ratings yet

- Parguez - Dallo Stato Sociale Allo Stato Predatore (Anteprima) PDFDocument187 pagesParguez - Dallo Stato Sociale Allo Stato Predatore (Anteprima) PDFGiovanni GrecoNo ratings yet

- Ten Principles of EconomicsDocument8 pagesTen Principles of EconomicsJustine MelindoNo ratings yet

- Philippine Christian University: Dasmarinas CampusDocument15 pagesPhilippine Christian University: Dasmarinas CampusRobin Escoses MallariNo ratings yet

- CSN 20F 2015 EngDocument314 pagesCSN 20F 2015 EngPradnya SonarNo ratings yet

- Basic Cash Formulas Manual April 2009 - 2.8Document123 pagesBasic Cash Formulas Manual April 2009 - 2.8horns2034No ratings yet

- Solved PapersDocument167 pagesSolved Papersasfar08200% (1)

- Mathematics: Interest Rates and FinanceDocument55 pagesMathematics: Interest Rates and FinanceAmr Tarek100% (1)

- Monitoring Cycles, Jobs, and The Price LevelDocument42 pagesMonitoring Cycles, Jobs, and The Price LevelibarhimNo ratings yet

- 2023 Solar Risk Assessment FinalDocument21 pages2023 Solar Risk Assessment FinalFake EmailNo ratings yet

- Pak Mat Western Restaurant SWOT AnalysisDocument68 pagesPak Mat Western Restaurant SWOT AnalysisNurazira Sarman100% (1)

- Msdi - Alcala de Henares, SpainDocument4 pagesMsdi - Alcala de Henares, SpainDurgesh Nandini Mohanty100% (1)

- Assignment: Date: July 28, 2020Document18 pagesAssignment: Date: July 28, 2020arslanjaved690No ratings yet

- Test Bank For Macroeconomics Fifth Canadian Edition 5 e 5th Edition Olivier Blanchard David W JohnsonDocument8 pagesTest Bank For Macroeconomics Fifth Canadian Edition 5 e 5th Edition Olivier Blanchard David W Johnsonmarthaalexandra7xyfu1No ratings yet

- 1.1.1 Political StabilityDocument3 pages1.1.1 Political StabilityCuong VUongNo ratings yet