You might also like

- Breath of Life Attunement (Self Attunement)Document4 pagesBreath of Life Attunement (Self Attunement)Petrea CiortanNo ratings yet

- Monitoring Training PDFDocument264 pagesMonitoring Training PDFDiego Rojo100% (6)

- It Is Finished - John 19 30Document4 pagesIt Is Finished - John 19 30payasrommelNo ratings yet

- BMC Ent530 ReportDocument20 pagesBMC Ent530 ReportAinnur Haziqah100% (3)

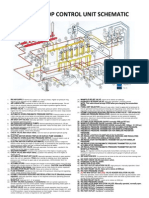

- Koomey Unit-53 Items - A3Document1 pageKoomey Unit-53 Items - A3Jayaprakash Gopala Kamath83% (6)

- Assignment HBEF3703 Introduction To Guidance and Counselling / May 2020 SemesterDocument8 pagesAssignment HBEF3703 Introduction To Guidance and Counselling / May 2020 SemesterSteve SimonNo ratings yet

- Fairview Terminal PhaseII Expansion Project Report - Oct2012Document436 pagesFairview Terminal PhaseII Expansion Project Report - Oct2012NewsroomNo ratings yet

- Corporate BankingDocument21 pagesCorporate BankingPadma NarayananNo ratings yet

- Shariah-Compliant E-Wallet Prospects & Challenges (28 October 2020 ISRA Consulting)Document51 pagesShariah-Compliant E-Wallet Prospects & Challenges (28 October 2020 ISRA Consulting)Abdul Aziz Mohd Nor100% (1)

- Module 3 Docket SystemDocument26 pagesModule 3 Docket SystemGinoong Kim GalvezNo ratings yet

- Islamic Commercial BankingDocument26 pagesIslamic Commercial BankingjmfaleelNo ratings yet

- Banking Is Described As The Business of Taking and Securing Money Held by Other People and CompaniesDocument8 pagesBanking Is Described As The Business of Taking and Securing Money Held by Other People and CompaniesTasnim ZaraNo ratings yet

- A Study On Bank of Maharashtra: Commercial Banking SystemDocument13 pagesA Study On Bank of Maharashtra: Commercial Banking SystemGovind N VNo ratings yet

- Banking Retail ProductsDocument7 pagesBanking Retail ProductsaadisssNo ratings yet

- Accelerate Innovation.: Strengthen Your CoreDocument12 pagesAccelerate Innovation.: Strengthen Your CoreMarthaNo ratings yet

- Audit of Banks - July 8, 2022Document29 pagesAudit of Banks - July 8, 2022Bea Garcia100% (1)

- Book - Credit Monitoring & NPA - 31!3!2013Document172 pagesBook - Credit Monitoring & NPA - 31!3!2013Manoj KularNo ratings yet

- Overview of Lending Activity: by Dr. Ashok K. DubeyDocument19 pagesOverview of Lending Activity: by Dr. Ashok K. DubeySmitha R AcharyaNo ratings yet

- Corporate Banking of IciciDocument38 pagesCorporate Banking of Iciciscribd_lostandfoundNo ratings yet

- 2017 McKinsey Payments Report PDFDocument16 pages2017 McKinsey Payments Report PDFnihar shethNo ratings yet

- Retail Banking Training MaterialDocument96 pagesRetail Banking Training MaterialTemesgen DentamoNo ratings yet

- Customer Service in Banks - RBI RulesDocument15 pagesCustomer Service in Banks - RBI RulesRAMESHBABUNo ratings yet

- MFG Technical Design Guide FRP Composite 0Document25 pagesMFG Technical Design Guide FRP Composite 0thiyakiNo ratings yet

- Introduction To Treasury and Funds Management 27-11-2018Document51 pagesIntroduction To Treasury and Funds Management 27-11-2018faisal_sarwar82No ratings yet

- Cash Management ServicesDocument23 pagesCash Management Servicessanjay_sbi100% (1)

- Banks, Banking & Retail Banking Services: Prepared By:: Mithun ShankarDocument56 pagesBanks, Banking & Retail Banking Services: Prepared By:: Mithun Shankardevendrachoudhary_upscNo ratings yet

- Customer Service PolicyDocument26 pagesCustomer Service PolicyThol Lyna100% (1)

- UNIT 2 - 16th September 2020Document42 pagesUNIT 2 - 16th September 2020GracyNo ratings yet

- Fs Revolutionizing Corp Lending Digital World WPDocument10 pagesFs Revolutionizing Corp Lending Digital World WPRishi SrivastavaNo ratings yet

- Chapter 1 - Introduction To Digital Banking - V1.0Document17 pagesChapter 1 - Introduction To Digital Banking - V1.0prabhjinderNo ratings yet

- 3branch Teller Training Manual 1. 6Document31 pages3branch Teller Training Manual 1. 6Ashenafi GirmaNo ratings yet

- Lobbyworks 4.0 PDFDocument8 pagesLobbyworks 4.0 PDFMohammed FaisalNo ratings yet

- Best Practices in Digital RadiographyDocument30 pagesBest Practices in Digital RadiographyJulian HutabaratNo ratings yet

- Tecnology in BankingDocument6 pagesTecnology in BankingShakthi RaghaviNo ratings yet

- Cash Management SolutionsDocument6 pagesCash Management SolutionsNavin ChoudharyNo ratings yet

- JBL Full - S. M. Abdul MukitDocument50 pagesJBL Full - S. M. Abdul MukithabibNo ratings yet

- 12 Chapter 9 - Risk Management in Banks NBFCsDocument4 pages12 Chapter 9 - Risk Management in Banks NBFCsgarima_kukreja_dceNo ratings yet

- Presentation MSME Products 24092018 - Ver 1Document52 pagesPresentation MSME Products 24092018 - Ver 1Murali KrishnanNo ratings yet

- Banking Solutions A Transition From Manual System To CBSDocument13 pagesBanking Solutions A Transition From Manual System To CBSPravah ShuklaNo ratings yet

- Internship Report UBL6Document125 pagesInternship Report UBL6dilhNo ratings yet

- ACBS Commercial Loan System Fact SheetDocument4 pagesACBS Commercial Loan System Fact SheetRajitNo ratings yet

- The Term Alternate Delivery ChannelDocument4 pagesThe Term Alternate Delivery ChannelIftekhar Abid Fahim100% (1)

- CAIIB Retail Products Module B Retail Banking PDFDocument29 pagesCAIIB Retail Products Module B Retail Banking PDFmansiNo ratings yet

- Cash Reserve RatioDocument40 pagesCash Reserve RatioMinal DalviNo ratings yet

- CHAP - 03 - Managing and Pricing Deposit ServicesDocument60 pagesCHAP - 03 - Managing and Pricing Deposit ServicesTran Thanh NganNo ratings yet

- Pradhanmantri Jan Dhan Yojana: Finatix Club IIM RaipurDocument10 pagesPradhanmantri Jan Dhan Yojana: Finatix Club IIM RaipurYadvendra YadavNo ratings yet

- Emergence of Doorstep Banking - Merits and DemeritsDocument11 pagesEmergence of Doorstep Banking - Merits and Demeritsmani100% (1)

- Dovetail Research - 2016 Value of InstantDocument19 pagesDovetail Research - 2016 Value of InstantHitesh ThakkarNo ratings yet

- Caiib BFM Module D NotesDocument36 pagesCaiib BFM Module D NotesA Man TA100% (1)

- A Research Paper On RBI Branch Licensing Policy: "Branching" The Gap Between FinancialDocument13 pagesA Research Paper On RBI Branch Licensing Policy: "Branching" The Gap Between Financialgayatrimohanty05No ratings yet

- Banker Customer RelationshipDocument13 pagesBanker Customer RelationshipFahimAnwarNo ratings yet

- Loans &advances (Mantu) - Project - 1-2Document48 pagesLoans &advances (Mantu) - Project - 1-2Shivu BaligeriNo ratings yet

- Retail Banking Products and ServicesDocument17 pagesRetail Banking Products and ServicesAneesha AkhilNo ratings yet

- Islamic Treasury Risk Management ProductsDocument4 pagesIslamic Treasury Risk Management ProductsjjangguNo ratings yet

- DNS Bank (Saurabh)Document25 pagesDNS Bank (Saurabh)Shoumi MahapatraNo ratings yet

- Post-Dated Cheques in The UAE - The Pros and ConsDocument4 pagesPost-Dated Cheques in The UAE - The Pros and Consfortune xiuNo ratings yet

- Housing Finance FMG18YDocument80 pagesHousing Finance FMG18YMadhusudan PartaniNo ratings yet

- Unit-1 The Micro-Small and Medium Enterprises (Msmes) Are Small Sized Entities, Defined inDocument36 pagesUnit-1 The Micro-Small and Medium Enterprises (Msmes) Are Small Sized Entities, Defined inBhaskaran BalamuraliNo ratings yet

- Sahay GeM On CredAll SiteDocument12 pagesSahay GeM On CredAll SiteManvi Pareek100% (1)

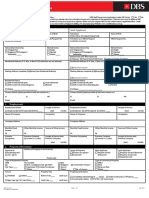

- DBS Mortgage All-In-One Application Form 2016Document3 pagesDBS Mortgage All-In-One Application Form 2016Viola HippieNo ratings yet

- KYC New ProjectDocument42 pagesKYC New ProjectNisha RathoreNo ratings yet

- Pssbooklet PDFDocument142 pagesPssbooklet PDFForkLogNo ratings yet

- Service Charges and FeesDocument10 pagesService Charges and FeesBella BishaNo ratings yet

- Pool Management: Muhammad Zeeshan Khan Product Manager Summit Bank Islamic EmailDocument31 pagesPool Management: Muhammad Zeeshan Khan Product Manager Summit Bank Islamic EmailAsad MemonNo ratings yet

- Defining Provisioning Coverage Ratio-VRK100-05Oct2011Document2 pagesDefining Provisioning Coverage Ratio-VRK100-05Oct2011RamaKrishna Vadlamudi, CFANo ratings yet

- Promotion Study Material PDFDocument271 pagesPromotion Study Material PDFsunil25150% (2)

- Interest Rate & Role of BNMDocument57 pagesInterest Rate & Role of BNMAinnur HaziqahNo ratings yet

- Banking Products & Services IIDocument39 pagesBanking Products & Services IIAinnur HaziqahNo ratings yet

- Banking Regulation & Management 1Document2 pagesBanking Regulation & Management 1Ainnur HaziqahNo ratings yet

- Lab Assignment 1Document3 pagesLab Assignment 1Ainnur HaziqahNo ratings yet

- Agricultural Revolution - Industrial RevolutionDocument2 pagesAgricultural Revolution - Industrial RevolutionJenni SilvaNo ratings yet

- Thesis Statement Arranged MarriagesDocument5 pagesThesis Statement Arranged Marriageskimberlypattersoncoloradosprings100% (2)

- Computer Networks TCP Congestion Control 1Document43 pagesComputer Networks TCP Congestion Control 1bavobavoNo ratings yet

- Wilms Tumor Hank Baskin, MDDocument11 pagesWilms Tumor Hank Baskin, MDPraktekDokterMelatiNo ratings yet

- U-Bolts For PolesDocument11 pagesU-Bolts For PolesMosa Elnaid ElnaidNo ratings yet

- All Progressive Circle Wise & Cadar Wise Summery Status 01-03-2024Document25 pagesAll Progressive Circle Wise & Cadar Wise Summery Status 01-03-2024vivekNo ratings yet

- Enable Root Access openSUSEDocument4 pagesEnable Root Access openSUSEAgung PambudiNo ratings yet

- HVDC Ground ElectrodeDocument13 pagesHVDC Ground ElectrodeHeather CarterNo ratings yet

- Transformers: Engr. Michael Ernie F. Rodriguez Instructor IDocument18 pagesTransformers: Engr. Michael Ernie F. Rodriguez Instructor IAndrew Montegrejo BarcomaNo ratings yet

- CRANE MERCHANDISING SYSTEMS (AKA DIXIE-NARCO) DN-501E LandscapeDocument33 pagesCRANE MERCHANDISING SYSTEMS (AKA DIXIE-NARCO) DN-501E LandscapeAnderson MachadoNo ratings yet

- أساليب البلاغة في سورة الملكDocument24 pagesأساليب البلاغة في سورة الملكjihan pyramida50% (2)

- Charge Coupled Device (CCD) : Presented byDocument18 pagesCharge Coupled Device (CCD) : Presented byBE CAREFULNo ratings yet

- MAKS Kenpark Schematic 31-03-2018-ModelDocument1 pageMAKS Kenpark Schematic 31-03-2018-Modelibti nabilNo ratings yet

- Neil Armstrong BiographyDocument4 pagesNeil Armstrong Biographyapi-232002863No ratings yet

- Hristo Boev ShumenRevisedDocument6 pagesHristo Boev ShumenRevisedHristo BoevNo ratings yet

- IXL - Fifth Grade Language Arts PracticeDocument3 pagesIXL - Fifth Grade Language Arts PracticeJanderson Barroso0% (1)

- Coral Reef Restoration A Guide To EffectDocument56 pagesCoral Reef Restoration A Guide To EffectDavid Higuita RamirezNo ratings yet

- Modicon M251 - Programming Guide EIO0000003089.02Document270 pagesModicon M251 - Programming Guide EIO0000003089.02mariookkNo ratings yet

- 500kVA Dyn5Document1 page500kVA Dyn5edwardNo ratings yet

- Camping-Safety LP-FF Crossword PDFDocument3 pagesCamping-Safety LP-FF Crossword PDFgreisannNo ratings yet

- In Uence of Fatigue Loading in Shear Failures of Reinforced Concrete Members Without Transverse ReinforcementDocument14 pagesIn Uence of Fatigue Loading in Shear Failures of Reinforced Concrete Members Without Transverse ReinforcementSai CharanNo ratings yet