You might also like

- Internal Control of Fixed Assets: A Controller and Auditor's GuideFrom EverandInternal Control of Fixed Assets: A Controller and Auditor's GuideRating: 4 out of 5 stars4/5 (1)

- Kelompok 5 Chapter 9 EditedDocument38 pagesKelompok 5 Chapter 9 EditedFathiyah AdilahNo ratings yet

- PB6MAT+Chapter 9 - Property, Plant & EquipmentDocument26 pagesPB6MAT+Chapter 9 - Property, Plant & EquipmentTirza NaomiNo ratings yet

- Fixed Assets Management PDFDocument20 pagesFixed Assets Management PDFDnukumNo ratings yet

- Far 17 Investment PropertyDocument12 pagesFar 17 Investment PropertyTeresaNo ratings yet

- IAS 36 ImpairmentDocument9 pagesIAS 36 ImpairmentDaniyal AhmedNo ratings yet

- Prepared by Nitin S PoojaryDocument36 pagesPrepared by Nitin S PoojaryAmit GoyalNo ratings yet

- 06 Intangible AssetsDocument57 pages06 Intangible Assets林義哲No ratings yet

- Fundamentals of Accounting PART IIDocument32 pagesFundamentals of Accounting PART IIJoshua Jay JesuroNo ratings yet

- Glossary of Terms for International Valuation StandardsDocument112 pagesGlossary of Terms for International Valuation StandardsMonica SimaNo ratings yet

- Learning Outcomes: After Studying This Chapter, Students Should Be Able ToDocument12 pagesLearning Outcomes: After Studying This Chapter, Students Should Be Able ToNUR SYAZANI MUHAMMADNo ratings yet

- Conceptual Framework of AccountingDocument28 pagesConceptual Framework of AccountingNahian HasanNo ratings yet

- 20187-378 - Quick Reference Guide ValuationDocument11 pages20187-378 - Quick Reference Guide Valuationvikas@davimNo ratings yet

- Accounting Charts - Quick Referencer by ICAIDocument22 pagesAccounting Charts - Quick Referencer by ICAIQuestion Bank100% (1)

- 44 Ind AS 102 Share Based Payment 1201Document87 pages44 Ind AS 102 Share Based Payment 1201Ahmed MadhaNo ratings yet

- Chapter 17 IAS 36 Impairment of AssetsDocument13 pagesChapter 17 IAS 36 Impairment of AssetsKelvin Chu JYNo ratings yet

- 18 AIS 012 (MD Jubayed Hossen)Document9 pages18 AIS 012 (MD Jubayed Hossen)Md JubayedNo ratings yet

- Pas 16Document32 pagesPas 16kiema katsutoNo ratings yet

- PSBA - Property, Plant and EquipmentDocument13 pagesPSBA - Property, Plant and EquipmentAbdulmajed Unda MimbantasNo ratings yet

- Chapter 21Document25 pagesChapter 21Charissa Cecile HaberNo ratings yet

- PAS 1 Presentation of Financial StatementsDocument4 pagesPAS 1 Presentation of Financial StatementsLary Lou Ventura100% (14)

- Session 8 (22nd Oct)Document122 pagesSession 8 (22nd Oct)zf8dkk8fnzNo ratings yet

- Concepts of Capital Maintenance in Fair Value AccountingDocument6 pagesConcepts of Capital Maintenance in Fair Value AccountingDISEREE AMOR ATIENZANo ratings yet

- Unit 2: Indian Accounting Standard 16: Property, Plant and EquipmentDocument52 pagesUnit 2: Indian Accounting Standard 16: Property, Plant and EquipmentHitesh Karmur100% (1)

- Balance Sheet BasicsDocument20 pagesBalance Sheet BasicsSarbani Mishra0% (1)

- Framework For Preparation and Presentation of Financial StatementsDocument5 pagesFramework For Preparation and Presentation of Financial Statementssamartha umbareNo ratings yet

- 1.1 PAS 1 Chapter 2 Summary (SFP)Document2 pages1.1 PAS 1 Chapter 2 Summary (SFP)Deviane CalabriaNo ratings yet

- Accounting 2Document7 pagesAccounting 2Valentina SerratoreNo ratings yet

- CAF 1 SupplementsDocument36 pagesCAF 1 SupplementsAb WasayNo ratings yet

- Final SummaryDocument6 pagesFinal SummaryAkanksha singhNo ratings yet

- CA Notes Concept and Accounting of Depreciation PDFDocument36 pagesCA Notes Concept and Accounting of Depreciation PDFBijay Aryan Dhakal100% (2)

- Chapter 15 Miscellaneous TopicsDocument6 pagesChapter 15 Miscellaneous TopicsAngelica Joy ManaoisNo ratings yet

- Tcevha 2015 Audited Fs and Notes 1 1Document12 pagesTcevha 2015 Audited Fs and Notes 1 1Rogerick LeabresNo ratings yet

- Summer 2013 5Document4 pagesSummer 2013 5TiNo ratings yet

- Conceptual Framework IFRS 2022Document27 pagesConceptual Framework IFRS 2022Ánh Nguyễn Thị NgọcNo ratings yet

- 66705studentjournal-Oct2021a (1) - Removed MadarDocument20 pages66705studentjournal-Oct2021a (1) - Removed MadarTimepass MungfuliNo ratings yet

- Ind AS 109Document47 pagesInd AS 109Savin Avaran SajanNo ratings yet

- Indian Accounting Standard 16: Property, Plant and EquipmentDocument47 pagesIndian Accounting Standard 16: Property, Plant and Equipmentmanoj rajeev ram gNo ratings yet

- Basic Accounting ReviewDocument75 pagesBasic Accounting ReviewSofie SergioNo ratings yet

- P 2Document4 pagesP 2Julious CaalimNo ratings yet

- Summary PpeDocument8 pagesSummary PpeJenilyn CalaraNo ratings yet

- Unit 2 Conceptual Framework SlidesDocument18 pagesUnit 2 Conceptual Framework SlidesNandi MliloNo ratings yet

- Conceptual Framework OverviewDocument6 pagesConceptual Framework OverviewRendra SeptikoNo ratings yet

- Accounting PPT - Intangible AssetDocument58 pagesAccounting PPT - Intangible AssetGokul RamNo ratings yet

- IMS Proschool IFRS EbookDocument143 pagesIMS Proschool IFRS EbookhariinshrNo ratings yet

- Ias 16 Property, Plant & Equipment: Adeel SaleemDocument20 pagesIas 16 Property, Plant & Equipment: Adeel SaleemAtif RehmanNo ratings yet

- Conceptual Framework (Part 2) : AssetsDocument3 pagesConceptual Framework (Part 2) : AssetsEui KimNo ratings yet

- Name of The Company: Financial Statement of The Year: 2012 & 2016Document5 pagesName of The Company: Financial Statement of The Year: 2012 & 2016Den XNo ratings yet

- Ipsas 23: Revenue From Non Exchange TransactionsDocument11 pagesIpsas 23: Revenue From Non Exchange TransactionsHace AdisNo ratings yet

- APC 403 PFRS For SEs (Section 1-2)Document3 pagesAPC 403 PFRS For SEs (Section 1-2)AnnSareineMamadesNo ratings yet

- Concept and Accounting of Depreciation: Learning OutcomesDocument35 pagesConcept and Accounting of Depreciation: Learning OutcomesShristiNo ratings yet

- MODULE_2_NotesDocument2 pagesMODULE_2_NotesJoshua AlvarezNo ratings yet

- FABM2-Chapter 1Document31 pagesFABM2-Chapter 1Marjon GarabelNo ratings yet

- Ques. 1. Peterlee (A) - Purpose and Authoritative Status of The FrameworkDocument7 pagesQues. 1. Peterlee (A) - Purpose and Authoritative Status of The FrameworkJulet Harris-TopeyNo ratings yet

- IAS Mình T So NDocument75 pagesIAS Mình T So NĐông VyNo ratings yet

- Presentation of Assets and LiabilitiesDocument8 pagesPresentation of Assets and LiabilitiesMichael AquinoNo ratings yet

- Study Note 1.2, Page 12 32Document21 pagesStudy Note 1.2, Page 12 32s4sahithNo ratings yet

- FRR Part C Accounting 04Document5 pagesFRR Part C Accounting 04Sarthak GargNo ratings yet

- 55002bosfndnov19 p1 cp5Document35 pages55002bosfndnov19 p1 cp5Priti Daga100% (1)

- Basic Financial Accounting and Reporting (Bfar) : Philippine Based (Summary and Class Notes)Document22 pagesBasic Financial Accounting and Reporting (Bfar) : Philippine Based (Summary and Class Notes)LiaNo ratings yet

- Akuntansi BiayaDocument4 pagesAkuntansi BiayaIdha RahmaNo ratings yet

- 4th Assignment Idha Rahma 19080304009Document2 pages4th Assignment Idha Rahma 19080304009Idha RahmaNo ratings yet

- 4th Assignment Idha Rahma 19080304009Document2 pages4th Assignment Idha Rahma 19080304009Idha RahmaNo ratings yet

- Agency Theory and Its Impacts on Business PracticesDocument2 pagesAgency Theory and Its Impacts on Business PracticesIdha RahmaNo ratings yet

- VRIO Analysis of Nike ResourcesDocument3 pagesVRIO Analysis of Nike ResourcesIdha RahmaNo ratings yet

- Final Project Group 9THDocument32 pagesFinal Project Group 9THIdha RahmaNo ratings yet

- ABC activity levels and cost driversDocument6 pagesABC activity levels and cost driversIdha RahmaNo ratings yet

- Final Project Group 9THDocument32 pagesFinal Project Group 9THIdha RahmaNo ratings yet

- Case Study CVP AnalysisDocument6 pagesCase Study CVP AnalysisIdha RahmaNo ratings yet

- Book HSRP appointment onlineDocument1 pageBook HSRP appointment onlineѕᴀcнιn ѕᴀιnιNo ratings yet

- Truth in Lending ActDocument2 pagesTruth in Lending ActGabieNo ratings yet

- REPORTINGDocument8 pagesREPORTINGMUHAMMAD HUMZANo ratings yet

- Future of Robo Advisory Platform in IndiaDocument17 pagesFuture of Robo Advisory Platform in IndiaVignesh ShanmugamNo ratings yet

- The Role of Financial Markets and Institutions in Supporting The Global Economy During The COVID 19 PandemicDocument60 pagesThe Role of Financial Markets and Institutions in Supporting The Global Economy During The COVID 19 PandemicHanaSuhanaNo ratings yet

- CBDCs Beyond Borders - Results From A Survey of Central Banks (Jun 2021)Document22 pagesCBDCs Beyond Borders - Results From A Survey of Central Banks (Jun 2021)Fernando HernandezNo ratings yet

- Islamic Finance TakafulDocument11 pagesIslamic Finance Takafulammar_qaiserNo ratings yet

- CPA in The USA in The USDocument2 pagesCPA in The USA in The USRonald NadonNo ratings yet

- Creditsafe Company Report 11349769 World Citizen Equity Partners LTDDocument9 pagesCreditsafe Company Report 11349769 World Citizen Equity Partners LTDDavid HundeyinNo ratings yet

- PM Quiz 4Document3 pagesPM Quiz 4Daniyal NasirNo ratings yet

- Chapter 5 Multiple Choice QuestionsDocument6 pagesChapter 5 Multiple Choice QuestionsĐan KimNo ratings yet

- Acca SBR - Book 3 - June 2022Document576 pagesAcca SBR - Book 3 - June 2022dabignoob123100% (2)

- PDF SYBCom - F Div - Paper AFM IIIDocument16 pagesPDF SYBCom - F Div - Paper AFM IIIPushkar DereNo ratings yet

- Ethical Issues in AccountingDocument20 pagesEthical Issues in AccountingKarina AyuNo ratings yet

- Government of Andhra Pradesh: Challan Reference FormDocument1 pageGovernment of Andhra Pradesh: Challan Reference FormBhoolokaReddy pitta100% (1)

- Financial Performance Analysis of Commercial Private Banks in BangladeshDocument78 pagesFinancial Performance Analysis of Commercial Private Banks in Bangladeshmd.jewel ranaNo ratings yet

- Project Work of Accounts (055) Ratio Analysis: Submitted By-Avishkaar JainDocument30 pagesProject Work of Accounts (055) Ratio Analysis: Submitted By-Avishkaar JainAvishkaar JainNo ratings yet

- International Financial Regulation Seminar QuestionsDocument2 pagesInternational Financial Regulation Seminar QuestionsNicu BotnariNo ratings yet

- PPP Luggage Purchase AnalysisDocument21 pagesPPP Luggage Purchase AnalysisTruc PhanNo ratings yet

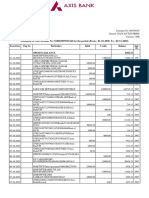

- Statement of Axis Account No:918010099547443 For The Period (From: 01-10-2020 To: 02-11-2020)Document5 pagesStatement of Axis Account No:918010099547443 For The Period (From: 01-10-2020 To: 02-11-2020)minniNo ratings yet

- Superhouse Limited: Email: Share@superhouse - in Url: HTTP://WWW - Superhouse.inDocument7 pagesSuperhouse Limited: Email: Share@superhouse - in Url: HTTP://WWW - Superhouse.inAmrut BhattNo ratings yet

- Group 5 Monetary Central BankingDocument19 pagesGroup 5 Monetary Central BankingAurea Espinosa ErazoNo ratings yet

- Title of The Project: Life Insurance Corporation (LIC)Document46 pagesTitle of The Project: Life Insurance Corporation (LIC)KusNo ratings yet

- West Bengal eProcurement Refund ReportDocument2 pagesWest Bengal eProcurement Refund ReportKalyan GaineNo ratings yet

- 1642335769414loosciwbpgxnvjdbpdf Original-3Document1 page1642335769414loosciwbpgxnvjdbpdf Original-3Gopichand YadavNo ratings yet

- CPA Paper 16Document9 pagesCPA Paper 16sanu sayedNo ratings yet

- Wattal Committee ReportDocument2 pagesWattal Committee ReportKunwarbir Singh lohatNo ratings yet

- Coindaq PDFDocument1 pageCoindaq PDFmuruganNo ratings yet

- Terrific Temps Fills Temporary Employment Positions For Local Businesses SomeDocument2 pagesTerrific Temps Fills Temporary Employment Positions For Local Businesses SomeAmit PandeyNo ratings yet

- BBA Final ReportDocument23 pagesBBA Final ReportPitambar PoudelNo ratings yet