You might also like

- Define product cost componentsDocument5 pagesDefine product cost componentsKatrina DeveraNo ratings yet

- Product CostDocument2 pagesProduct CostEster MaulinaNo ratings yet

- Cost Sheet P&SDocument41 pagesCost Sheet P&SJishnuPatilNo ratings yet

- Cost ClassificationDocument19 pagesCost ClassificationMohammad Faizan Farooq Qadri Attari100% (1)

- Product CostDocument22 pagesProduct CostJINKY TOLENTINONo ratings yet

- Management Accounting Session 2 Cost Terms & Purposes: Indian Institute of Management RohtakDocument58 pagesManagement Accounting Session 2 Cost Terms & Purposes: Indian Institute of Management RohtakSiddharthNo ratings yet

- Lesson-13 Elements of Cost and Cost SheetDocument8 pagesLesson-13 Elements of Cost and Cost SheetMonika SinglaNo ratings yet

- Elements of Cost SheetDocument41 pagesElements of Cost Sheetapi-2701408994% (18)

- Lesson-13 Elements of Cost and Cost SheetDocument5 pagesLesson-13 Elements of Cost and Cost SheetSairam BhukyaNo ratings yet

- Ma Slide Ta Chap 19Document6 pagesMa Slide Ta Chap 19Le H KhangNo ratings yet

- Cost ClassificationDocument6 pagesCost ClassificationAnonymous yy8In96j0r100% (1)

- Manufacturing and Nonmanufacturing CostsDocument18 pagesManufacturing and Nonmanufacturing CostsBoulos Albert100% (1)

- Cost Classification - AnswersDocument64 pagesCost Classification - Answerssamreen iqbalNo ratings yet

- Inventory: COST OF PRODUCTIONDocument104 pagesInventory: COST OF PRODUCTIONHAFIZ MUHAMMAD UMAR FAROOQ RANANo ratings yet

- Cost Accounting Concepts: Prof. Dr. Farid MoharamDocument90 pagesCost Accounting Concepts: Prof. Dr. Farid Moharammohamed el kadyNo ratings yet

- Garment Costing: Minnie BastinDocument73 pagesGarment Costing: Minnie BastinBastinNo ratings yet

- Costing TheoryDocument5 pagesCosting TheoryShaji KuttyNo ratings yet

- Week 11 Manufacturing AccountDocument9 pagesWeek 11 Manufacturing AccountWeijianNo ratings yet

- Chapter 1 - Manufacturing AccountDocument32 pagesChapter 1 - Manufacturing AccountNORZAIHA BINTI ALI MoeNo ratings yet

- Manufacturing and Non Manufacturing CostsDocument26 pagesManufacturing and Non Manufacturing Costsrajaguru_s0% (2)

- MQE Cost Acctg Session 1Document78 pagesMQE Cost Acctg Session 1Frances Monique Alburo0% (1)

- COST ELEMENTS BREAKDOWNDocument9 pagesCOST ELEMENTS BREAKDOWNDaniel KerandiNo ratings yet

- Fashion Accessory Cost ComponentsDocument21 pagesFashion Accessory Cost ComponentsKim Laurence Mejia ReyesNo ratings yet

- Costs - Concepts and ClassificationsDocument5 pagesCosts - Concepts and ClassificationsCarlo B CagampangNo ratings yet

- Chapter 2 - Managerial Acc. & Cost ConceptsDocument23 pagesChapter 2 - Managerial Acc. & Cost ConceptsMuhammad Ali KazmiNo ratings yet

- COST Lesson 2Document4 pagesCOST Lesson 2Christian Clyde Zacal Ching0% (1)

- Cost Accounting: Direct, Variable, FixedDocument7 pagesCost Accounting: Direct, Variable, FixedMahnoor ChathaNo ratings yet

- Managerial Accounting ExamDocument3 pagesManagerial Accounting Examsaed abdiqafarNo ratings yet

- Elements of Cost: Manisha VermaDocument31 pagesElements of Cost: Manisha VermaPriyanshNo ratings yet

- Lec 02 Cost ClassificationsDocument97 pagesLec 02 Cost ClassificationsMd Shawfiqul IslamNo ratings yet

- Chapter 02Document57 pagesChapter 02Adam AbdullahiNo ratings yet

- Chapter 12 Cost Sheet or Statement of CostDocument16 pagesChapter 12 Cost Sheet or Statement of CostNeelesh MishraNo ratings yet

- Cost_Classifications__167083589515669092976396eeb75c11aDocument16 pagesCost_Classifications__167083589515669092976396eeb75c11a22je0766No ratings yet

- Cost AnalysisDocument36 pagesCost AnalysisHarisagar ThulasiramanNo ratings yet

- Cost SheetDocument5 pagesCost SheetDilip ChenaniNo ratings yet

- Cost and Supply Analysis - Unit 1Document12 pagesCost and Supply Analysis - Unit 1PethurajNo ratings yet

- Chapter TwoDocument33 pagesChapter TwoTerefe DubeNo ratings yet

- Acc GR 11 T4 Week 1&2 Manuftring Costs ENGDocument4 pagesAcc GR 11 T4 Week 1&2 Manuftring Costs ENGsihlemooi3No ratings yet

- Cost Classification Theory and Practice QuestionsDocument9 pagesCost Classification Theory and Practice QuestionsBilal Rauf100% (1)

- Product Cost Flows and Business OrganizationsDocument48 pagesProduct Cost Flows and Business OrganizationsGaluh Boga KuswaraNo ratings yet

- Chapter 3 - Virtual - Classroom-M.Document61 pagesChapter 3 - Virtual - Classroom-M.rebeccahf7No ratings yet

- Manufacturing Cost BreakdownDocument4 pagesManufacturing Cost BreakdownAwais TauseefNo ratings yet

- Topics 2 Product CostsDocument2 pagesTopics 2 Product CostssameerhaNo ratings yet

- Elements of CostDocument38 pagesElements of CostRajyalakshmi.GNo ratings yet

- Elementary Cost Concepts ExplainedDocument15 pagesElementary Cost Concepts ExplainedExa AkbarNo ratings yet

- Chapter 1 - Manufacturing Account (I)Document16 pagesChapter 1 - Manufacturing Account (I)NG JIA LUNGNo ratings yet

- Manufacturing Business - Costing Methods and Financial StatementsDocument4 pagesManufacturing Business - Costing Methods and Financial StatementsVISITACION JAIRUS GWENNo ratings yet

- Cost Accounting: Introduction To Cost Accounting Lecture-1 Jameel A Khan HakroDocument35 pagesCost Accounting: Introduction To Cost Accounting Lecture-1 Jameel A Khan Hakrokashif aliNo ratings yet

- CostDocument27 pagesCostAbid AliNo ratings yet

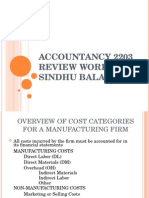

- Accountancy 2203 Review Workshop Sindhu BalaDocument27 pagesAccountancy 2203 Review Workshop Sindhu BalaAnna Mae SanchezNo ratings yet

- Manufacturing ManagementDocument126 pagesManufacturing ManagementSIDDHARTH JHANo ratings yet

- Session 8 - PGDM 2021-23Document36 pagesSession 8 - PGDM 2021-23Krishnapriya NairNo ratings yet

- Manufacturing and Non-Manufacturing CostDocument4 pagesManufacturing and Non-Manufacturing CostLaghari ShafquatNo ratings yet

- Cost Accounting Updated VersionDocument128 pagesCost Accounting Updated VersionTct TurgutNo ratings yet

- Cost Terms, Concepts, and Classifications: UAA - ACCT 202 Principles of Managerial Accounting Dr. Fred BarbeeDocument41 pagesCost Terms, Concepts, and Classifications: UAA - ACCT 202 Principles of Managerial Accounting Dr. Fred BarbeeBlerim HalimiNo ratings yet

- Management Accounting: Product CostingDocument22 pagesManagement Accounting: Product CostingDaksh AnejaNo ratings yet

- CHAPTER 2 Cost Terms and PurposeDocument31 pagesCHAPTER 2 Cost Terms and PurposeRose McMahonNo ratings yet

- Cost Analysis, Concepts & ClassificationsDocument43 pagesCost Analysis, Concepts & Classificationsmarget85% (13)

- Manufacturing Wastes Stream: Toyota Production System Lean Principles and ValuesFrom EverandManufacturing Wastes Stream: Toyota Production System Lean Principles and ValuesRating: 4.5 out of 5 stars4.5/5 (3)

- RAW MaterialsDocument6 pagesRAW MaterialsShawn MendesNo ratings yet

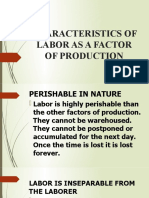

- Characteristics of Labor As A Factor of ProductionDocument8 pagesCharacteristics of Labor As A Factor of ProductionShawn MendesNo ratings yet

- 3.5 Part 1Document15 pages3.5 Part 1Shawn MendesNo ratings yet

- Goal of Capacity PlanningDocument11 pagesGoal of Capacity PlanningShawn MendesNo ratings yet

- Repairs and MaintenanceDocument10 pagesRepairs and MaintenanceShawn MendesNo ratings yet

- 3.1 Part 1Document16 pages3.1 Part 1Shawn MendesNo ratings yet

- Plant Layout Principles and Types GuideDocument90 pagesPlant Layout Principles and Types GuideShawn MendesNo ratings yet

- 3.1 Part 2Document12 pages3.1 Part 2Shawn MendesNo ratings yet

- Fixed CapitalDocument10 pagesFixed CapitalShawn MendesNo ratings yet

- IntroductionDocument2 pagesIntroductionShawn MendesNo ratings yet

- IntroductionDocument2 pagesIntroductionShawn MendesNo ratings yet

- Resultant: No Motion (STATICS) Changing Motion (DYNAMICS)Document1 pageResultant: No Motion (STATICS) Changing Motion (DYNAMICS)Shawn MendesNo ratings yet

- Eng Econ SlidesDocument34 pagesEng Econ Slidesاحمد عمر حديدNo ratings yet

- Customer-Centricity in Retail BankingDocument17 pagesCustomer-Centricity in Retail BankingMadalina PopescuNo ratings yet

- GTP&DWG of - Earthing Pipe& Earth RodDocument6 pagesGTP&DWG of - Earthing Pipe& Earth RodabhishekNo ratings yet

- Keith Dawson (Author) - The Call Center Handbook-CRC Press (2007)Document283 pagesKeith Dawson (Author) - The Call Center Handbook-CRC Press (2007)aaati100% (1)

- As 116941 Im-H3ee RM 96M16412 WW GB 2021 2 PDFDocument332 pagesAs 116941 Im-H3ee RM 96M16412 WW GB 2021 2 PDFPierre-Olivier MouthuyNo ratings yet

- Revit Structure 4 User GuideDocument728 pagesRevit Structure 4 User GuidehernawanmhNo ratings yet

- Event Tree Analysis ExplainedDocument13 pagesEvent Tree Analysis Explainedananthu.u100% (1)

- Merchandising - Journal EntriesDocument3 pagesMerchandising - Journal EntriesBhea Ballesteros CabasanNo ratings yet

- PA System Design GuideDocument68 pagesPA System Design GuideBob Pierce100% (1)

- Tarea 3 Customer ServiceDocument17 pagesTarea 3 Customer ServicetonyNo ratings yet

- Daily Construction Report (DCR) : Project ManagerDocument5 pagesDaily Construction Report (DCR) : Project ManagerMoath AlhajiriNo ratings yet

- What Is The APICS CPIM CertificationDocument6 pagesWhat Is The APICS CPIM CertificationDina EleyanNo ratings yet

- Argus 20230518fmbsulDocument15 pagesArgus 20230518fmbsulngi-moscowNo ratings yet

- Audit of LiabilitiesDocument5 pagesAudit of LiabilitiesMenacexgNo ratings yet

- Ebook-ENG-The Ultimate Guide For Visas in Australia-Go Study Australia-1Document41 pagesEbook-ENG-The Ultimate Guide For Visas in Australia-Go Study Australia-1Mico de LeonNo ratings yet

- Step by Step Guide: Online Process of APEDA RegistrationDocument6 pagesStep by Step Guide: Online Process of APEDA RegistrationNandaniNo ratings yet

- HSP Faisal Hannan CVDocument3 pagesHSP Faisal Hannan CVmba2135156No ratings yet

- Slots, Tables, and All That Jazz: Managing Customer Profitability at MGM Grand Hotel (Do All The Questions)Document3 pagesSlots, Tables, and All That Jazz: Managing Customer Profitability at MGM Grand Hotel (Do All The Questions)Ankita jainNo ratings yet

- Steel Authority of India LimitedDocument28 pagesSteel Authority of India LimitedAbhishek VishwaNo ratings yet

- San Miguel Drink Behavior Final Exam - Goedings - MarollanoDocument11 pagesSan Miguel Drink Behavior Final Exam - Goedings - MarollanoDrakon BgNo ratings yet

- LMC Global Sugar Strategic View 2020 Brochure 1Document17 pagesLMC Global Sugar Strategic View 2020 Brochure 1Ahmed OuhniniNo ratings yet

- 1 Annual Tanglaw Cup Case Study CompetitionDocument2 pages1 Annual Tanglaw Cup Case Study CompetitionDominic Dela VegaNo ratings yet

- Literature @jun-2020 MODIFIEDDocument26 pagesLiterature @jun-2020 MODIFIEDEng-Mukhtaar CatooshNo ratings yet

- Consumer Behavior 12th Edition Schiffman Test BankDocument31 pagesConsumer Behavior 12th Edition Schiffman Test Bankrowanbridgetuls3100% (24)

- National Teachers College ManilaDocument6 pagesNational Teachers College ManilaJeline LensicoNo ratings yet

- Module - 1 Working Capital Management: MeaningDocument30 pagesModule - 1 Working Capital Management: MeaningumeshrathoreNo ratings yet

- DOH vs Phillip Morris: SC rules on constitutionality of tobacco promotion banDocument15 pagesDOH vs Phillip Morris: SC rules on constitutionality of tobacco promotion banPaul ToguayNo ratings yet

- Que For PG 98 Equity Val NotesDocument3 pagesQue For PG 98 Equity Val Notesrahul.modi18No ratings yet

- KYC InglesDocument2 pagesKYC InglesJakeNo ratings yet

- EE-SX1115: Photomicrosensor (Transmissive)Document4 pagesEE-SX1115: Photomicrosensor (Transmissive)Alejo RamirezNo ratings yet

- India's Balance of Payments Crisis and It's ImpactsDocument62 pagesIndia's Balance of Payments Crisis and It's ImpactsAkhil RupaniNo ratings yet